The task to decarbonise Australia’s electricity sector is immense. Australia has set ambitious targets for emissions reductions in the electricity sector by 2030, including a national policy target of 82% renewables and state-based targets with similar ambitions.

To achieve these targets, Australia has embarked on one of the largest and most ambitious infrastructure builds in the country’s history. The energy capital investment task between 2020 and 2030 (covering grid-scale generation and new transmission) is expected to be c.$300 billion-$400 billion AUD.1 This will exceed the scale of the 2007-2017 liquefied natural gas(LNG) investment boom and will almost equal the size of the economy-transforming 2005-2015 mining investment boom. This will be one of the largest capital investment cycles we have ever undertaken.

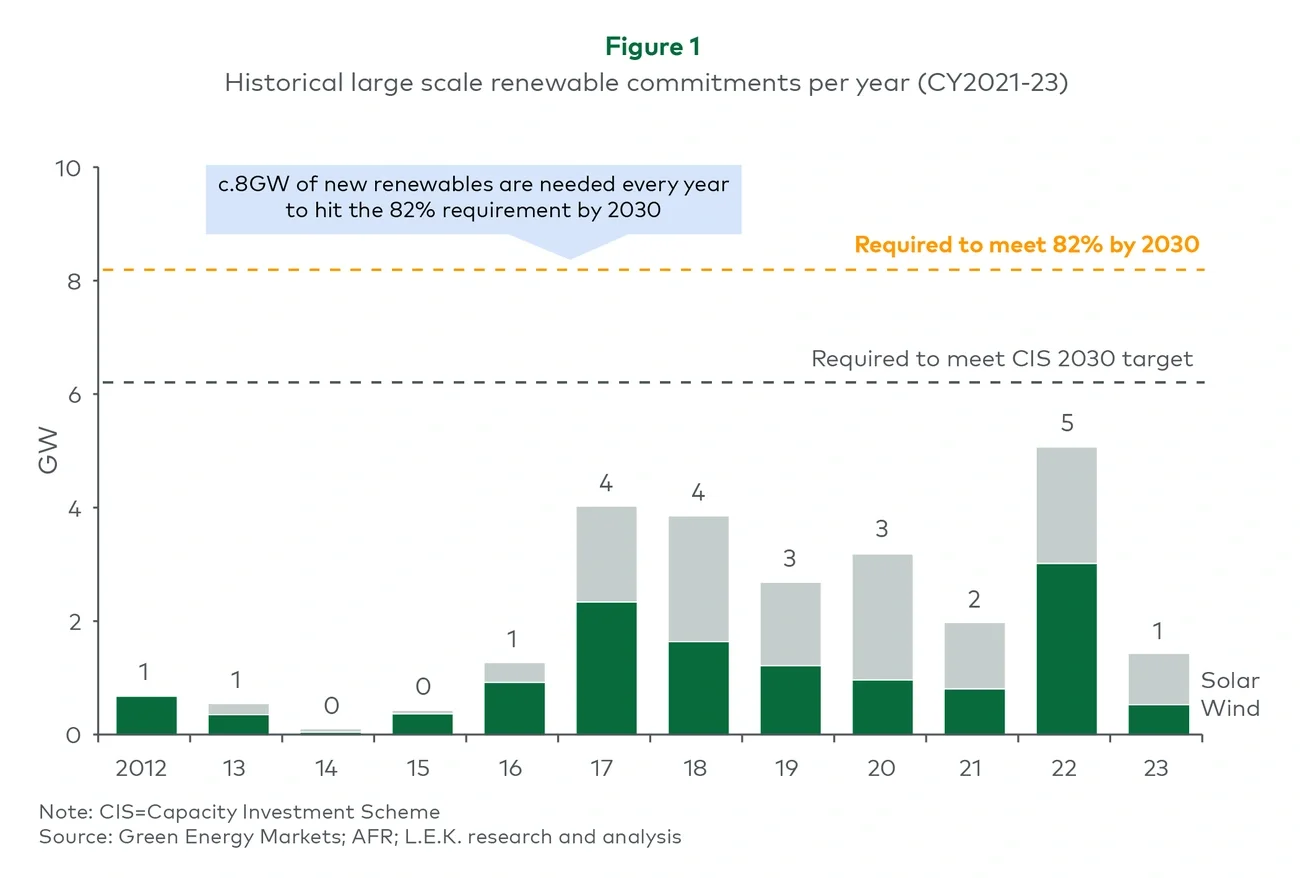

However, building large-scale generation at the pace needed to achieve this goal will be incredibly difficult. Achieving the 82% renewables target by 2030 will require 8GW of new renewable capacity to be added each year between 2024 and 2030. This compares against a historical peak of 5GW added in 2022 and a recent average of c.2.9GW p.a. from 2019 to 2023 (see Figure 1). Global supply chains and obtaining environmental and planning approvals, landholder engagement and community licence, and local industry and workforce capacity represent significant barriers to this pace of large-scale generation construction.