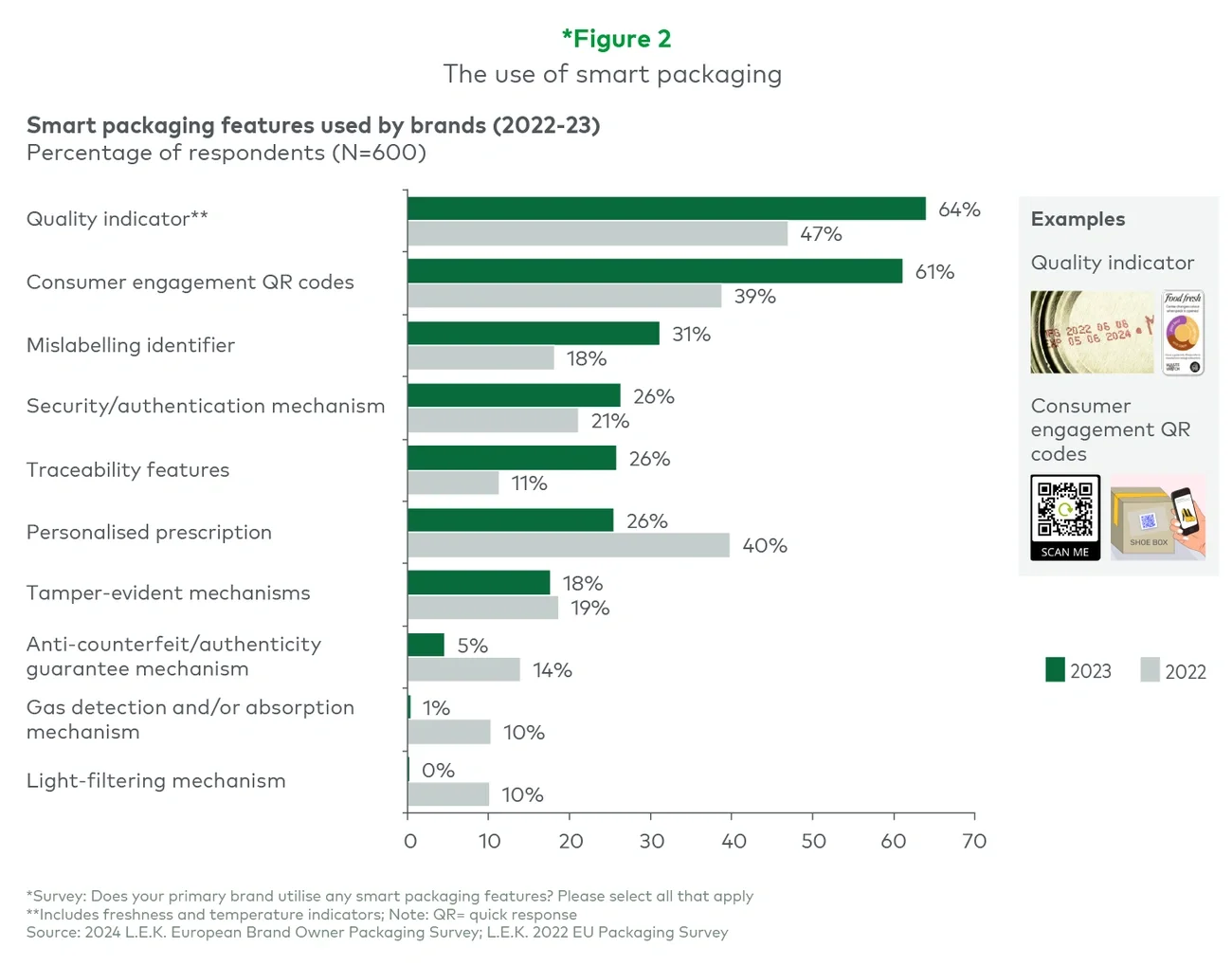

Respondents cited positive support for smart packaging from across sectors and geographies. Their feedback highlights the multiple benefits of smart packaging, making a compelling case for its future:

“Our customers really appreciate the company’s commitment to effective, safe pharmaceutical products, monitored in real time, [which] leads to increased brand loyalty.”

— French health and wellness brand

“A temperature indicator in the packaging proved to be a strategic move that increased both profits and sales.”

— UK food and beverage brand

“The smart labelling identifier offers personalised product suggestions and discounts based on customer preferences obtained from the collected data.”

— Spanish food and beverage brand

“This smart packaging method will significantly increase consumer satisfaction and engagement by providing valuable information and instructions on how to use and benefit from the product.”

— German household brand

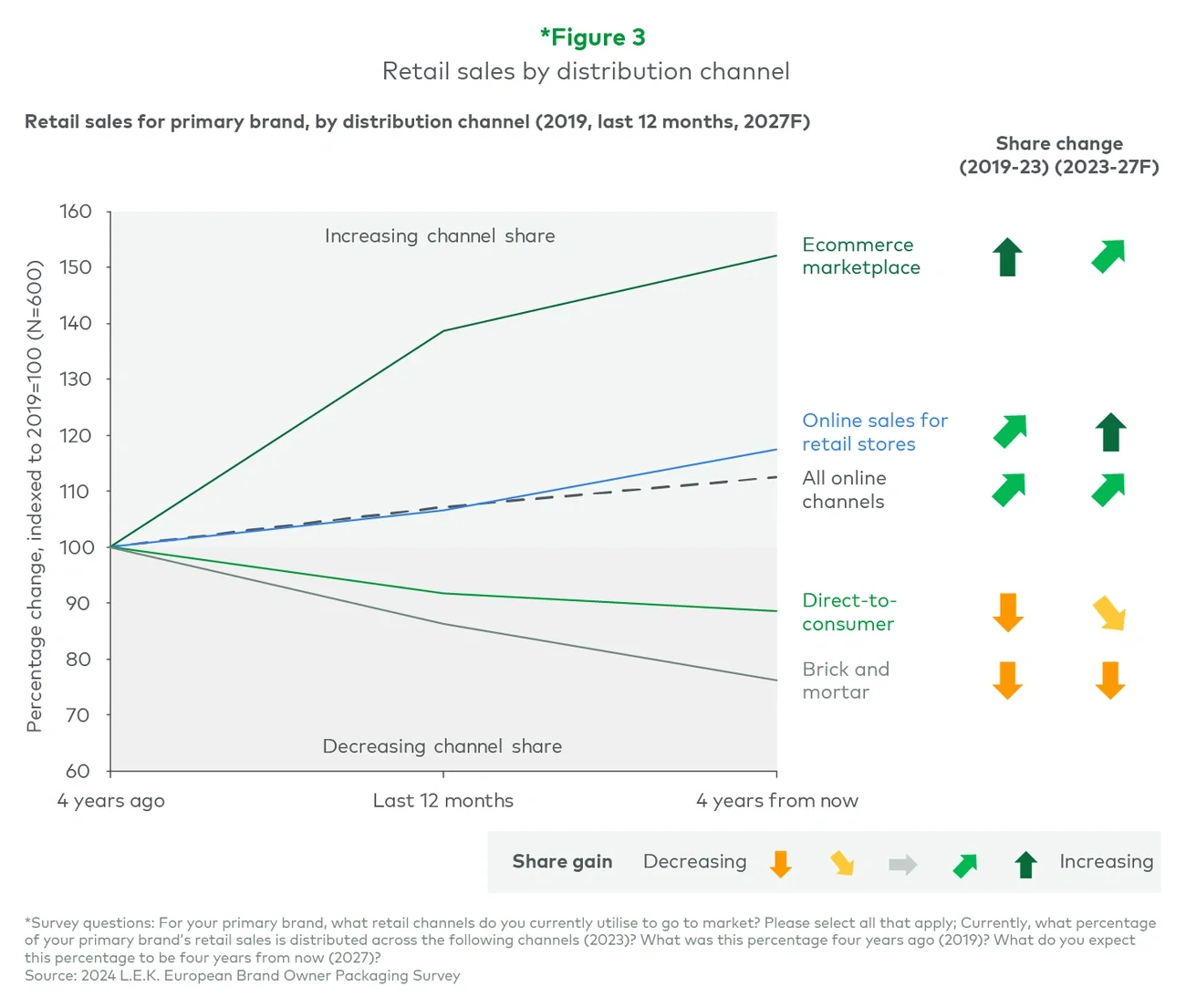

Ecommerce clicks with consumers

As online shopping continues to grow in popularity, brand owners are looking for new ways to tailor packaging to suit specific channels.

The brand owners taking part in our survey expect ecommerce to continue to gain market share to 2027 and beyond, an increase driven primarily by growth in ecommerce marketplaces. They told us that they anticipate a further decline in sales at bricks-and-mortar locations. In addition, they said the troubled direct-to-consumer model is facing difficulties, especially among brands that are largely supported by venture capital and relying on buying revenue rather than generating it organically.

The rise of ecommerce is a trend common across all end markets (see Figure 3), with substantial growth in online sales for beverage, health and household, and food brands over the past four years of c.79%, c.54% and c.39%, respectively. Much of this growth can be attributed to the impact of the COVID-19 pandemic, and this trend is expected to decelerate in the future, pointing to a more subdued outlook for ecommerce in these sectors.

In contrast, our survey shows pet food and consumer electronics categories exhibiting a more consistent and viable penetration of the ecommerce channel, with steady trajectories and sustainable growth at 10%-15% over the past four years.