These assets are now likely approaching the end of their hold periods, many of which were extended, as mentioned earlier, due to COVID-19, macroeconomic conditions (e.g., rising interest rates, inflation), destocking and volume challenges from lowered consumer confidence.

Industry participants involved in packaging M&A are more optimistic about transaction activity in the near term compared to 2024, as packaging volume challenges associated with destocking dynamics come to an end and consumer spending begins to trend toward normal following elevated inflation. However, key factors will likely impact what assets come to market and ultimately transact in the near term.

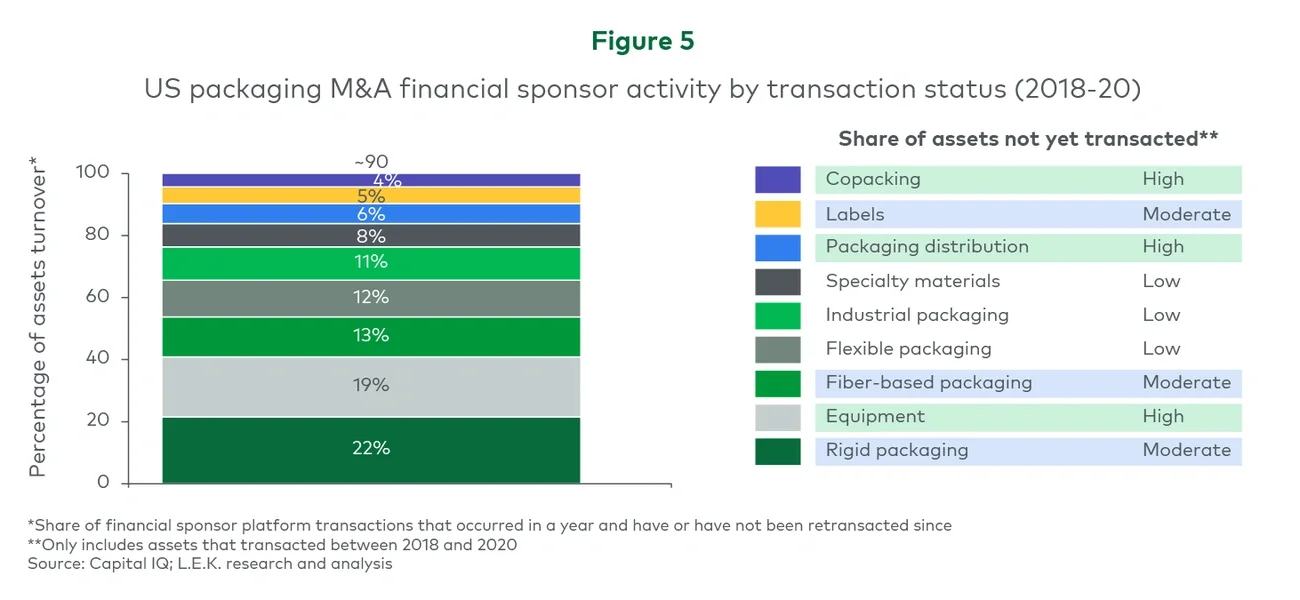

Although distribution of assets across subsectors is fairly even, assets more heavily impacted by destocking (i.e., those serving more shelf-stable product categories within food, beverage, home and personal care) could take longer to come to market as sellers continue to delay transactions in order to show normalized EBITDA levels and volume growth for their businesses.

Conclusion

Looking toward 2025 and beyond, there are solid reasons for optimism among sellers wanting to realize a return on a previous investment and buyers wishing to gain or increase exposure in the packaging sector.

Although many sellers are hopeful that their business assets have returned to normal, strategic buyers remain interested in platform-building, and more favorable macroeconomic conditions should boost sellers’ confidence in their ability to successfully transact. Buyers are likely to find an increased supply of available assets across segments. This should expand the probability that they will find assets to align well with their investment goals.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC