The consolidation of veterinary services markets is expected to continue at pace across many European countries, presenting significant value creation opportunities for operators and investors in animal health. Rising in-catchment competition across all dimensions of competition will require independent and corporate players alike to become more sophisticated, as consolidation for procurement synergies alone is no longer enough.

Consolidation momentum underpinned by favourable structural trends

Veterinary services markets across the globe are characterised by favourable structural trends. Pet populations are growing, reflecting powerful societal trends, including younger generations seeking to adopt a pet prior to, or even instead of, starting a family and an ageing population seeking companionship in animals — an issue brought into sharp focus by the COVID-19 pandemic. Meanwhile, pets are increasingly being treated as members of the family

The ‘humanisation’ of pets is not only driving greater spend per pet but also increasing the resilience of spend throughout the economic cycle, which represents a sea change in how society views pets over a single generation.

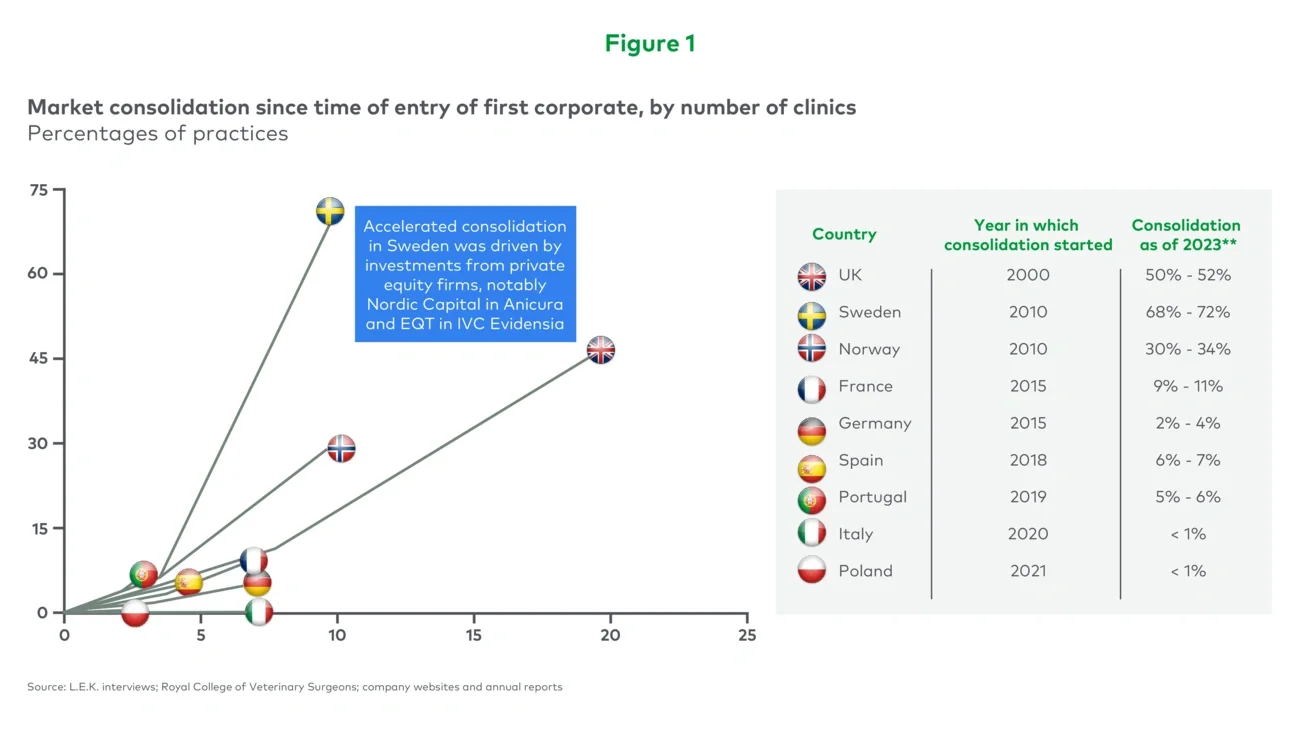

Compelling long-term growth prospects have attracted significant investor interest in the animal health sector. This is particularly evident in the current consolidation of veterinary practices across Europe, which is being accelerated by private equity backed businesses. Whilst there are local variations in the speed and progress of the major underlying trends — reflecting varying degrees of market maturity as well as some cultural and macroeconomic differences — we expect European markets to continue to consolidate at pace over the coming years, with significant implications for both operators and investors. Figure 1 shows the progress of vet services consolidation across a range of European markets.