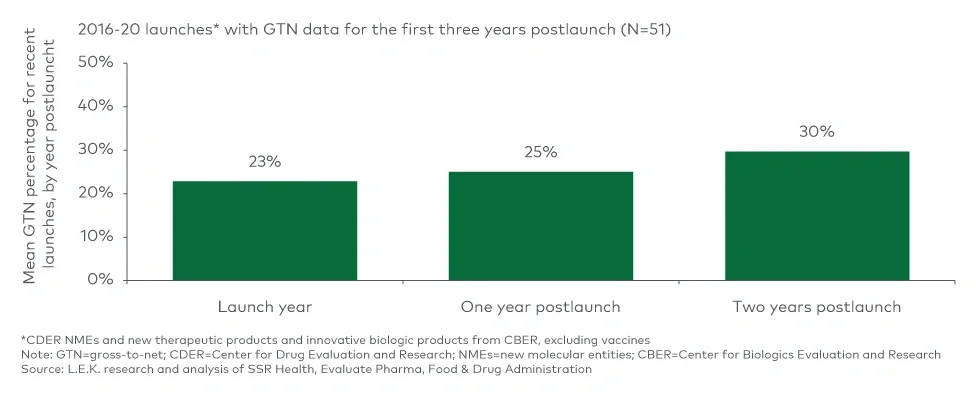

In the early postlaunch years, investing in patient assistance programs can be effective to maximize uptake by capitalizing on early demand as broad payer coverage is being established. This can mean covering the full cost of the product for patients who are not yet covered, which comes with a notable up-front impact on net price per patient. However, satisfying early customer demand and reducing access barriers can steepen the uptake curve and foster positive sentiment among patients and prescribers. As patients are then converted to traditional coverage (if treated chronically), net price per patient can improve moving forward.

Once payer access and net price are established, it can remain stable until manufacturers choose to pivot in response to insufficient pull-through of demand, new competitive entrants or shifts in payer/public policy.

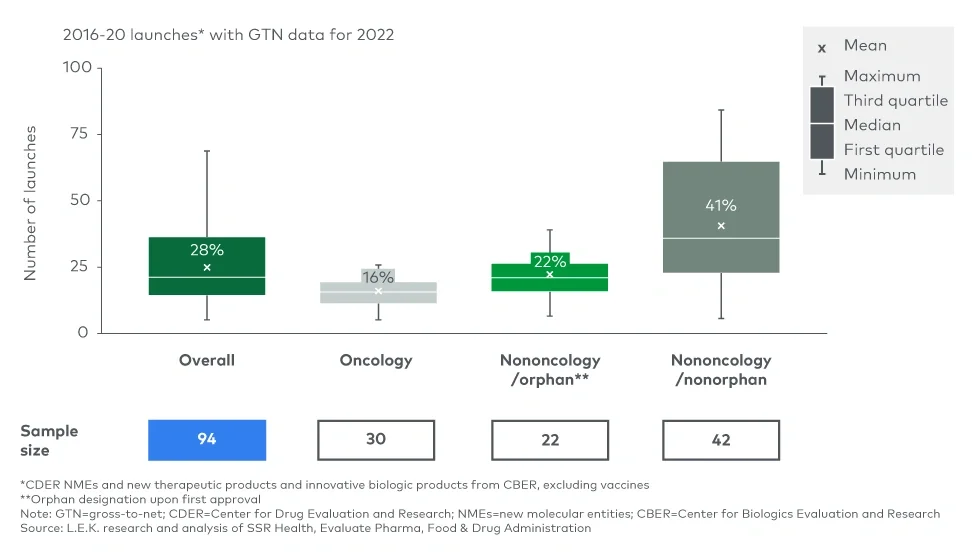

Biosimilar or generic competition can represent the ultimate threat to a product’s GTN as significant net price competition ensues and payers drive use toward lower-cost options. However, in today’s GTN environment, those who are already heavily discounting may be somewhat protected due to “rebate walls.” On the other hand, products that have maintained modest GTN deductions are most susceptible to market share erosion upon biosimilar entry. A recent report illustrates this dynamic well, clearly showing that oncology, the therapeutic area with the most modest GTN deductions, has been the most susceptible to market share and net price (average sales price) erosion from biosimilars.

New policies may have significant impacts on GTN

Upcoming policy changes, namely IRA, are a looming presence whose impact on GTN will be felt directly and indirectly, in some ways applying additional pressure and in other ways disincentivizing practices that have driven increasing GTN over time. We have been closely following the IRA and its potential impacts throughout the biopharma ecosystem.

Most prominent is the Centers for Medicare & Medicaid Services (CMS) Maximum Fair Price negotiation after nine (small molecule) or 13 (biologic) years, which will affect products with >$200 million in gross Medicare spending. For selected products, net price is likely to decline for the remaining years of patent life, though uncertainty around the magnitude of decline remains, as there is no “floor” for Maximum Fair Price. Life cycle evaluations and revenue expectations will now need to be viewed through the lens of both patent and CMS negotiation runways. The curtailed life cycle of branded drugs, and more so for small molecules, may place a greater emphasis on maintaining optimal margins early.

The Part D benefit redesign under the IRA introduces two key changes with implications for GTN. First, manufacturers will have direct liability in the coverage (10%) and catastrophic phases (20%) in lieu of coverage gap liability (70%). Second, plan sponsors, not CMS, will now face most of the liability in the catastrophic phase (60% vs. 15% pre-IRA). This creates increased incentive for plans to implement utilization management controls for high-cost drugs, which may drive further discounts. Historically, patients who reached the catastrophic phase drove rebates to plan sponsors, while CMS faced the liability; plans’ heightened liability in the catastrophic phase per the IRA may disincentivize high-list-price, high-rebate strategies.

The IRA also introduces new penalties in Medicare for list price increases that outpace inflation, disincentivizing postlaunch list price increases, even if those strategies maintain consistent net price. Finally, under the American Rescue Plan, the 100% “Average Manufacturer Price (AMP) cap” on Medicaid rebates has been removed, which also disincentivizes high-list-price, high-rebate strategies that previously would have been triggered by this cap and protected GTN margin.

Outside the IRA, GTN dynamics may be impacted by a number of other market trends, including PBM legislation, 340B growth and hospital consolidation.

Biopharmas will need to consider several key GTN questions when strategically planning

- What is the expected magnitude of GTN for a drug’s particular market situation?

- How sensitive are forecasts to GTN dynamics?

- How will GTN evolve over the product’s life cycle?

- How will new policies, such as the IRA, impact GTN strategy?

Our Biopharma practice works with clients across a range of strategic issues, including pricing and access optimization, IRA preparation, and developing dynamic GTN forecasting. If you or your organization is interested in discussing the implications of the growing GTN bubble or the implications of IRA/PBM legislation for your future opportunities and optimal strategies to prepare, please reach out to us.

We would like to thank Adam O’Neil for his contributions to this piece.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC