In August 2022, President Joe Biden signed the Inflation Reduction Act (IRA) into law, marking the most significant healthcare reform since the Affordable Care Act. This is a step forward in improving the affordability of and access to innovative treatments. The IRA includes multiple provisions, including a limit on copayments for insulin covered under Part D or furnished through durable medical equipment (DME) under Part B; elimination of out-of-pocket cost sharing for adult vaccines covered under Part D, Medicaid and CHIP (Children’s Health Insurance Program); expanded eligibility for low-income subsidies; and, importantly, a $2,000 annual cap on Part D patient out-of-pocket costs.

The IRA provision with the potential to most significantly impact future revenues and investment for biopharmaceutical manufacturers is the authorization of CMS to directly negotiate a maximum fair price for therapies covered under Medicare Parts B and D with substantial punitive measures if manufacturers do not consent to pricing negotiation.

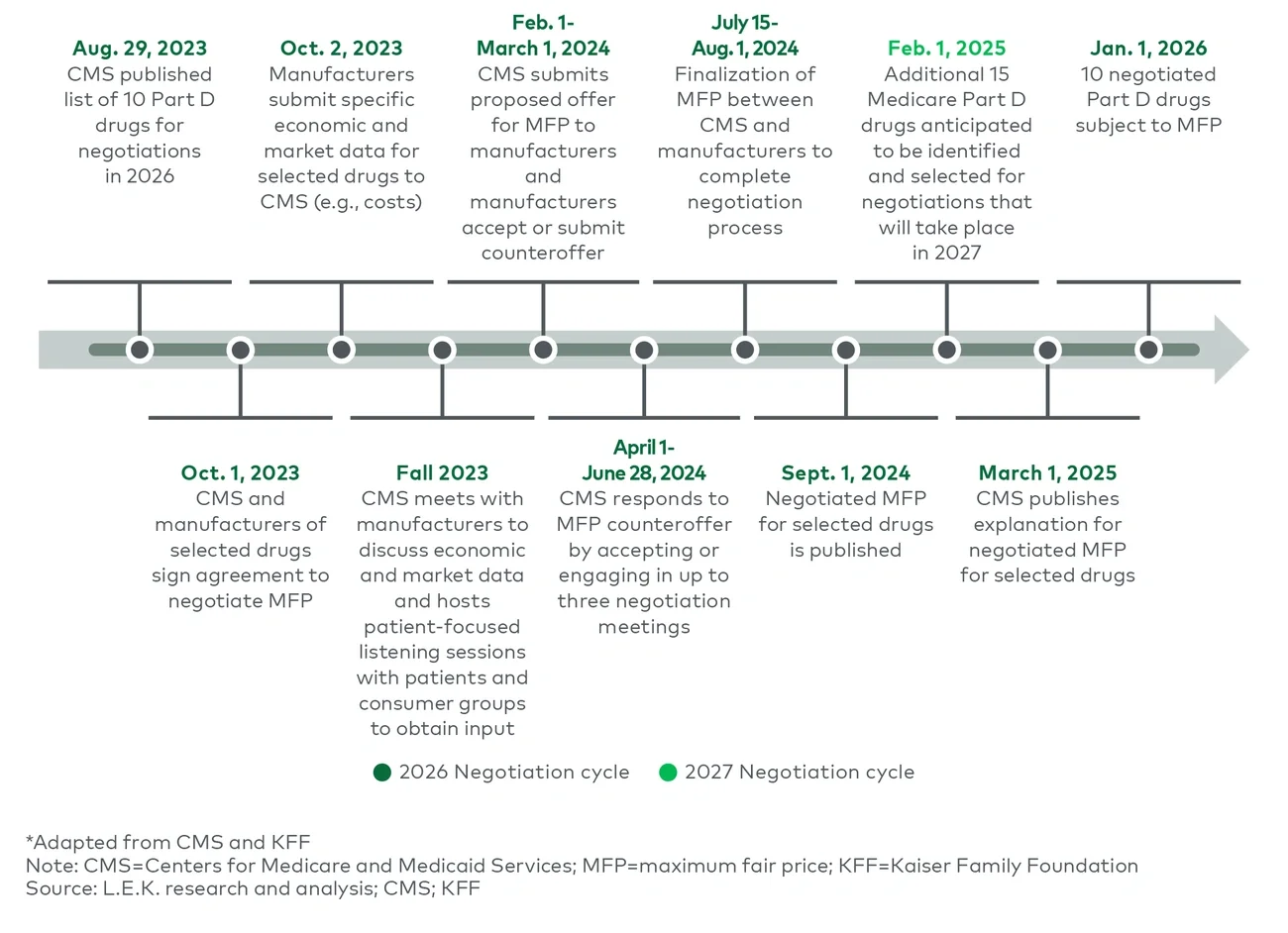

On Aug. 29, 2023, the Centers for Medicare and Medicaid Services (CMS) disclosed the first 10 products to be subject to this negotiation beginning in 2026. In this report, L.E.K. Consulting discusses the announcement, the response and the implications for biopharmaceutical companies.

Medicare negotiations will significantly decrease drug prices, cutting revenues for biopharmaceutical manufacturers

Under the IRA, the secretary of the U.S. Department of Health and Human Services is authorized to select products that will be subject to a maximum fair price (MFP) negotiated by CMS. Manufacturers will be required to sell these therapies at no more than the MFP to any Medicare beneficiaries. Most products covered by Medicare are subject to negotiation on MFP after they have been FDA approved for seven years in the case of small molecule new drug application (NDA) approval or 11 years for biologics approved with biologics license applications (BLAs), and MFP pricing is instituted two years later.

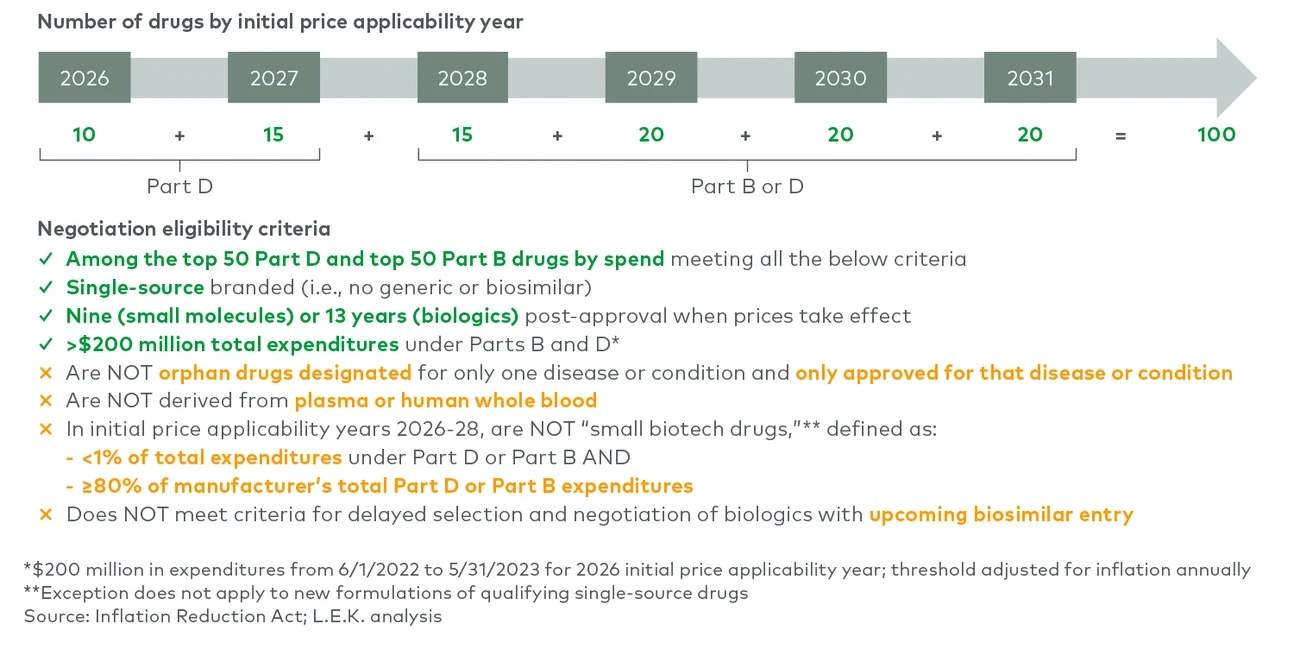

CMS is authorized to implement MFP for up to 100 Medicare-covered therapies by 2031. Negotiations will begin with product on Medicare’s Part D program (10 subject to MFP by 2026 with 15 more by 2027) before expanding to include both Part D and Part B drugs (see Figure 1). While the MFP only applies to Medicare beneficiaries, Commercial payers are likely to follow suit and renegotiate after CMS establishes the MFP.