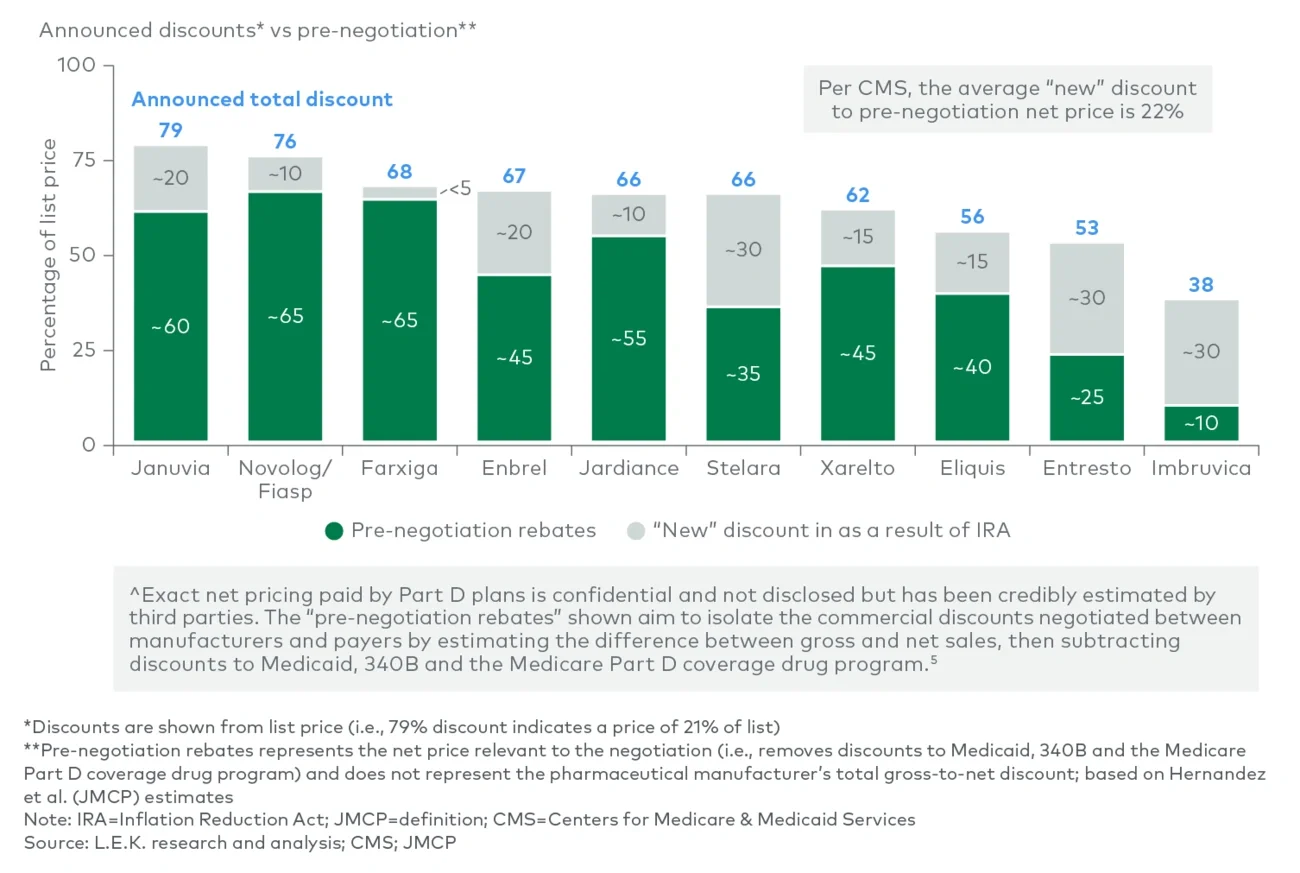

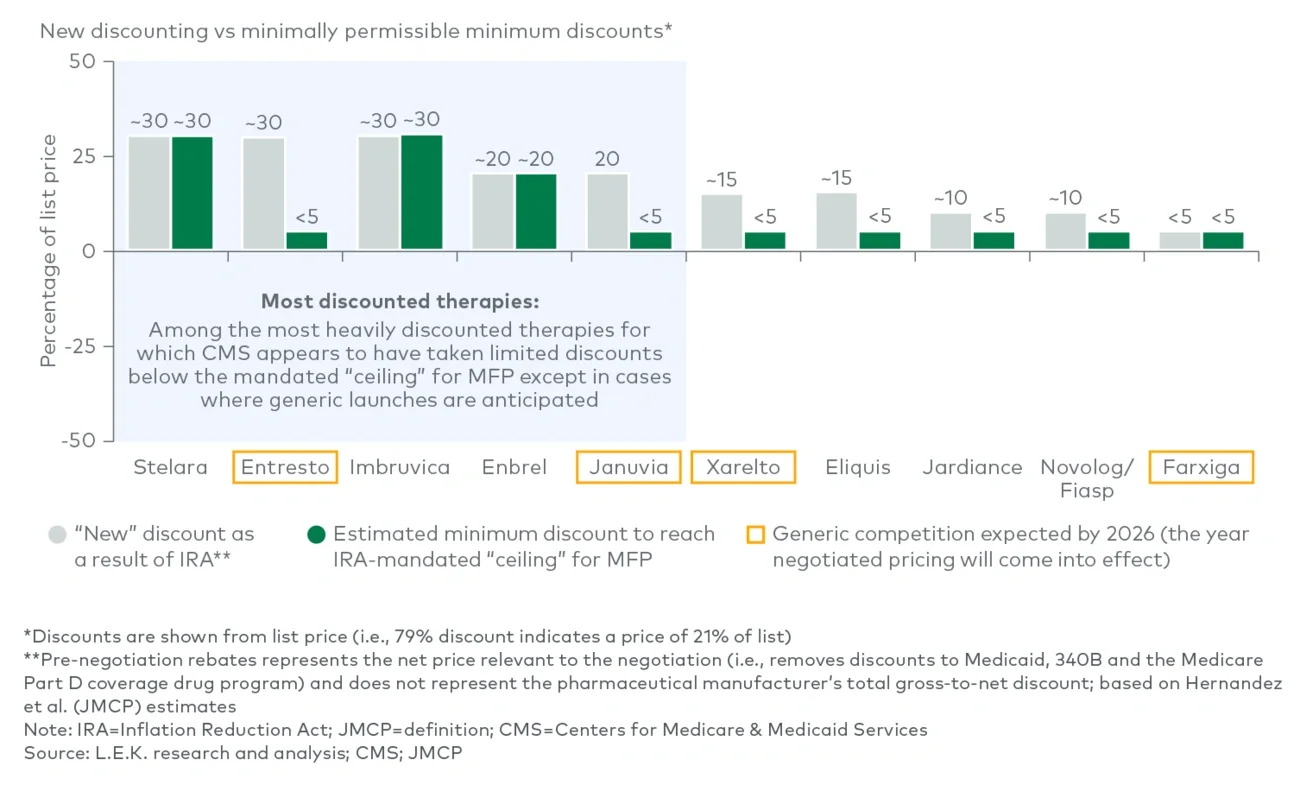

With CMS largely deferring to the mandated ceiling rather than pushing for greater discounts, the response from the market was minimal. Across affected companies, stock prices remained flat following the announcement.

While this negotiation suggests the impact of IRA negotiations may be muted for many products, substantial risks remain

The announcement suggests that the impact of the IRA may be relatively muted for products with already high rebates. And if CMS continues to discount to the statutory minimum, future rounds may be even less burdensome. This first round of product negotiations included more agents on the market for over 16 years, which have a lower mandated ceiling for MFP than more recently launched drugs do. In the future, this number should decline, potentially leading to lower overall discounts from pre-negotiation net prices.

Still, there are ongoing risks for future negotiated products. In particular, Imbruvica’s result may signal that oncology products may feel the greatest sting in future negotiations. Oncology products typically have relatively low rebating pre-negotiation, so the IRA’s mandated MFP ceiling is expected to impact these products more substantially. While the next set of 15 products to be negotiated has not been confirmed, L.E.K. predicts that oncology will be two to three times more represented in the next list of products than it is in these first 10.

Additionally, it is unclear how the negotiated products’ competitors will be impacted, if at all. Access to these negotiated drugs, and changes in access for competitors, may be less straightforward than one would expect. Negotiated drugs may be less profitable for Part D plans, given fewer rebates and exemption from new cost-sharing requirements. CMS understands that the negotiation will disrupt drug channel incentives, and intends to monitor Part D plans to make sure they remain preferred.

Perhaps most important, with so much negotiating power at the discretion of CMS, pharma is not guaranteed that the relatively conservative discounting from this round of negotiation will hold fast in the future. Changes in CMS leadership and strategy may drive a significantly more aggressive posture in future negotiations — and deeper discounts. The coming of a new U.S. presidential administration in 2025 only adds greater uncertainty as to whether the result of this negotiation round will be predictive of future negotiations.

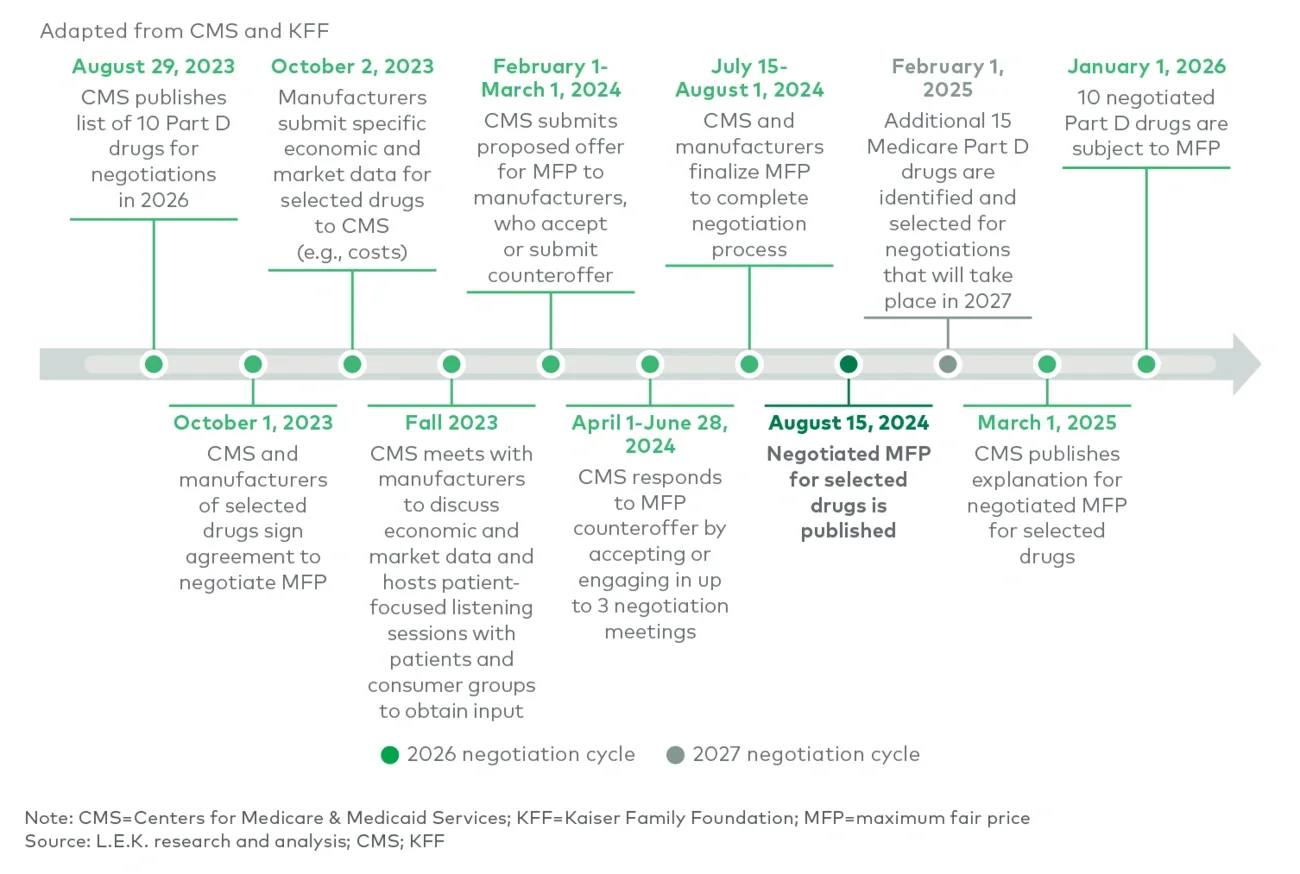

What is certain is that the IRA negotiations are having a continuing impact on pharma R&D decision-making. Some companies have publicly discontinued programs, some have shifted away from small molecules (given the shorter pre-negotiation window), some are avoiding orphan indication expansions and some are investing in next-generation products to restart the negotiation clock. Uncertainty around negotiation selection and impact may also deter biosimilar development. The prices announced in August will be in effect by 2026, but the repercussions of this action will be felt for much longer.

Our firm’s Biopharma practice works with clients across a range of strategic issues, including preparing for the impact of IRA negotiations on R&D, commercial and business development strategies. If you and your organization are interested in discussing the implications of the IRA on your future opportunities, as well as optimal strategies to prepare, please reach out to us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC