The business model for biopharmaceutical research and manufacturing is unique among industries. Manufacturers invest in research and development (R&D) at high cost and with high risk and long-time horizons. In fact, the biopharmaceutical industry has the highest R&D intensity of any industry as of 2019. As a result, in the past decade, the industry has brought to market transformative treatments including immune checkpoint inhibitors for solid tumor cancers, a new curative treatment for hepatitis C, cell therapy for leukemia and lymphoma, and, most recently, vaccines and treatments for COVID-19. U.S. companies led the world in the number of new chemical and biological entities launched from 2000 to 2020, and the U.S. is widely considered the most critical market for biopharmaceutical manufacturers, accounting for nearly 50% of branded prescription biopharmaceutical net revenues.1,2 This is due to a range of factors, including access to capital and talent, regulatory frameworks that promote innovation, and favorable pricing conditions.

On Aug. 16, President Biden signed the Inflation Reduction Act into law, marking the most significant healthcare reform since the Affordable Care Act. Several provisions of the act are a step forward in improving affordability of and access to innovative treatments, which is of benefit to patients and biopharmaceutical manufacturers alike. These include a limit on copayments for insulin covered under Part D or furnished through durable medical equipment (DME) under Part B; elimination of out-of-pocket cost sharing for adult vaccines covered under Part D, Medicaid and CHIP (Children’s Health Insurance Program) programs; expanded eligibility for low-income subsidies; and, importantly, a $2,000 annual cap on Part D patient out-of-pocket costs for the first time ever. However, several of the act’s key provisions will directly lead to lost revenue for biopharmaceutical manufacturers and require them to reevaluate their R&D budgets and portfolio priorities as a result. In this Executive Insights, L.E.K. Consulting discusses how this legislation is expected to impact biopharmaceutical manufacturers and how manufacturers can respond as they navigate this new normal.

Several key provisions of the Inflation Reduction Act focus on drug pricing

The law contains several key provisions related to Medicare that will directly impact drug pricing:3

-

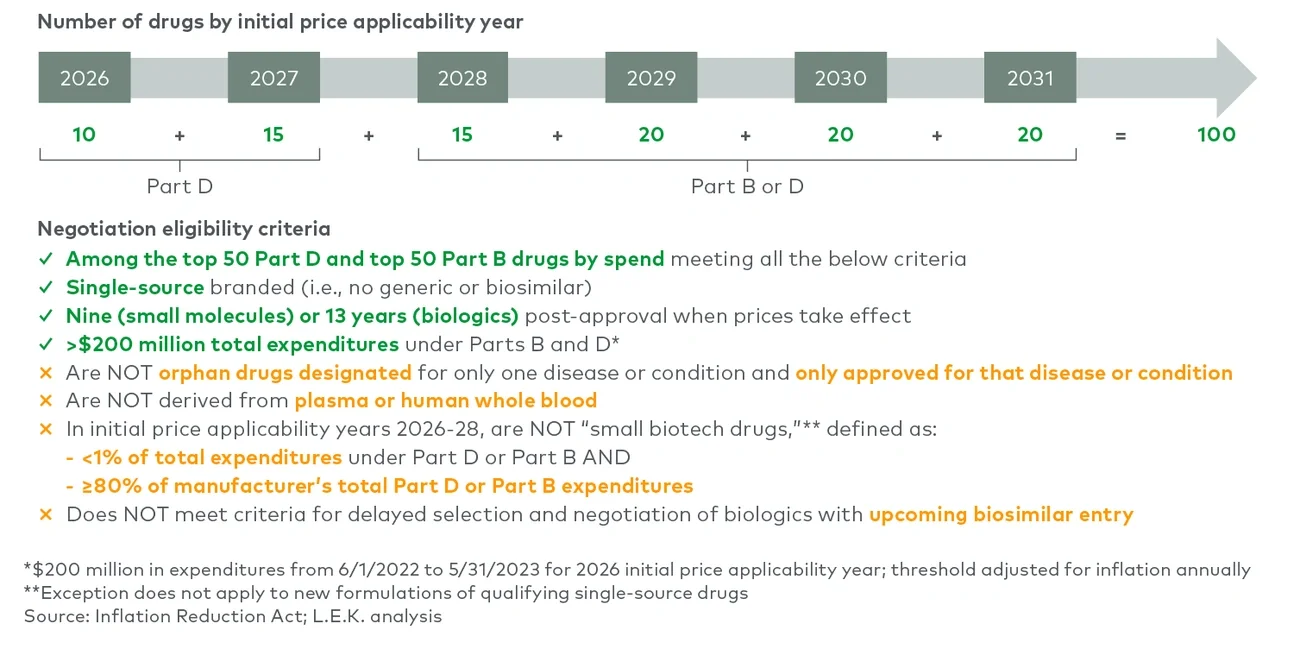

Medicare drug price negotiation: The secretary of Health and Human Services will be empowered to negotiate the prices of selected drugs with high budget impact on Medicare Parts B and D, with the first negotiated prices going into effect in 2026. The act’s penalties for noncompliance (including up to a 95% excise tax and fines) effectively mandate that biopharmaceutical manufacturers participate in this program (see Figure 1).