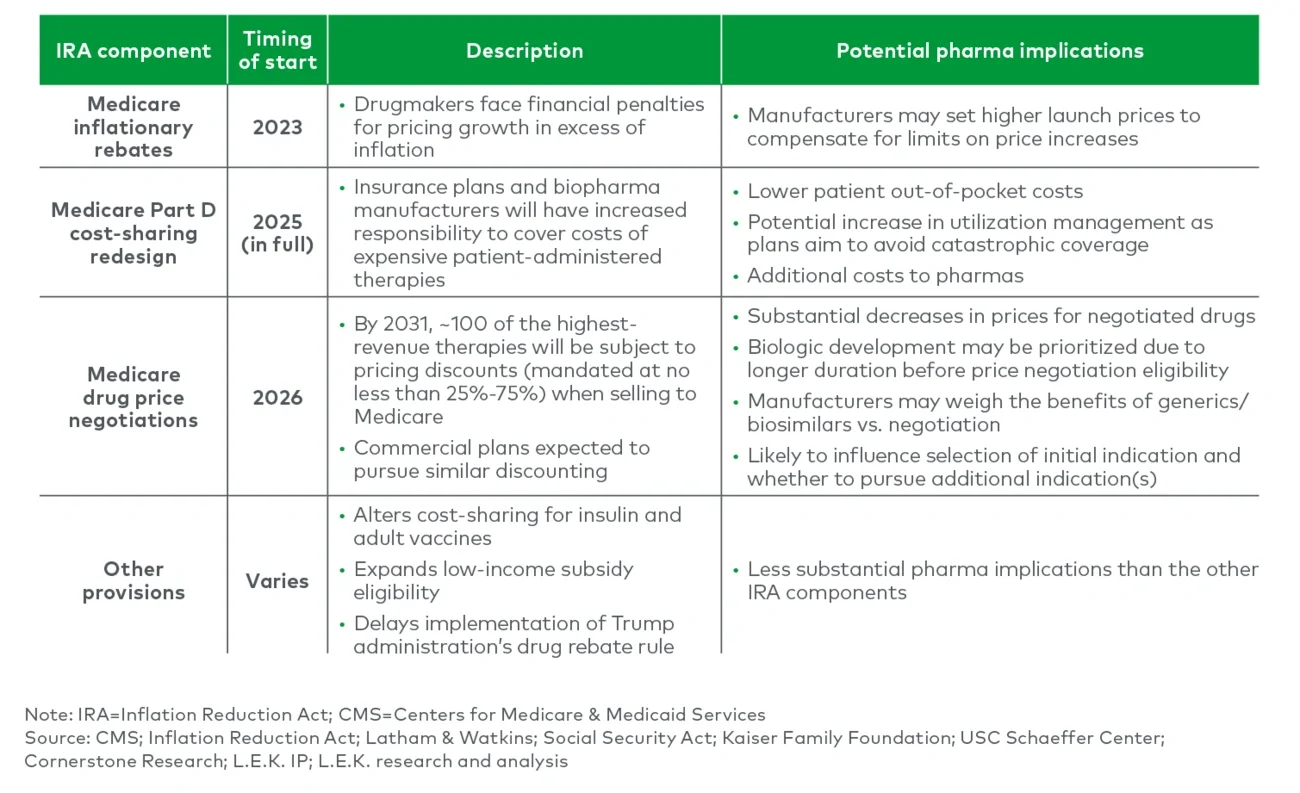

The U.S. Inflation Reduction Act (IRA) was signed into law in August 2022. It represents the most significant healthcare reform since the Affordable Care Act, amplifying affordability and access to innovative treatments. While the IRA has many provisions, its authorization of Centers for Medicare & Medicaid Services (CMS) to directly negotiate a maximum fair price for therapies covered under Medicare Parts B and D will have the most significant impact on biopharmaceutical manufacturers’ future revenues (see Figure 1). Manufacturers that agree to negotiation will have their drug prices significantly lowered; those that do not will be met with substantial penalties. In August 2023, CMS disclosed the first approximately 10 products to be subject to negotiation in 2026 — the first major step forward.

The Inflation Reduction Act: Implications for Drug Delivery Innovation

Key takeaways

The Inflation Reduction Act (IRA) is a major inflection point, improving affordability and access by allowing Medicare to directly negotiate drug prices; this will impart significant price cuts after 9 or 13 years for small molecule and biologic drugs, respectively, leading to lost revenues for biopharmas.

With increased pricing pressure and shorter product lifespans, biopharmas may look to enhance margins, shift focus to biologics and/or invest less in next-gen formulations, which would have implications for suppliers of drug delivery technologies; the initial set of drugs selected for negotiation includes several pens and autoinjectors and the next 15 will likely include a variety of inhalers.

Drug delivery technology providers should consider combining novel formulation and device technologies that meaningfully change everything from tissue localization, tolerability, efficacy and dosing intervals.

Additionally, development groups will need to plan LCM earlier and may need to enhance their platform approach to keep up with demands for multiple related molecules seeking different indications, a strategy likely to gain traction as IRA scope broadens.

Figure 1

Multiple components of the IRA will impact CMS-covered lives

While the impact of CMS price negotiations under the IRA will directly impact biopharmaceutical manufacturers, the act’s repercussions will also flow through to companies providing key inputs into drug product development, such as delivery technology. In this edition of Executive Insights, L.E.K. Consulting provides an overview of the IRA and discusses the implications for drug delivery technology providers.

Medicare negotiations will significantly decrease drug prices

Under the IRA, the Health and Human Services Secretary is authorized to select products that will be subject to a maximum fair price (MFP) negotiated by CMS. Manufacturers will be required to sell these therapies at no more than the MFP to any Medicare beneficiaries.

Most products covered by Medicare are subject to negotiation of an MFP after they have been approved by the Food and Drug Administration — for seven years in the case of small molecule NDA approval, or 11 years for biologics approved with biologics license applications (BLAs) — and MFP pricing is instituted two years later. CMS is authorized to implement an MFP for up to 100 Medicare-covered therapies by 2031.

Negotiations will begin with products on Medicare’s Part D program (10 subject to the MFP by 2026, with 15 more by 2027) before expanding to include both Part D and Part B drugs. While the MFP only applies to Medicare beneficiaries, commercial payers are likely to follow suit and renegotiate after CMS establishes the MFP.

The first wave of negotiated drugs is largely orals and injectables; the second wave likely will include inhalables

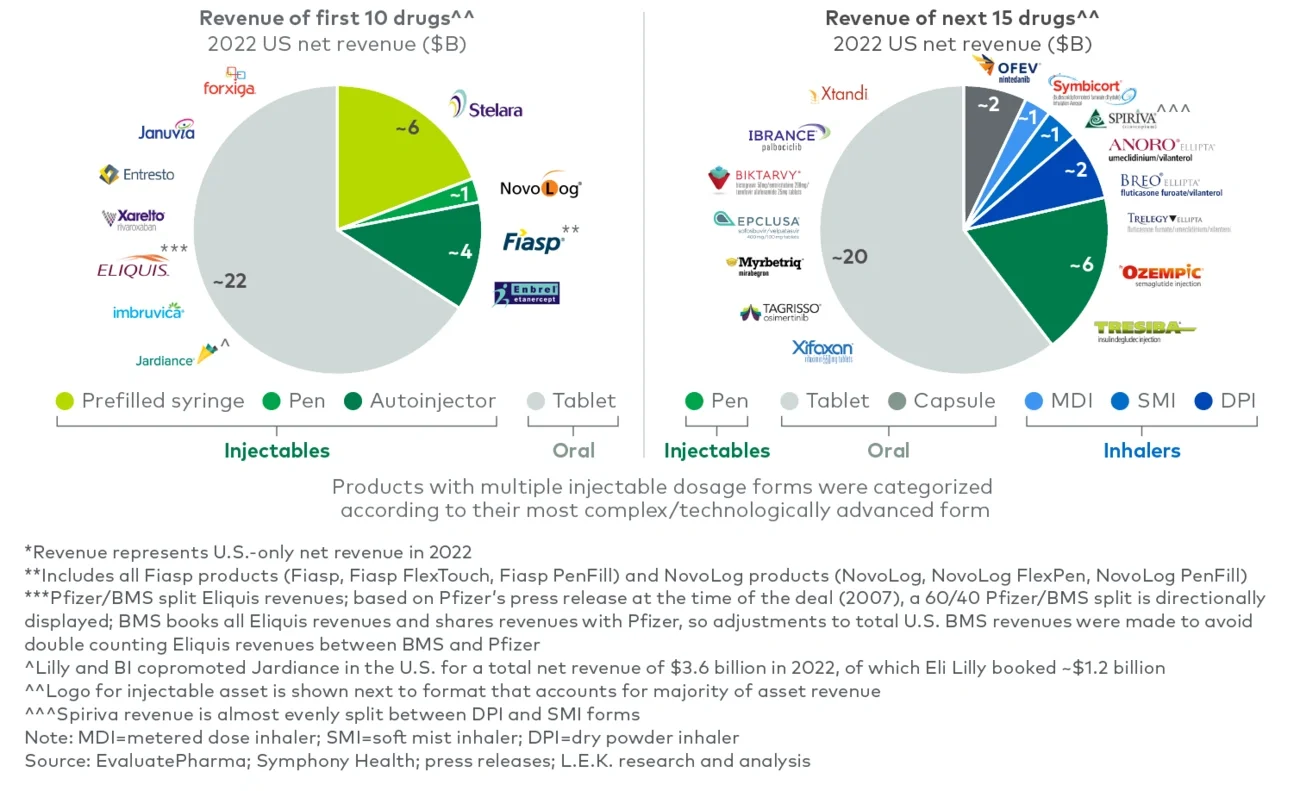

The first 10 drugs selected for 2026 Medicare negotiations represent around $30 billion in 2022 net revenues (roughly $50 billion in gross covered Part D prescription drug costs from June 2022 to May 2023). These drugs are marketed by established pharmaceutical companies and span therapeutic areas. Some may consider the list to be a first 11, as CMS grouped two of Novo Nordisk’s insulin brands as a single product. These insulins, Fiasp and NovoLog, were approved under separate BLAs and differ in the inclusion of vitamin B3.

These initial drugs were selected in a largely “mechanical” fashion, picking eligible products with the greatest Medicare Part D gross spend over the prior year while excluding those with an existing generic/biosimilar. Applying a similar logic, we have predicted drugs that may comprise the next 15 selected.

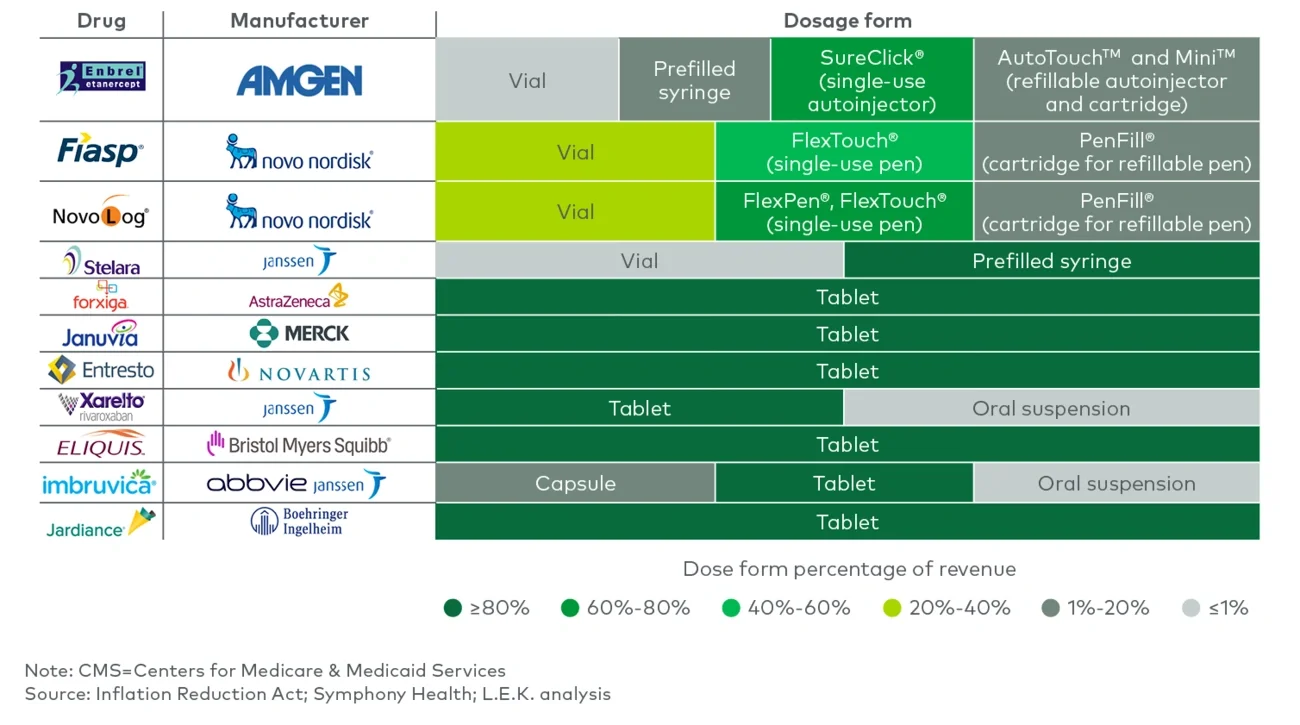

These products span dose forms and delivery technologies. The first 10 drugs selected include about three injectable therapeutics (grouping the insulins), with autoinjector, pen and prefilled syringe options, representing about $11 billion in net revenues at risk (see Figure 2). Some of these products include multiple forms. For example, the insulins (Fiasp and NovoLog) are offered as prefilled pens, cartridges (compatible with pens or pumps) and vials (see Figure 3A).

Figure 2

Negotiated products and potential next negotiated products, US net revenue* by product type

Figure 3A

Drug technology across 10 drugs selected for CMS negotiation

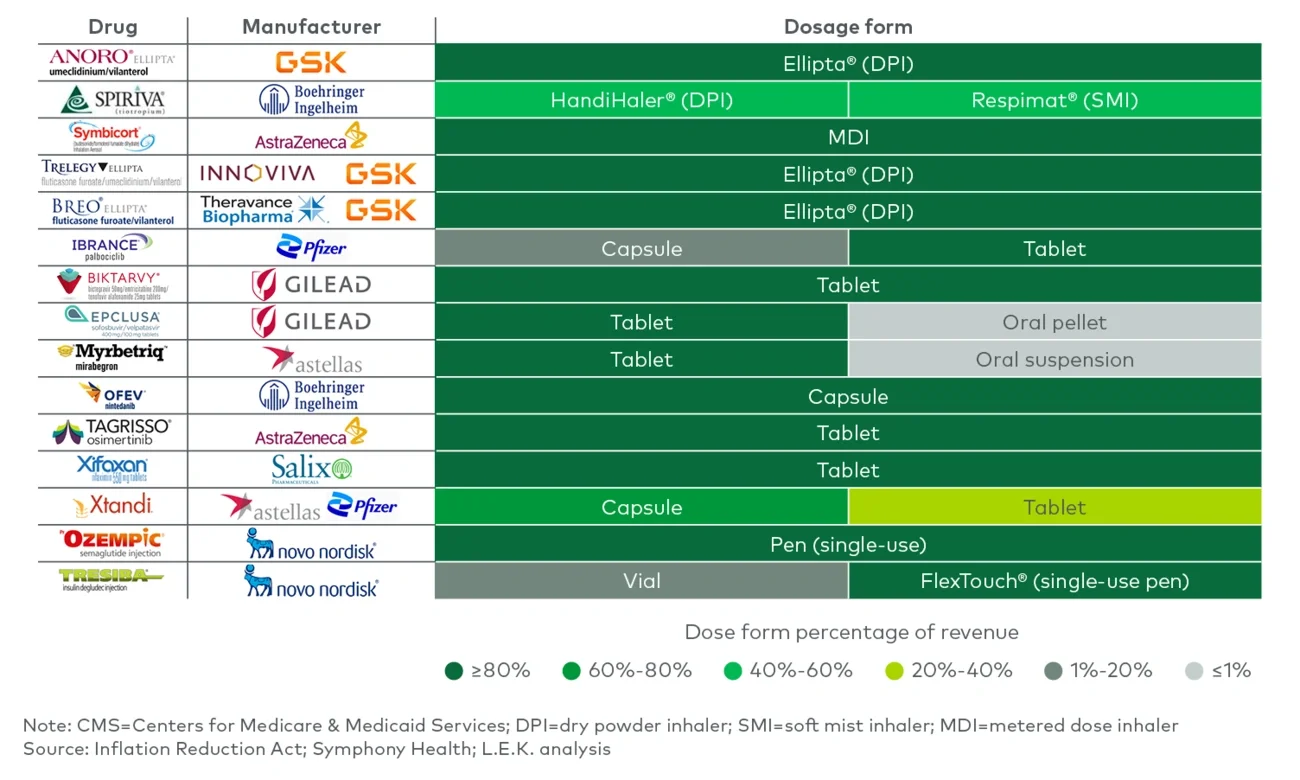

The next 15 drugs selected will likely include more orals and injectables, along with inhalables (see Figure 3B). [Disclaimer: L.E.K.’s “Next 15” represents potential candidates for CMS negotiation selection based on the current IRA framework and guidance. In early 2025, CMS is expected to announce the actual set of drugs for 2027 negotiation]. These inhalable products are tied to different delivery technologies, whether metered dose inhaler (MDI), dry powder inhaler (DPI) or soft mist inhaler (SMI). For example, Spiriva has both DPI and SMI forms, with differently branded technologies (i.e., HandiHaler, a DPI, and Respimat, an SMI).

Figure 3B

Drug technology across 15 potential next drugs selected for CMS negotiation

Unique drug delivery technologies include the following:

-

Fiasp and NovoLog’s NovoPen Echo® are refillable pens compatible with PenFill® cartridges that have a dose memory display indicating how many units were last injected and the number of hours since that injection; these pens also have more precise dosing that enables insulin delivery in half-unit increments.

-

Enbrel’s AutoTouch™ is an electromechanical refillable autoinjector compatible with Mini™ cartridges that enables one-handed injection, allows patients to choose from three different injection speeds, has light and sound cues to let patients know when the injection is complete, and is Bluetooth®-enabled to allow patients to automatically track injections in an associated app.

-

Spiriva’s Respimat® is an SMI that avoids the use of propellants (as is typical with MDIs), improves patient ease of use with a slower and longer spray that does not require coordination of device actuation and inspiration like MDIs, and results in enhanced deposition of the drug in the lungs.

-

Anoro, Breo and Trelegy’s Ellipta® devices are DPIs that are designed not only to be intuitive for patients but also to have greater versatility for delivering drug combinations due to an ability to simultaneously aerosolize two sets of blister strips containing different drugs/drug combinations. These are shown to be easier to use than other DPIs (e.g., DISKUS).

Drug delivery technology providers need to incorporate the IRA’s implications in their strategic planning

The IRA’s effects are not limited to the manufacturer — providers of delivery technology may feel the following effects:

-

With lower pricing and increased margin pressure, manufacturers may invest less in product components that lead to higher cost of goods

-

With a longer window before negotiations for biologics than for small molecules, drug manufacturers may shift away from small molecules, affecting providers of underlying delivery technology

-

Shorter product lifespans may impact drug manufacturers’ decisions whether to invest in traditional life cycle management product improvements (e.g., new delivery, new formulation), with unknowns that will be grouped as a single product

-

Later-to-market entrants may prioritize drug delivery technology at launch rather than later in the product life cycle in order to maximize differentiation early

-

Drug manufacturers may look to develop suites of related products with unique delivery technologies and indications rather than invest in single-product improvements

As delivery technology selection often occurs in the middle of clinical development and as many specifics of the IRA continue to unfold, the impact on drug delivery technology providers may take several years to crystallize.

L.E.K.’s Biopharma practice works with clients across a range of strategic issues, including preparing for the impact of IRA negotiations on R&D and commercial and business development strategies. If you or your organization is interested in discussing the implications of the IRA on your future opportunities and optimal strategies to prepare, please reach out to us.

For more information, please contact lifesciences@lek.com.

We would like to thank Ethan Bassin and Anna Li for their contributions to this piece.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC