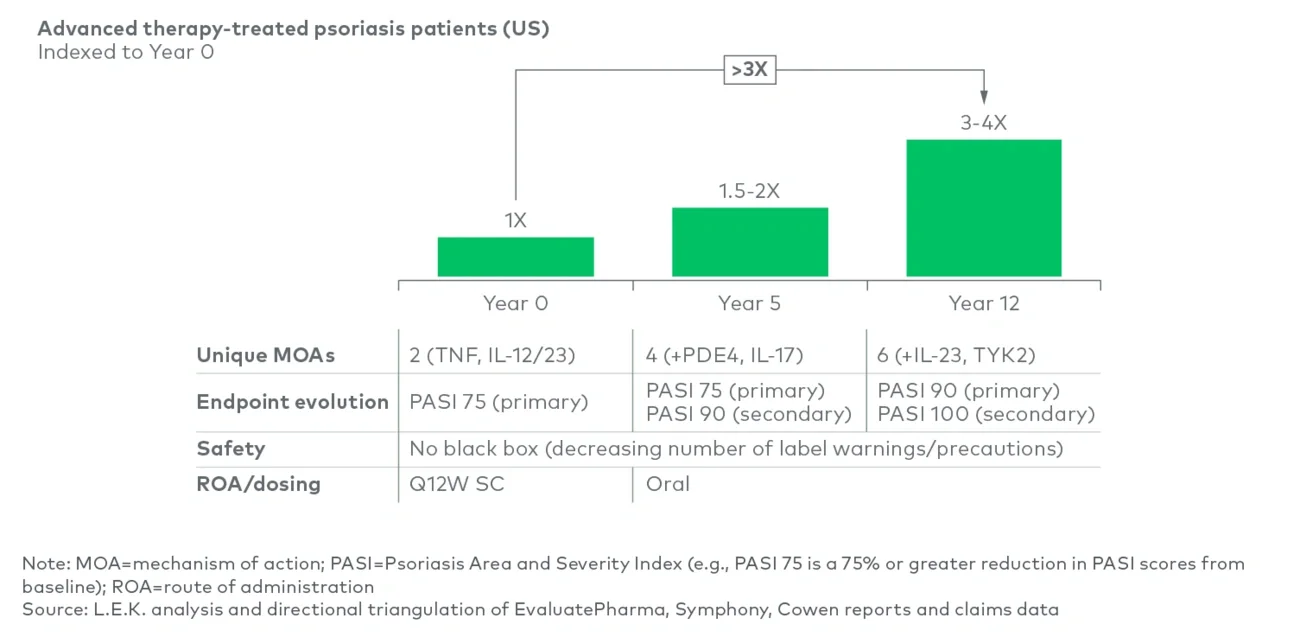

Given the cost of drug development and commercialization, it is critical to understand both whether a product is truly differentiated and whether the market is likely to expand in order to accurately gauge its commercial potential. Errors could have immense consequences, such as striving for a value proposition that does not resonate with key stakeholders, or deprioritizing an asset that would have been differentiated and missing out on a potential blockbuster. Over 60% of all innovative branded products approved between 2004 and 2018 failed to reach $250 million in U.S. revenues. Most of these products underperformed expectations, often because a team did not understand which endpoints most important or what performance thresholds were required across these endpoints, or was not realistic about the probability of achieving such thresholds.

The Inflation Reduction Act, which may incentivize companies to accelerate development given a potentially shorter drug life span, could further exacerbate companies’ inability to accurately gauge their products’ market potential. However, striving for faster development pathways should not come at the expense of understanding the target product profile required for commercial success. Still, many organizations are using outdated approaches to assess both internal and external product opportunities.

- Have a clear target product profile with both R&D and commercial input. Make sure it is based on performance thresholds across key endpoints that will enable share capture and that the R&D team feels are achievable.

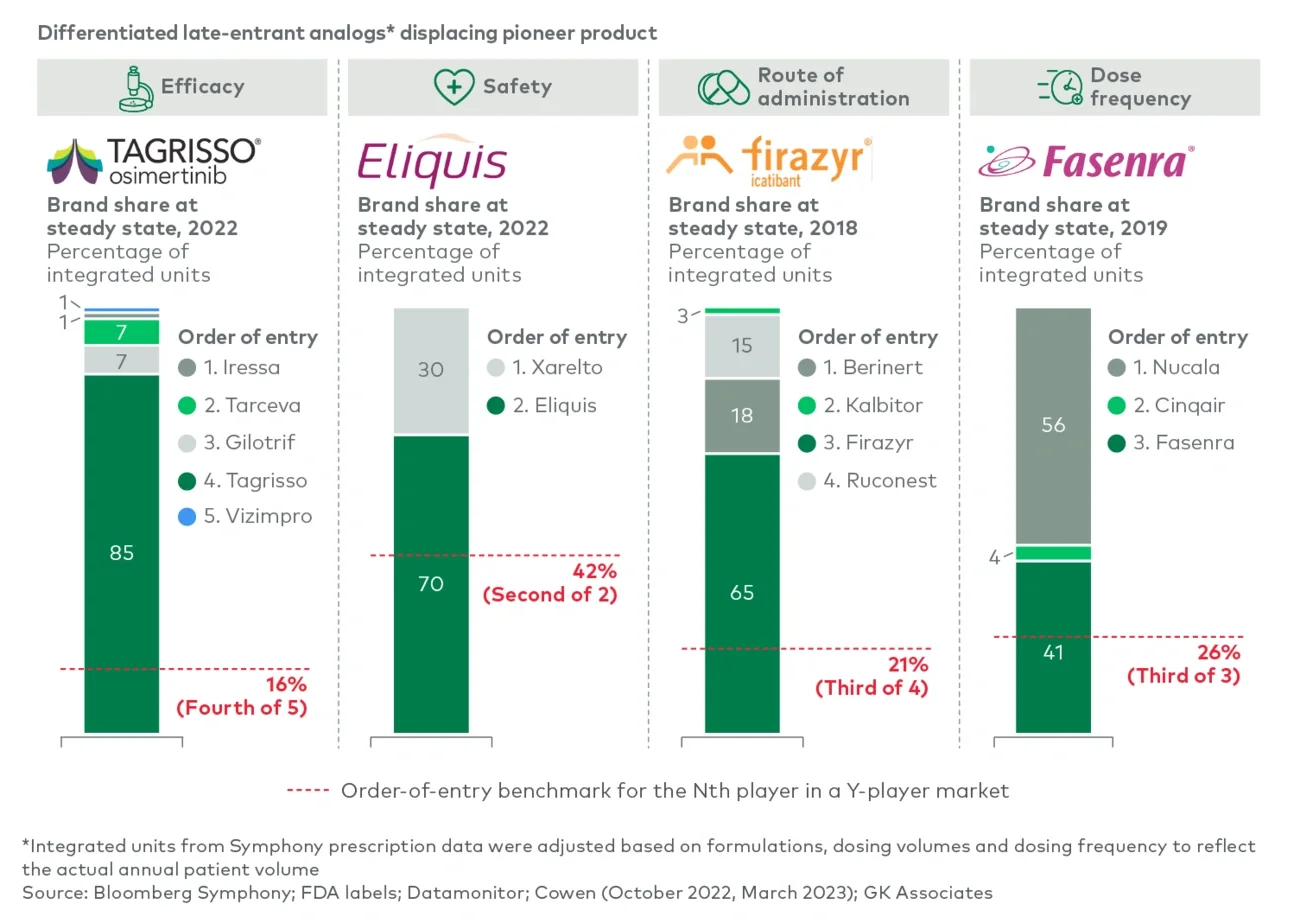

- Focus on differentiation that addresses an unmet need, not just numerical advantages. It is critical to understand which endpoints are valued and what performance is impactful if achieved. This can only be done through open and objective discussions with physicians, payers and patients.

- Do not rely on mechanistic rationale as the differentiator. While a difference in binding affinity could create promise of differentiation, commercial uptake will follow only if that mechanistic advantage drives better clinical performance on endpoints that physicians feel are important.

- Be honest about the probability of achieving the target product profile once performance thresholds have been defined. Often teams rely on traditional probability-of-success benchmarks, which typically reflect the probability of approval but not necessarily the probability of achieving a commercially successful product profile.

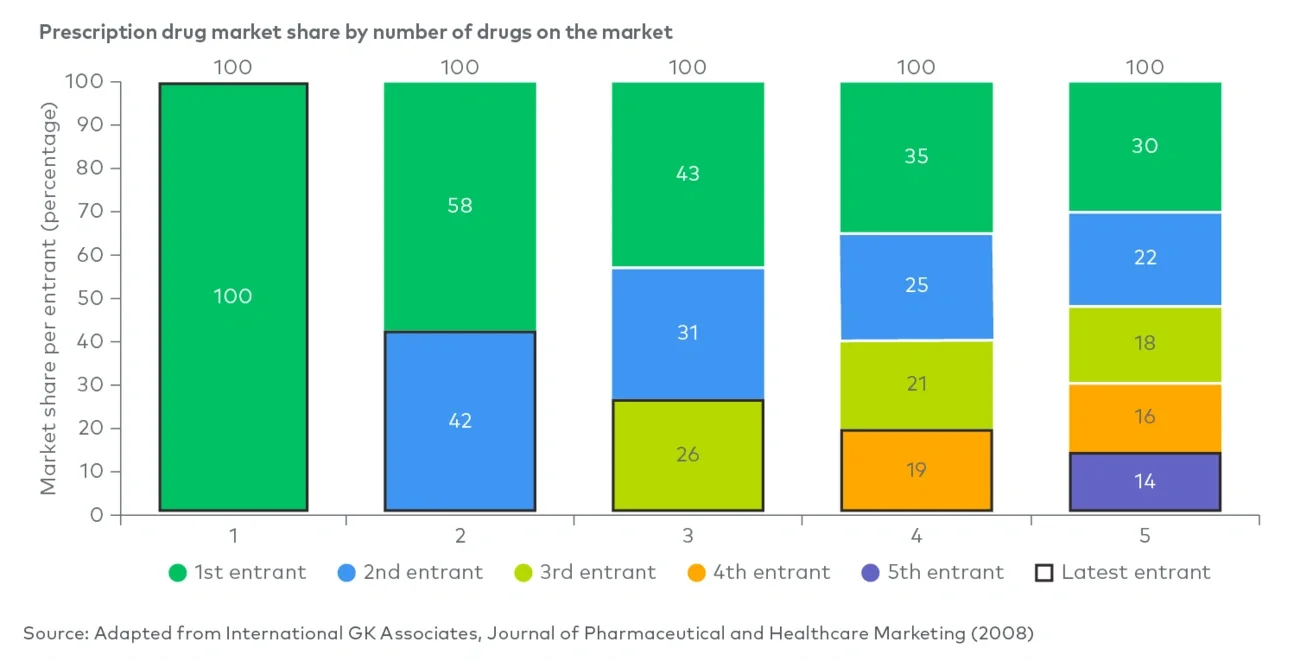

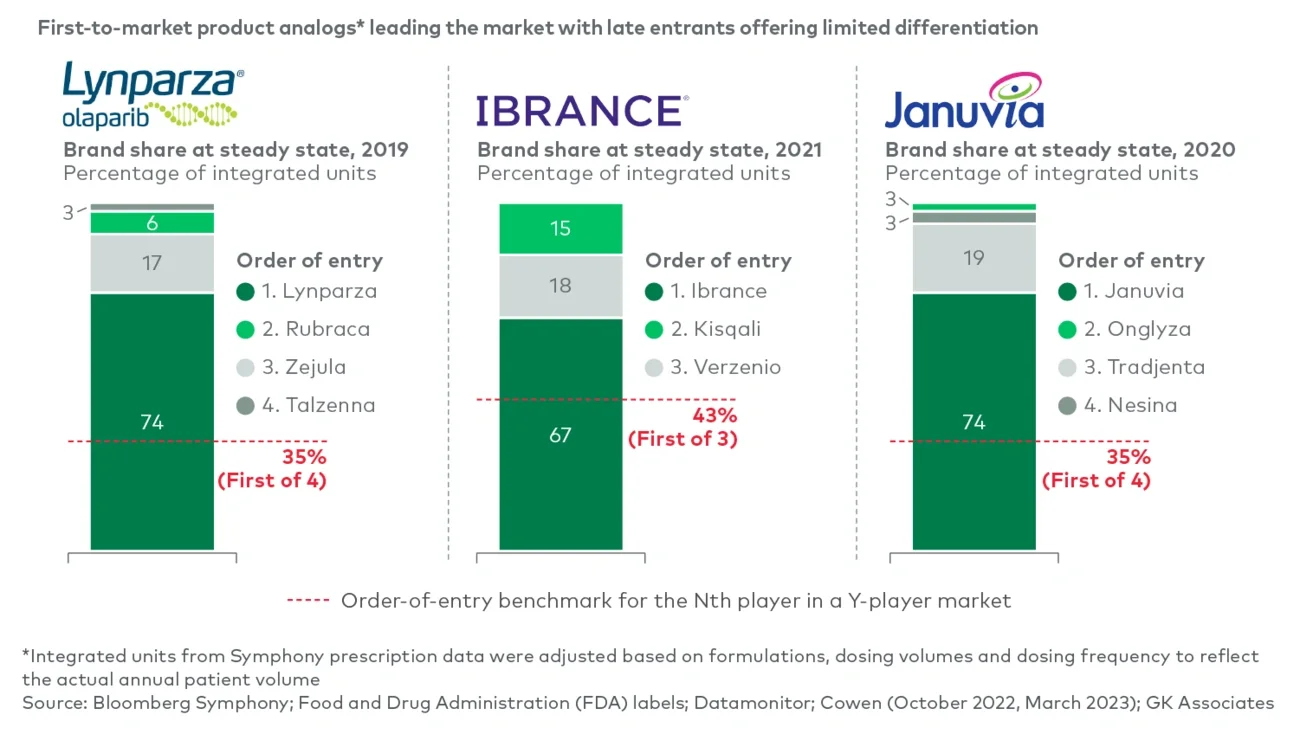

- Learn from analogs to sense-check assumptions. For instance, looking at analogs with our proprietary Launch Monitor tool would highlight that a 40% share estimate for a late-to-market product with only minor advantages in side effects physicians are not worried about should raise red flags.

We would like to thank David Knoff, Grace Mizuno and Jiayang Chen for their contributions to this piece.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC