Understanding the drivers of launch variability

We conducted an analysis of various factors that might influence the differences in launch performance across pharmaceutical companies. These factors included the diversity of therapeutic areas involved in launches, the order of market entry, decisions regarding co-promotion and pricing strategies. Interestingly, only two factors were found to be significantly linked to enhanced company launch performance: 1) a focus on launches within core therapeutic areas, and 2) proactive expansion in the early stages of the product life cycle.

The benefit of repeated launches in core therapeutic areas

In our analysis of top pharmaceutical companies, we observed a higher proportion of launches in core therapeutic areas, defined as areas where the company already had established revenue streams before the launch of a new product. Notably, 80% of the launches were in these core areas. These launches, encompassing 50 products, showed significantly higher average revenues per product compared to launches in noncore therapeutic areas — $670 million versus $280 million, representing a 2.4-fold difference. At the company level, this pattern persisted. The three highest-performing companies launched over 90% of their products into existing therapeutic areas. In contrast, the bottom three performers introduced 30% of their new products into areas outside their established core, highlighting a clear strategic divergence.

The benefits of introducing new products into existing therapeutic areas, where companies have established capabilities and stakeholder relationships, are clear. In these areas, companies can utilize their top talent, draw upon existing commercial infrastructure, leverage key relationships with stakeholders and apply insights from previous launches. Particularly important is the presence of an established commercial infrastructure that is scaled and customized to provider and patient needs, enabling accelerated launch uptake. Both the infrastructure and the experience also enable companies to foresee and navigate commercialization challenges, realign launch resources with anticipated commercial potential and capitalize on synergies with other products in their portfolio more effectively.

Yet this strategy of focusing on core therapeutic areas must be balanced with the need for diversification, especially as pharmaceutical companies grow and seek to expand beyond their primary, sometimes saturated markets. Diversification becomes crucial to sustaining growth and mitigating risks associated with overreliance on specific segments. This strategic consideration is underscored by the observation that lower-performing companies often suffer from a higher incidence of underperforming product launches, particularly in fields like anti-infectives, where they may lack established expertise and relationships.

As pharmaceutical companies consider which therapeutic areas to target for their forthcoming product launches, they may question whether certain areas are predisposed to greater success. According to our study, the choice of therapeutic area typically does not have a significant impact on the success of a launch. This finding indicates that the success of product launches depends less on the “where” — the therapeutic areas chosen — and more on the “how” — the strategy and approach companies employ in launching new products.

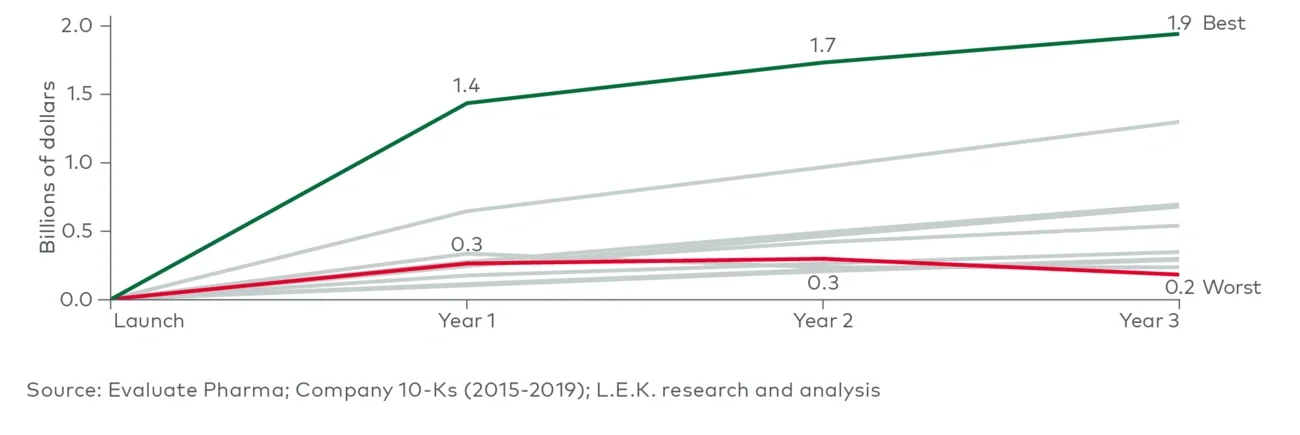

The need for early life cycle expansion

The strategic role of indication expansions in product strategy is essential. Companies that effectively invested in indication expansions, such as adding new lines of therapy, targeting different patient segments or addressing new diseases, consistently demonstrated higher average revenues. This trend is highlighted in the performance gap between the top and bottom companies: the top three performers averaged 1.4 extensions per product within three years of launch, while the bottom three managed only 0.4 extensions.

This significant difference emphasizes the critical impact of an early and well-planned product life cycle strategy, often entailing some level of preemptive investment to achieve outstanding revenue outcomes. Given equal circumstances, companies should give precedence to assets with the versatility to address multiple diseases. Investing early and accepting the associated risks in these programs can be more advantageous if the potential for incremental revenue justifies it, rather than adopting a cautious, phased approach.

These observations may need to be reevaluated considering the changes brought about by the Inflation Reduction Act passed in August 2022. The act’s introduction of Medicare price negotiation is perceived by many in the industry as akin to a loss of exclusivity event, mainly because there’s no minimum limit set for the prices Medicare can negotiate. This perception significantly impacts the time frame for recouping investments, consequently altering the return-on-investment calculations for indication expansions. Given that the window for generating substantial revenue is now further compressed, there’s growing skepticism within the industry about the viability of “pipeline in a product” investment strategies. Consequently, it’s leading to a reevaluation, with some suggesting the need to deprioritize certain indication expansion programs due to these altered financial dynamics.

Strategic implications

- Carefully manage the risks associated with therapeutic diversification: Pharmas will create more value when launching products in markets where they have established their brand, reputation and stakeholder relationships. Diversifying into new therapeutic areas needs to be carefully considered as it introduces inherent inefficiencies, and it necessitates the development of top talent and commercial infrastructure from the ground up rather than leveraging existing resources.

- Invest in early indication expansion: Indication expansions remain integral for strong performance. Companies must weigh the impact of the Medicare price negotiation from the Inflation Reduction Act as they consider portfolio investment decisions and indication expansion strategies early.

- Choose pharmaceutical partners with a proven launch track record: Biotech companies looking for pharmaceutical collaborators should prioritize partners based on their demonstrated success in product adoption and launch performance. This consideration is critical as significant future value, including milestones and royalties, hinges on the pharmaceutical partner’s capability to effectively execute the product launch. Hence, the track record should be a key factor alongside the potential deal terms.

The authors would like to thank Jenny Mackey, Franco Zambra, Hunter Tiedemann and Rylee Wander for their important contributions to this edition of Executive Insights.

For more information, please contact lifesciences@lekinsights.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC

Endnotes

1The 10 companies analyzed were the top 10 based on 2019 U.S. biopharma revenue.

2Contribution assumes total 2021 U.S. pharma revenues of ~$400B, based on U.S. medicine spending at estimated net manufacturer prices, from “The use of medicines in the U.S. 2022” IQVIA report.

3Includes innovative, branded products (new molecular entity and original biological product approvals from the Center for Drug Evaluation and Research; innovative products approved by the Center for Biologics Evaluation and Research) from 2015 to 2019. Reformulations, biosimilars and generics were excluded. Products provided for free access or sold as generics soon after launch were excluded. Products without reported Evaluate Pharma revenues for year three were excluded.