Combination vaccines now occupy a prominent role in many vaccine manufacturers’ pipelines, with six of the seven leading vaccine manufacturers investing through R&D and M&A (see Figure 1).

Executive Insights

Combination Vaccines: Converting Clinical Promise Into Commercial Scale

Combination Vaccines: Converting Clinical Promise Into Commercial Scale

July 11, 2025

Key takeaways

Adult combination vaccines face complex commercial hurdles beyond safety and efficacy, including policy alignment, economic value and multistakeholder buy-in across patients, payers, providers and policymakers.

Pharmacies, payers and providers may have conflicting motivations that undermine adoption, necessitating tailored strategies to ensure economic and operational viability across the ecosystem.

While paediatric combos thrive due to aligned stakeholder incentives and established immunisation schedules, adult vaccines confront behavioural hesitancy, fragmented delivery infrastructure and declining compliance — especially evident post-COVID.

Relying on paediatric playbooks is insufficient; success in adult combos demands customised commercial models, rigorous demand testing, robust HEOR evidence, pricing innovation and policy engagement to navigate a complex, evolving landscape.

Figure 1

Presence of combination vaccines in the pipeline of top vaccine players

Image

The prize is clear: an effective seasonal combination vaccine could tap into the $7 billion-plus global influenza vaccine market, and by boosting compliance among under-immunised segments, it may even expand the market.

While the headline benefits — streamlined schedules, fewer injections and improved adherence — seem clear on paper, real-world uptake in the adult segment remains largely untested. Adult vaccines, particularly those targeting healthy, working-age cohorts, face low baseline compliance and behavioural hesitancy, setting a high bar for commercial viability.

Layered onto the political headwinds that marked the early Trump era, these factors demand a disciplined, evidence-led appraisal of the pathway to commercial scale.

In this Executive Insights, we dissect the critical success factors and key implications for vaccine manufacturers.

Success hinges on more than clinical performance

To succeed, adult combination vaccines must overcome challenges that extend beyond clinical efficacy. These include:

- Policy alignment: are national immunisation schedules and regulatory guidance harmonised across target pathogens and age groups?

- Clinical and economic comparability: do combinations match monovalents on safety and efficacy, and can they offer price parity or cost-effectiveness to secure broad market access?

- Stakeholder buy-in: are patients willing to be vaccinated with each antigen, and are the incentives of patients, payers, providers, pharmacists and policymakers aligned?

Paediatric combination vaccines have achieved sustained commercial success by addressing operational constraints in immunisation delivery while maintaining strong safety and efficacy profiles. Market share dominance in both high-income (hexavalent, more than 70% share) and low-to-medium income (pentavalent, more than 85% share) countries demonstrates their long-term strategic value

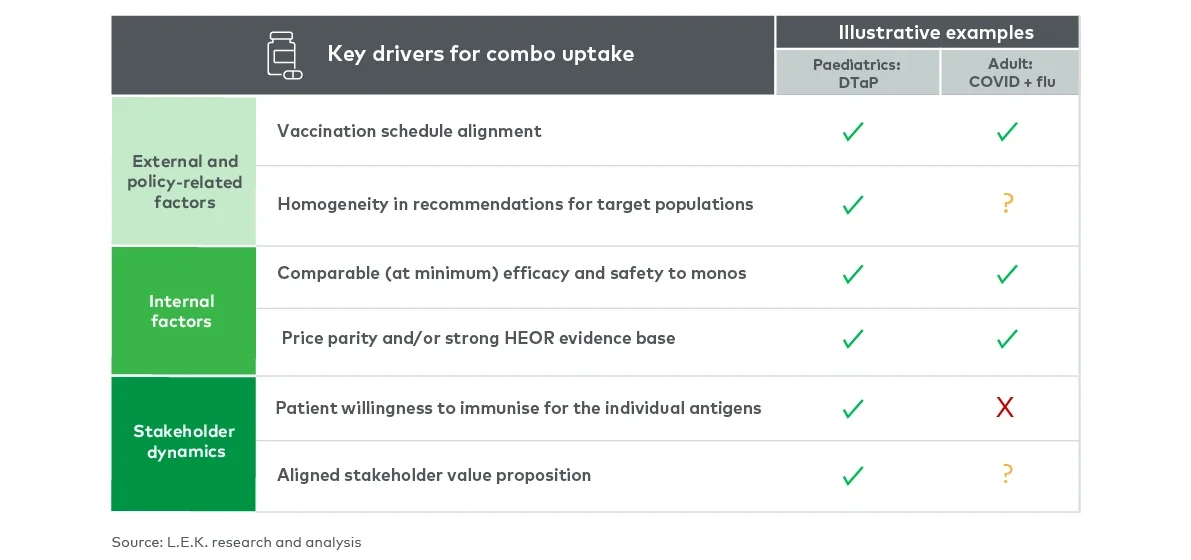

However, a side-by-side look at established paediatric combinations and the top adult candidates in development uncovers several differences (see Figure 2). To account for these differences, vaccine companies will need to deploy a different commercial strategy and mindset to achieve success in the adult combo space.

Figure 2

Key drivers for combo uptake: paediatric vs adult

Image

Combo vaccine uptake starts with behavioural buy-in

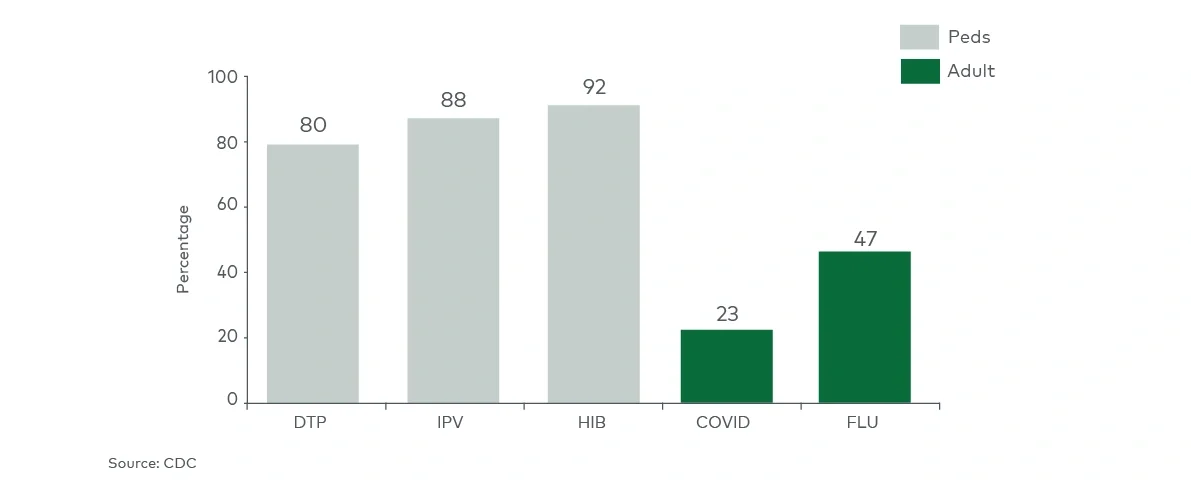

Hexavalent formulations that combine diphtheria, tetanus, acellular pertussis, inactivated poliovirus, Haemophilus influenzae type b and hepatitis B have dominated the infant market in most high- and many middle-income countries since their rollout in the early 2000s. Before their arrival, these six antigens were administered via four separate injections, all of which had strong vaccination rates at the time of the combos’ launch. For instance, DTaP coverage exceeded 90% in the US before hexavalent combos entered the market.

The behavioural contrast between the paediatric market and its adult counterpart is stark. The adult respiratory market has proven much more complex and fragile. COVID-19 vaccine administration in the US has plummeted from more than 5,000 doses per million people daily in 2021 to fewer than 50 daily in 2024. This decline suggests a sceptical and disengaged adult population, creating structural headwinds that manufacturers must address through education, engagement and access strategies.

Misaligned incentives could stall market adoption

Unlike in paediatrics — where payer support, provider schedules, patient acceptance and public health priorities and policy are largely synchronised — adult seasonal vaccines sit at the intersection of competing stakeholder agendas (see Figure 3):

- Patients appreciate the convenience of one shot, yet many are reluctant to take ‘extra’ antigens they view as nonessential (as illustrated in the COVID-19 example above).

- Providers must navigate different immunisation schedules and the different choices and variations of combinations available, adding complexity to point-of-care counselling and inventory trade-offs.

- Payers could see budget pressure if combos lift vaccine coverage rates, even at price parity, due to increased vaccination rates (VCR). Persuasive health economics and outcomes research (HEOR) evidence will therefore be critical to secure broad access and reimbursement.

- Pharmacies are typically paid per administration, so fewer injections may erode margins. Without revised fee structures, their incentive to stock and promote combos may be limited.

- Policymakers will need to consider real-world feasibility (e.g. alignment of combos with national immunisation schedules, strain update cadence, national health priorities and public sentiment towards individual components).

Figure 3

US adult vs paediatric vaccination rate (pre-combo launch)

Image

The launch context for future combination vaccines varies significantly, and some might have an easier road than others. For instance, adolescent vaccination, particularly in the realm of sexual health where there is an established schedule and existing infrastructure for HPV immunisation, or vaccines aimed at the older adult population where there is greater alignment around the need to vaccinate, could drive greater alignment among stakeholders. However, improving the health of the adult population — particularly in disease areas where political or other factors have created uncertainty around the need for vaccination — may present more complex challenges for combination strategies.

Manufacturers may need to rethink the commercial playbook

Simply relying on the paediatric combo playbook will not suffice. Manufacturers must pressure test the commercial rationale and share uptake expectations for each potential combination. If this assessment and/or our framework above reveal any critical gaps — such as lower-than-expected patient demand, uncertain payer support or policy misalignment — manufacturers should revisit their commercial strategy and/or investment levels accordingly.

To ensure commercial success, manufacturers may need to navigate specific challenges which require additional investment and a novel approach, including:

- Carefully evaluating real-world demand scenarios: if patient demand or stakeholder alignment is weak, reassess go-to-market strategy and/or investment scale.

- Tailoring commercial model: higher investment in educational campaigns and HEOR data may be needed to drive demand for combos with one or more lower-priority antigens.

- Planning for a competitive and dynamic landscape: expect direct competition (same target antigens), indirect overlaps (e.g. flu + COVID-19 vs flu + RSV) and displacement by incumbent monovalents.

- Adopting fit-for-purpose pricing strategies: budget-conscious stakeholders will demand robust HEOR evidence and cost-effectiveness modelling that supports pricing expectations.

- Shaping the policy environment: engage proactively on reimbursement models, pharmacist administration fees and tender-based procurement advantages.

The need for different commercial models and tactics, layered on top of potentially higher R&D outlays under evolving US policy and regulatory requirements, could tighten profit and loss headroom. Success will depend on disciplined portfolio prioritisation and innovative commercialisation tactics that concentrate resources where combination vaccines demonstrably move the needle.

Outlook: targeted investment and strategic discipline will define winners

Combination vaccines are a strategic opportunity, but not a guaranteed success. Their fate in the adult market will depend on behavioural insights, economic incentives and regulatory coordination.

Those who lead will be the ones who align stakeholder interests, deliver persuasive value propositions and invest with surgical precision. In a market constrained by platform complexity and commercial headwinds, clarity — not breadth — will distinguish market leaders from followers.

Contact us for a further discussion.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting

Questions about our latest thinking?

Questions about our latest thinking?

Related insights

You might also be interested in these insights.

English