The year 2021 brought tremendous progress to the biopharma industry. Nearly 5 billion people have now been at least partially vaccinated against COVID-19 worldwide, the first ever in-human data showing safety and efficacy of in vivo CRISPR gene editing was published, and 128 therapeutic-focused biopharma companies went public globally.

Going forward, biopharma executives will face challenges and should embrace transformation across many dimensions, including commercialization, financing and portfolio planning. This report shares highlights from five trends that are having the greatest impact on the industry:

-

Growth of the advanced modality pipeline

-

Continued global pricing pressure

-

Evolving commercialization models

-

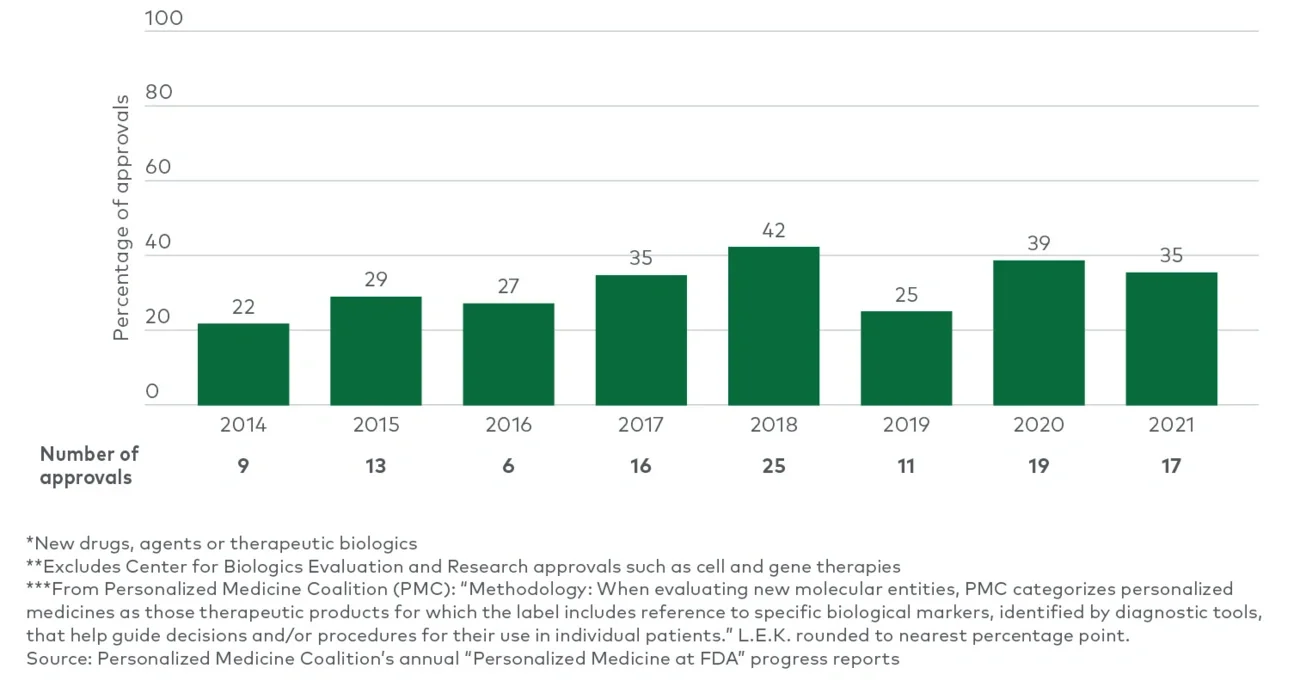

Increased patient diagnosis and biomarker initiatives

-

Evolving financing landscape

L.E.K. Consulting has developed its analysis based on global events and developments currently impacting the biopharma landscape and the key trends to watch:

Growth of the advanced modality pipeline

The advanced modality pipeline has grown rapidly in the past five years, and 2021 marked another “year of firsts” for advanced modalities. China approved its first CAR-T therapy, the first BCMA-targeted CAR-T therapy was approved in the U.S., and Intellia announced the first positive human data for CRISPR in vivo gene editing. A record $23.1 billion was raised in the areas of gene therapy, cell immunotherapy/cell therapy and tissue engineering. Clinical, regulatory and commercial milestones in 2022 will shape the trajectory of an increasingly diverse advanced modality pipeline.

Key developments to watch include the following:

-

Gilead’s Yescarta and Bristol Myers Squibb’s (BMS) Breyanzi are racing to bring CAR-T to earlier lines of large B-cell lymphoma treatment. Gilead filed regulatory submissions for second-line use with both the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA) and other regulatory authorities, and BMS filed a submission for second-line use with the FDA. Approvals would expand the market potential of these therapies.

-

There are only two approved gene therapies in the U.S., but multiple times that number may reach regulatory milestones this year. For example, Bluebird is awaiting FDA review of biologics license applications for beti-cel gene therapy for transfusion-dependent β-thalassemia and eli-cel for cerebral adrenoleukodystrophy (CALD), and BioMarin’s valoctocogene roxaparvovec for severe hemophilia A is being reviewed by the EMA and the company expects to submit to the FDA this year. Other planned or potential FDA and/or EMA submissions include CRISPR and Vertex’s CTX001 for transfusion-dependent β-thalassemia and severe sickle cell disease, and CSL Behring and uniQure’s etranacogene dezaparvovec for severe to moderately severe hemophilia B. The decisions will set precedents for the safety and efficacy needed to support approval. The therapies’ next steps in gaining market access, manufacturing at commercial scale and driving adoption will also be instructive for the field.

-

The reinvigoration of the RNA therapeutic pipeline will likely continue in 2022. Expected late-stage readouts include Alnylam’s RNAi Onpattro in transthyretin amyloidosis with cardiomyopathy (ATTR-CM) and Ionis and AstraZeneca’s antisense oligonucleotide eplontersen for hereditary ATTR polyneuropathy (hATTR-PN). In addition, the pipeline could expand its focus in mechanisms like RNA editing, tRNA, circular RNA and mRNA.

-

Biopharmas are increasingly looking at protein degradation to destroy disease-causing proteins previously believed to be too difficult to pharmacologically target by using small molecules such as proteolysis-targeting chimeras (PROTACs). The preclinical- and clinical-stage protein degrader pipeline increased by nearly 70% from 2020 to 2021,1 and 2022 should be a year of continued progress.

The developments listed above are by no means comprehensive. For example, we also expect to see continued investment in allogeneic cell therapy and rapid growth in the Chinese cell and gene therapy pipeline. But they demonstrate clear advancements — from exploring new mechanisms to expanding to new diseases to accelerating in new geographies and setting critical precedents in the path to commercialization.

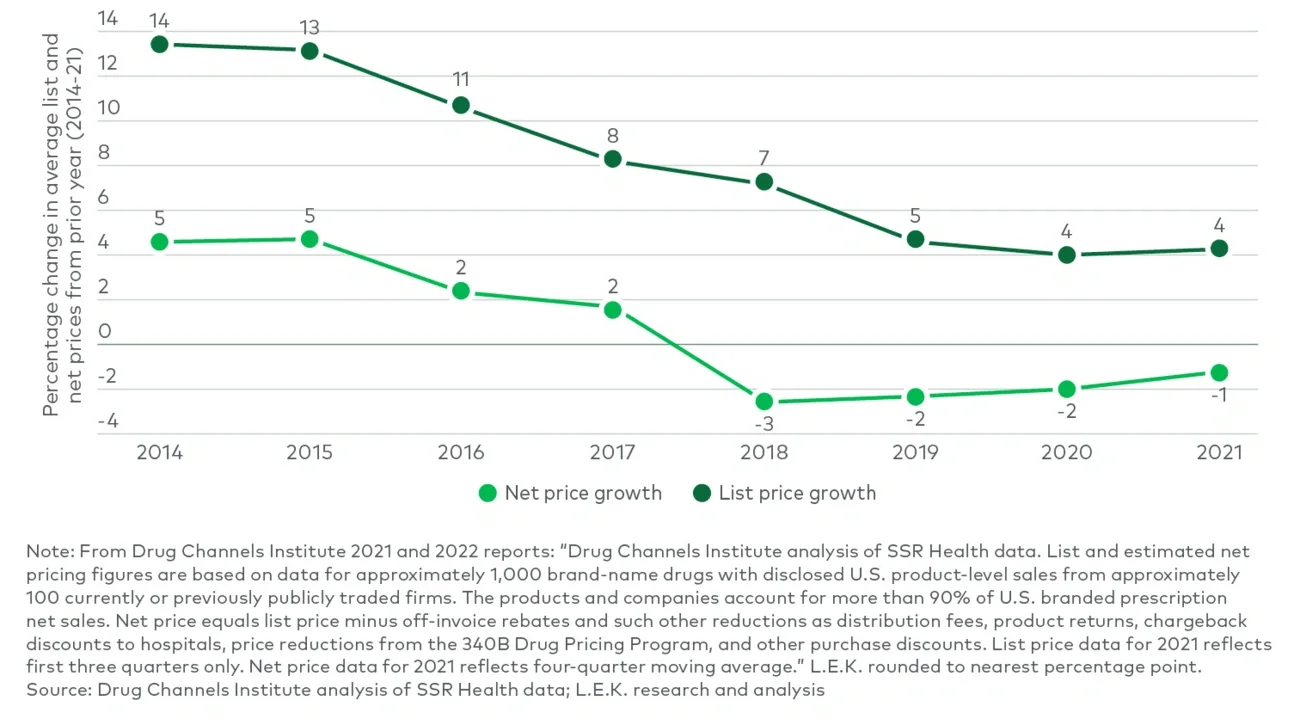

Continued global pricing pressure

Governments, payers and consumers continue to place pressure on drug prices across the globe. In the U.S., pharmacy benefit managers (PBMs) and payers are negotiating more significant discounts, with declining net prices since 2018 despite list price increases (see Figure 1). Payers also are continuing to restrict coverage of therapies they deem too expensive; the Centers for Medicare & Medicaid Services’ (CMS) recent proposed coverage restriction of Aduhelm to clinical trial patients is just one example. Pricing pressure may also come from new competitors within the industry. EQRx, the first of a potential wave of companies with disruptive “low-cost, me-too” strategies, intends to price its therapies 50%-70% lower than competitors’ pricing. It has assembled a pipeline of at least five clinical assets and has partnerships or memoranda of understanding (MOUs) with CVS Health, Geisinger, Blue Shield of California, BlueCross BlueShield of North Carolina, Horizon and NHS England. The timing of its first filings remains to be seen, as their current pivotal trial data for two lead assets is from Chinese studies and U.S.-based studies are planned to begin this year. Additionally, the biosimilar pipeline is accelerating and may soon provide increased competition to numerous blockbuster franchises.