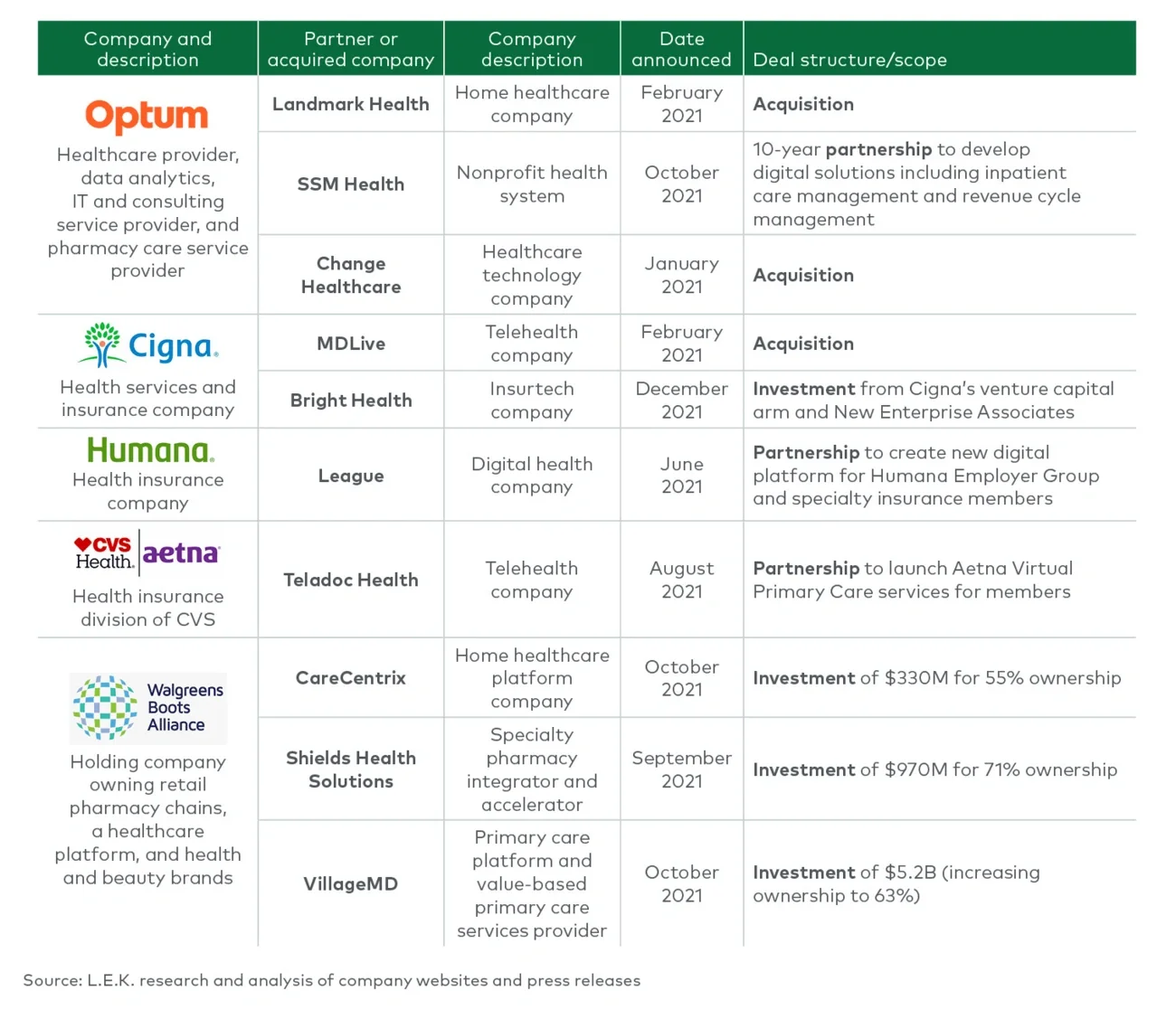

There are opportunities for additional providers to enter the telehealth space. CVS and Aetna’s partnership with Teladoc and Cigna’s acquisition of MDLive are good examples of this. Telehealth’s growing popularity will no doubt spur more activity in the future.

Adoption of real-time clinical data solutions

As aggregators of healthcare data, payers are increasingly understanding and acting on their ability to leverage real-time clinical data to inform clinical decision-making and care management. Payer analysis of data has historically generated lagged insights, and has predominantly, or exclusively, relied on claims data. While payers have tried to introduce real-time checks such as home visits, nothing comes close to the accuracy and precision of going straight to the source — clinical data residing in electronic health record (EHR) systems. As such, there has been increased demand for companies that offer EHR data extraction/abstraction services to help set future expectations. Companies such as DataLink and Health Catalyst help extract/abstract data from EHRs, and others such as Cotiviti and Q-Centrix (reporting/compliance focused) and MedeAnalytics and Truven Health Analytics (business operations focused) help provide real-time analytics services.

Providers also see great value in gaining access to real-time clinical data. On top of providing quality reporting data and servicing medical record requests, EHR data extractions/abstractions also help with real-time care management and coordination. Companies such as CarePort Health, Lightbeam Health Solutions and Aledade enable providers to better define and measure population health initiatives aimed at improving outcomes and lowering costs, and also to aggregate data to enable seamless transitions of care. Further, there are growing applications to leverage EHR data in continuous clinical surveillance, which may help screen out false alarms in patient monitoring devices or reveal subtle trends about a patient’s health early on.

There is room to innovate, however. Within current offerings, payers and providers are seeking the ability to create more detailed and customized reporting, increase interoperability across EHR platforms, further data standardization in order to increase efficiency, and increase overall automation. Additionally, payers demand the ability to build a longitudinal member dataset that provides a comprehensive member medical history over time and can therefore enable more effective care management interventions, as well as low-latency clinical data (ideally, real-time data) to enable more timely care and streamline back-office processes. However, providers have not been eager to share access to clinical data due to concerns around federal laws restricting release of medical information and competitive rate sensitivities.

There is power in harnessing real-time clinical data. Doing so informs payers of ways to drive down costs and improve patient outcomes, and aids in providers’ clinical decision-making and population health management. Payers and providers are truly in a unique position, given their ability to leverage EHR data and stakeholder relationships and fortify their role in care coordination, to create a more powerful, data-driven picture of each patient’s condition and thus improve their overall care journey.

Conclusion

Healthcare in the U.S. is always changing. Some of the changes represent a steady march over the years, such as the ongoing dominance of managed care in Medicare and Medicaid, the move toward lower-cost sites of care, payers diversifying into the provider space and the expansion of behavioral health models. All of these trends will continue. But this year we will see, in particular, that health systems will continue to confront staffing shortages, unconventional partnerships will become the norm, VBC will see rapid growth beyond primary care, in-home and virtual visits will become a permanent fixture of the landscape, and real-time clinical data solutions will be adopted at an increased pace. L.E.K. closely monitors these trends and helps companies navigate the evolving healthcare landscape to build winning strategies.