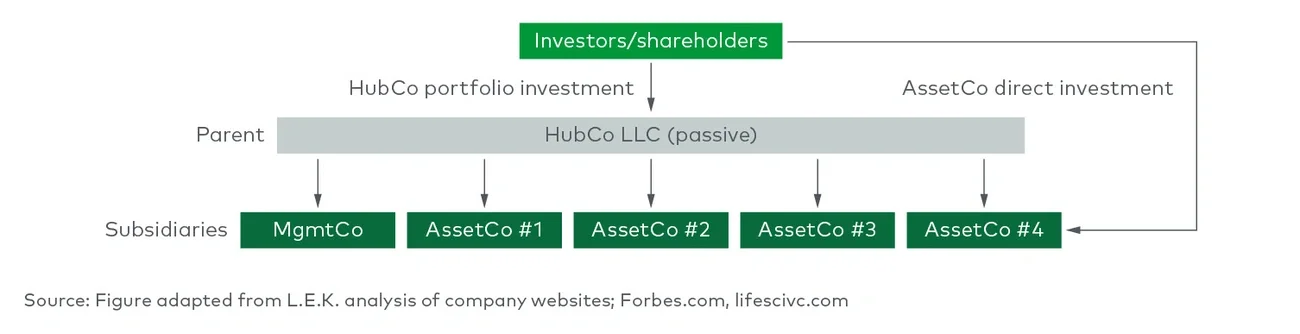

While the past few years have seen a high volume of initial public offering (IPO) activity throughout the biotech sector — particularly during 2020 and 2021 — in the near term, funding for biotech companies is likely to come increasingly from private and alternative sources. This shift in investor focus may lead biotech firms to consider evolving their business models to ones that allow for greater flexibility in fundraising, in order to attract this type of investor.

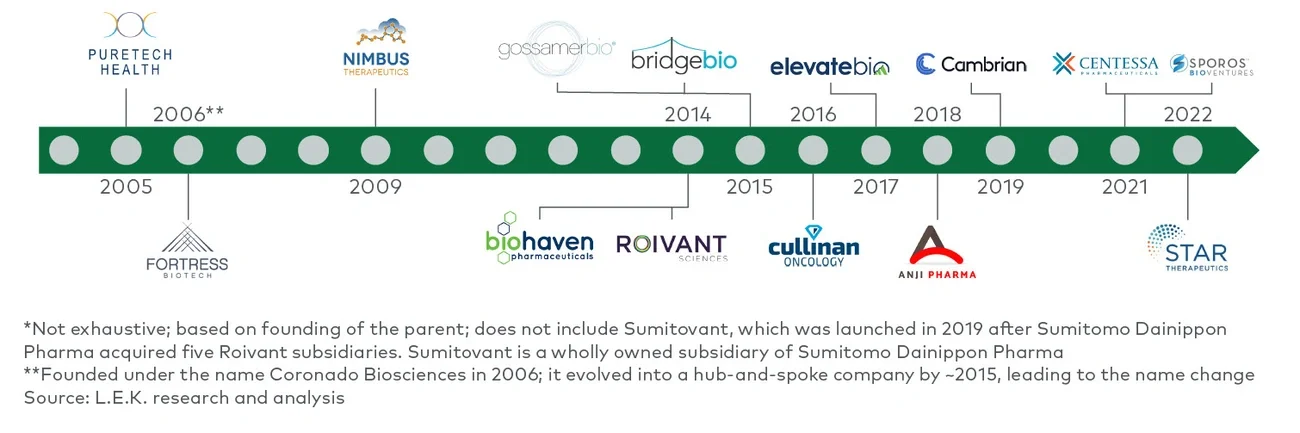

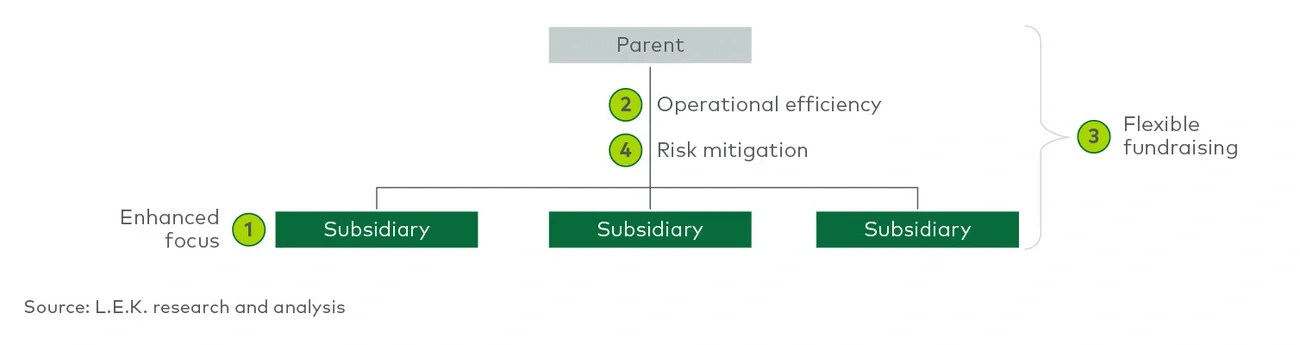

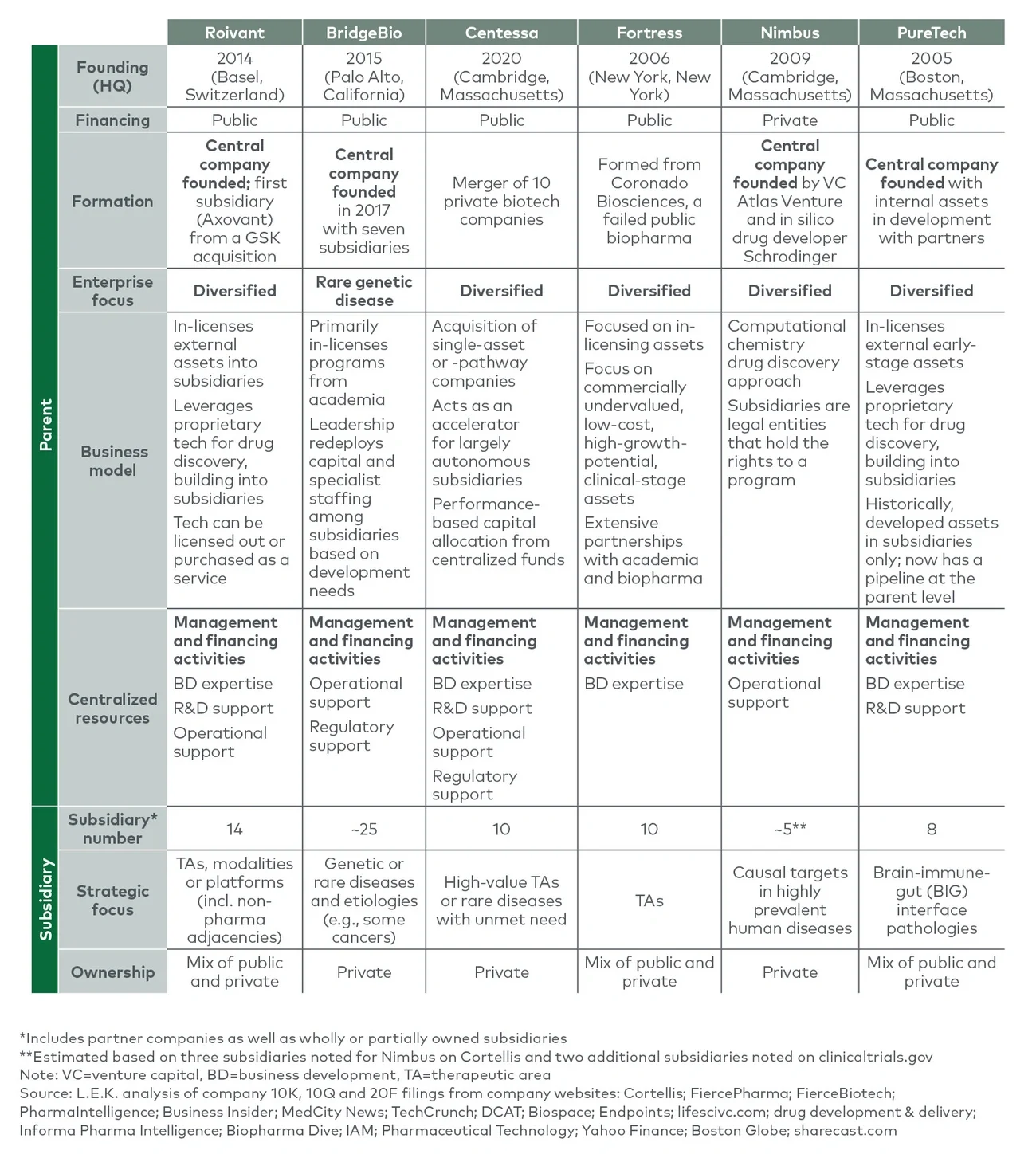

As “hub-and-spoke” business models have emerged within biopharma (see Figure 1), so has the potential need for alternative funding approaches. Hub-and-spoke model companies use a centralized portfolio management team (the parent company) that owns and controls a set of subsidiaries. The subsidiaries remain focused on their asset(s), program(s) and therapeutic area(s), while the parent company provides centralized leadership and resources to subsidiaries across therapeutic areas, indications and/or technologies. Subsidiaries may be spun out from the parent or aggregated. For example, Roivant began by purchasing shelved assets from pharmas and then spinning out subsidiaries (Axovant first). Conversely, Centessa was formed through the aggregation of 10 private biotech firms, each focused on a single asset or biological pathway. There may be variations on this theme and different names used to describe the models (e.g., “portfolio model,” “LLC holding company model”); in this Executive Insights, L.E.K. Consulting considers these companies more generally.