At 11 billion US dollars, India is the fourth-largest MedTech market in the APAC region. Despite per capita spend being low compared to other APAC markets, positive news is that per capita healthcare spend in India has grown rapidly, especially in recent years. Compared to the present figure of US$74, average healthcare spending per capita was US$49 as recently as 2012, implying a CAGR of nearly 4%. Rising affordability and expanding insurance coverage are primary contributors to the growth in healthcare spending. IN addition, growth of the MedTech sector can further fuel growth in healthcare spending.

Rising affordability

Rising affordability for quality healthcare is driven by India’s rising per capita disposable income, which reached US$2,900 in 2023-24, growing by 8% in FY24 and 13.3% in FY23. In line with rising affordability, growth in India’s household spend per capita at 7.8% Y-o-Y, is forecasted to outpace that of fellow developing Asian economies such as Indonesia, Philippines and Thailand.

Besides rising income, other factors contributing to rising affordability are a) large youth population — the median age in India is 29.8 years in 2024, as per The World Factbook, compared to 40.2 in China and 49.9 in Japan, and b) ongoing urbanization.

Rising insurance coverage

The proportion of India’s population not covered by any form of health insurance has fallen considerably from 63% in FY2014-15 to 30% in FY2021-22. This has mainly been due to expanding health insurance, both public and private. Among government schemes, where population coverage has increased from 25% to 51% during the same period, Pradhan Mantri Jan Arogya Yojana (PM-JAY) has been a key contributor. With 550 million identification cards issued, it is the world’s largest government-sponsored healthcare program. The latest government data shows that the scheme has facilitated 71 million hospitalizations. In a significant move, the Union Cabinet has approved expansion of the AB PM-JAY, ensuring all senior citizens aged 70 and above receive health coverage, regardless of income. Meanwhile, private health insurance coverage has also increased by 4%, registering a 23% CAGR over the past decade.

The growth in overall healthcare spending, driven by rising affordability and better insurance coverage, is expected to spill over into the Indian medical devices market and support in its expansion.

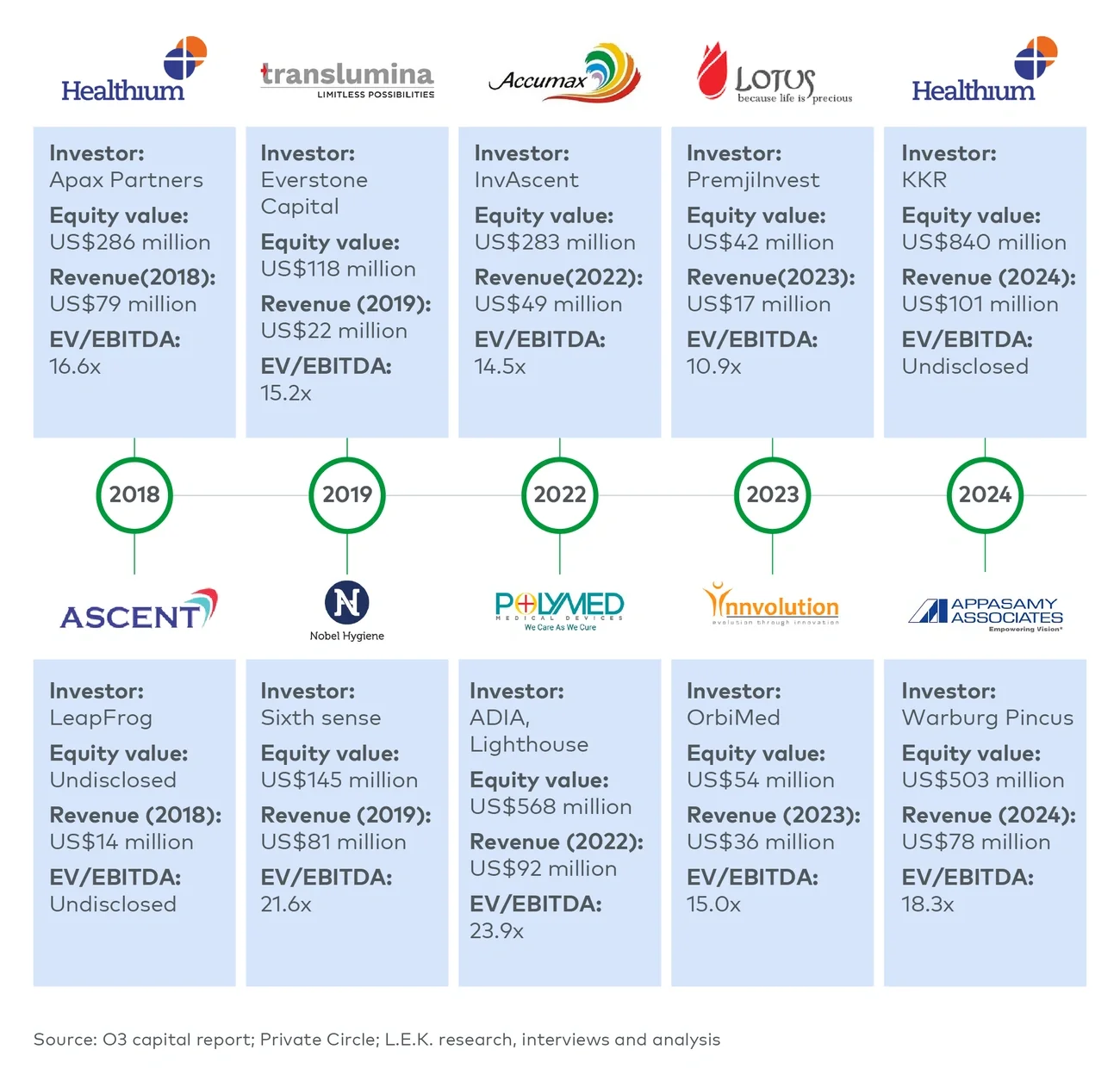

Primarily, a) increasing focus among Indian MedTech manufacturers on R&D and innovation to develop high quality products that meet market needs in both domestic and international markets, b) supportive MedTech manufacturing ecosystem, driven by supportive govt. policies, talent availability and infrastructure that has the capability and capacity to serve both Indian demand and international markets via exports, and c) capital infusion by public and private sector to aid companies to expand capacity, diversify portfolio and strengthen marketing efforts, have the potential to create multiple $billion revenue MedTech companies in India.

We will touch upon each of these key points in detail in the sections below:

A. MedTech innovations

Overview of the MedTech market in India

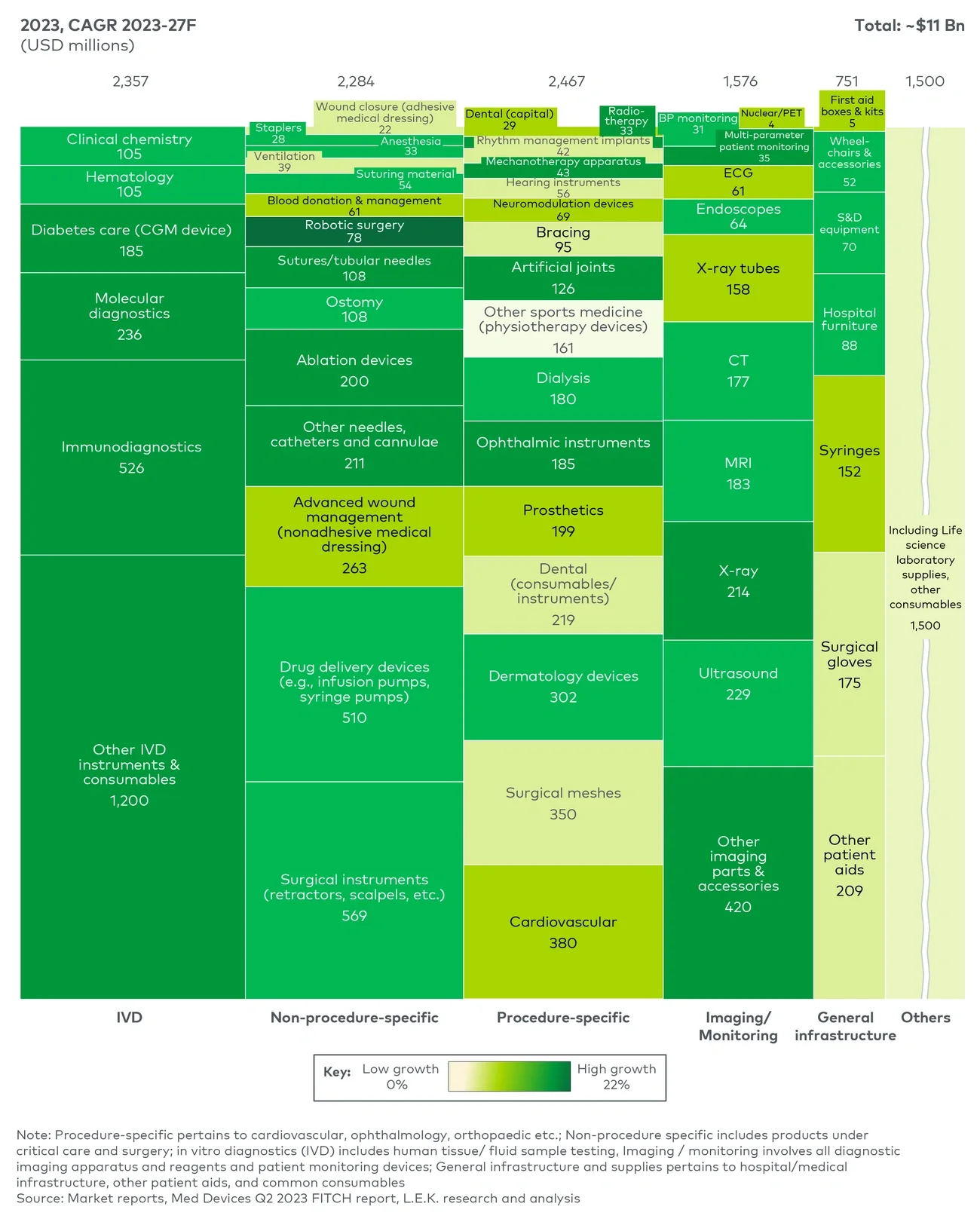

The MedTech market in India can be divided into five broad categories:

- Invitro diagnostics (IVD) that revolves around disease diagnosis and preventive care using human tissue/fluid sample

- Procedure-specific devices that are used for medical intervention specific to a therapeutic segment (e.g., cardiology, ophthalmology, dentistry, etc.)

- A wide range of non-procedure-specific devices that are used to perform surgeries and medical interventions across multiple therapeutic areas

- Imaging and monitoring devices designed either to visualize structures and organs within the body for diagnostic/therapeutic purposes or for patient monitoring

- General infrastructure and supplies that pertain to an extensive list of essential products used for the overall functioning of healthcare facilities, supporting routine and emergency medical care

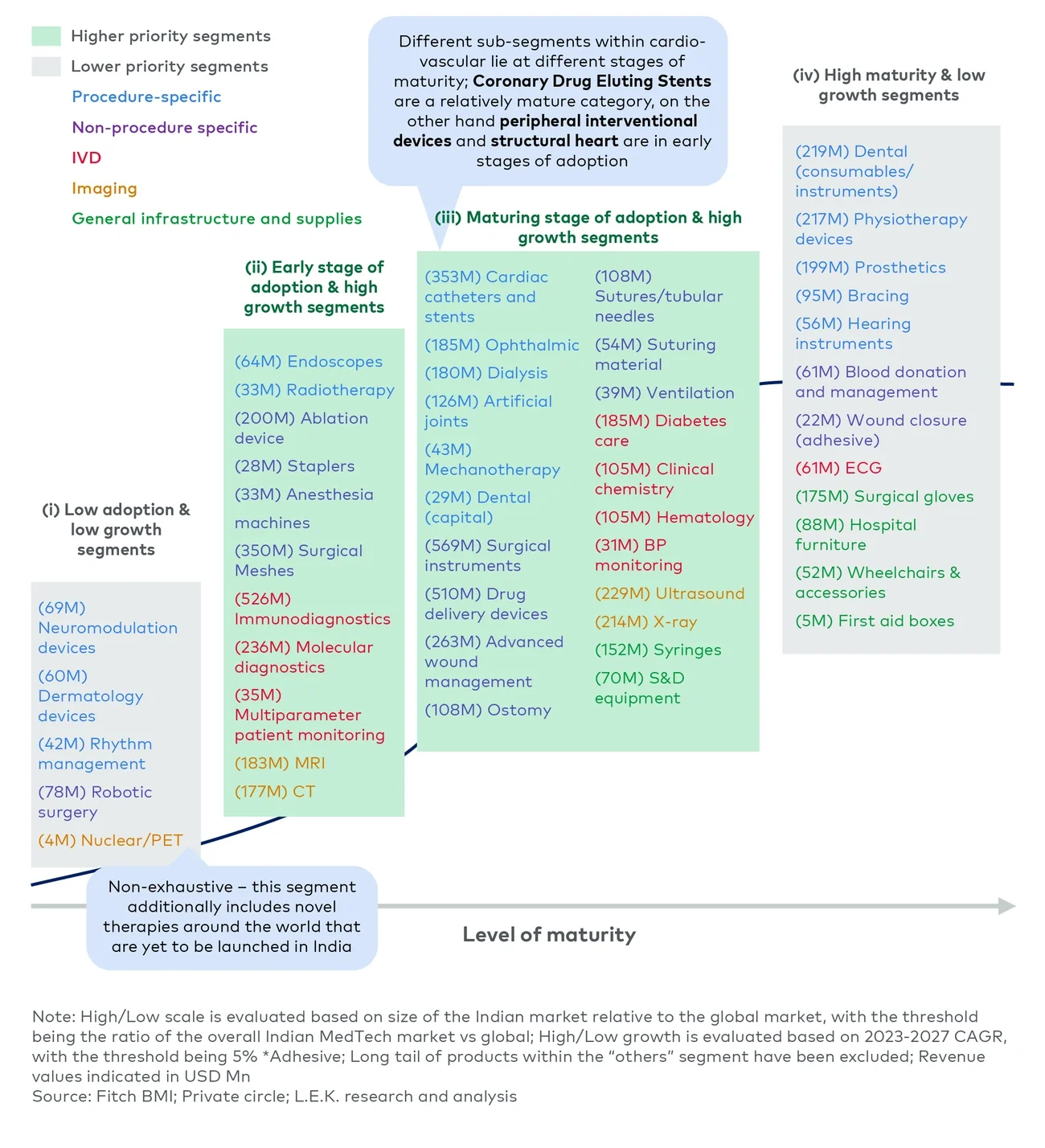

Out of these, invitro diagnostics used by diagnostic laboratories, hospitals, research institutions, clinics, and POCT providers, is the largest and fastest-growing segment, followed by surgical instruments and consumables (see figure 1).