Introduction

While first-to-market biopharma products in a new therapeutic class are often seen as having a clear competitive advantage, recent trends tell a more nuanced story.

Over the past decade, around half of all innovative branded biopharma launches have been second or later entrants within their therapeutic class (late entrants). Some have successfully reshaped the standard of care — offering superior efficacy, safety and/or convenience — and have achieved strong commercial performance. Others, however, have struggled to gain traction, falling short of expectations with disappointing sales and minimal market impact.

As competition within therapeutic classes intensifies, critical questions emerge: When does it make strategic sense to develop a late entrant — and when is it simply too late? More importantly, what factors determine success for those entering an already-crowded field?

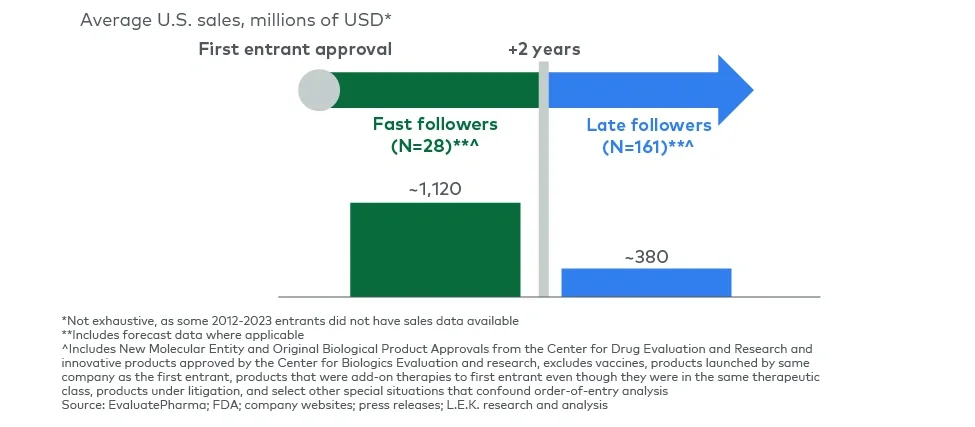

Followers fare better within two years of first launch

In the first two years following the launch of a new therapeutic class, the treatment landscape remains fluid, with physician adoption still evolving. This period offers fast followers — those entering the market within two years after the first-in-class entrant — a strategic window to capitalize on market dynamics and shape prescribing habits. With a stronger clinical profile, fast followers can capture substantial market share and, in some cases, even outperform the first-in- class entrant.

As time passes, physician and patient familiarity and comfort with early entrants tend to deepen, leading to entrenched prescribing habits and growing loyalty to established brands. This creates a high barrier to entry for later competitors, which must offer a clearly differentiated value proposition to displace existing treatments. As a result, fast followers outperform late followers significantly, achieving nearly three times the average sales (see Figure 1). This performance gap underscores the importance of timing, strategic positioning and rapid execution in competitive therapeutic classes.