Previous attempts to assess R&D productivity often suffered from outdated data, opaque methodologies or limited scope, focusing on a small subset of companies. However, with the biopharma industry undergoing significant shifts, it is more critical than ever to adopt a current and transparent approach to understanding how R&D productivity is evolving.

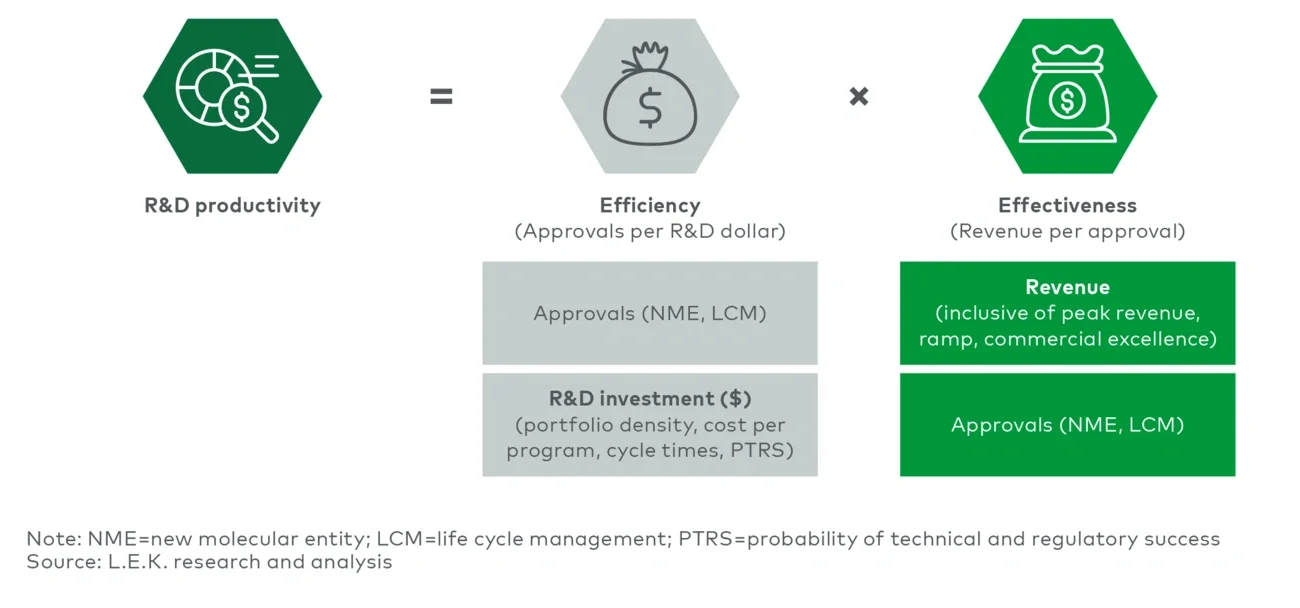

In this edition of L.E.K. Consulting’s Executive Insights, we explore the two key components of R&D productivity and compares R&D efficiency and R&D effectiveness between Top 15 Biopharmas by revenue and the remainder of the industry (smaller companies).1

Such insights are essential to inform and optimize R&D strategies in this dynamic landscape. By understanding the nuances of R&D productivity across different segments of the industry, leaders can leverage mutual strengths to enhance productivity and navigate the evolving challenges and opportunities in drug development and commercialization.

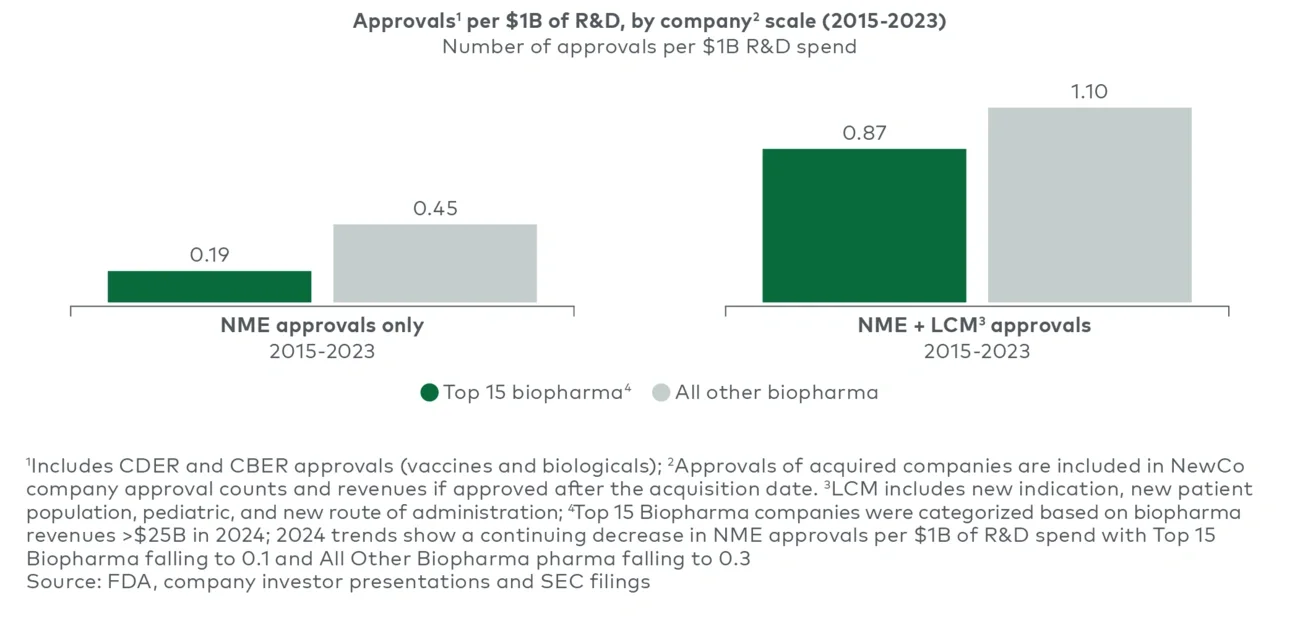

Smaller companies surpass large pharmas in R&D efficiency

Despite remarkable advances in science, technology and operational practices, the consensus within the biopharma industry is that R&D productivity has been steadily declining. This trend is evident in the widening gap between industry R&D expenditures and revenue growth over the past decade. This situation stems from a steady decline in efficiency, a trend that has persisted over the past 50 years.

A major factor behind the decline in R&D efficiency is the escalating complexity of clinical trials. The scale and scope of these programs have expanded significantly, driven by evolving regulatory demands and a rapidly changing global clinical trial landscape. This has led to longer trial durations, greater enrollment challenges and higher investment costs. Consequently, the number of new approvals per R&D dollar has decreased over the past few decades.

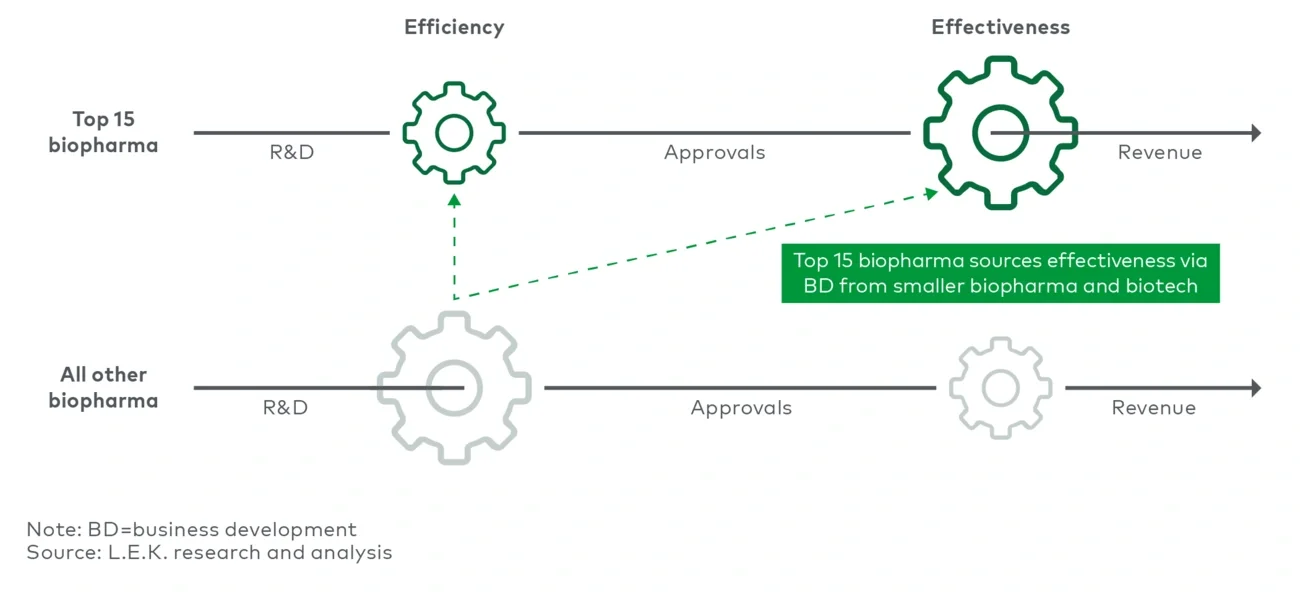

Interestingly, large pharmas have been less efficient at converting R&D investments into new drug approvals compared to the rest of the industry (see Figure 2). Even when factoring in life cycle indications, the efficiency disparity remains evident, although less pronounced.

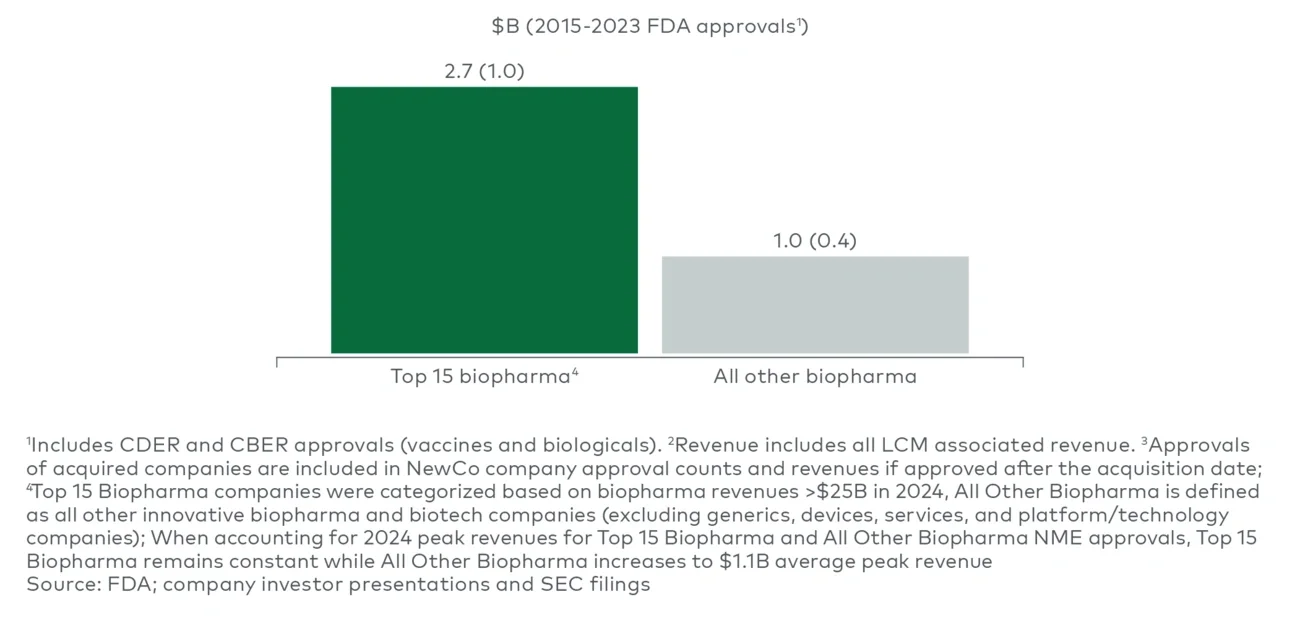

This is partly driven by their reliance on outliers — mega-blockbuster drugs such as Keytruda, Humira and Dupixent, among others — to drive top-line growth. To meet stringent internal revenue and return-on- investment thresholds, large pharmas concentrate their efforts on programs with the highest market potential, which typically have more life cycle management opportunities. While such drugs deliver transformative value, they also significantly raise the bar for R&D investments, demanding substantial financial resources and time to achieve market success. This heavy focus on blockbuster outcomes often leads large pharmas to prioritize effectiveness — producing high-impact, high-revenue therapies — at the expense of efficiency, limiting the number and diversity of opportunities pursued within their R&D investments and reducing the potential efficiency of their R&D portfolios in addressing broader medical needs.