In the fifth installment of our outlook on how COVID-19 will impact the advertising industry, we analyze potential scenarios for the print advertising industry. Each advertising format will be affected differently, and it is important to understand the historical relationships between each format and broader economic conditions in order to assess potential recovery scenarios.

In this article, L.E.K. Consulting analyzes future scenarios for print advertising, including looking at its historical relationship with U.S. GDP, and forecasts potential growth trajectories — ultimately drawing out strategic implications for the format.

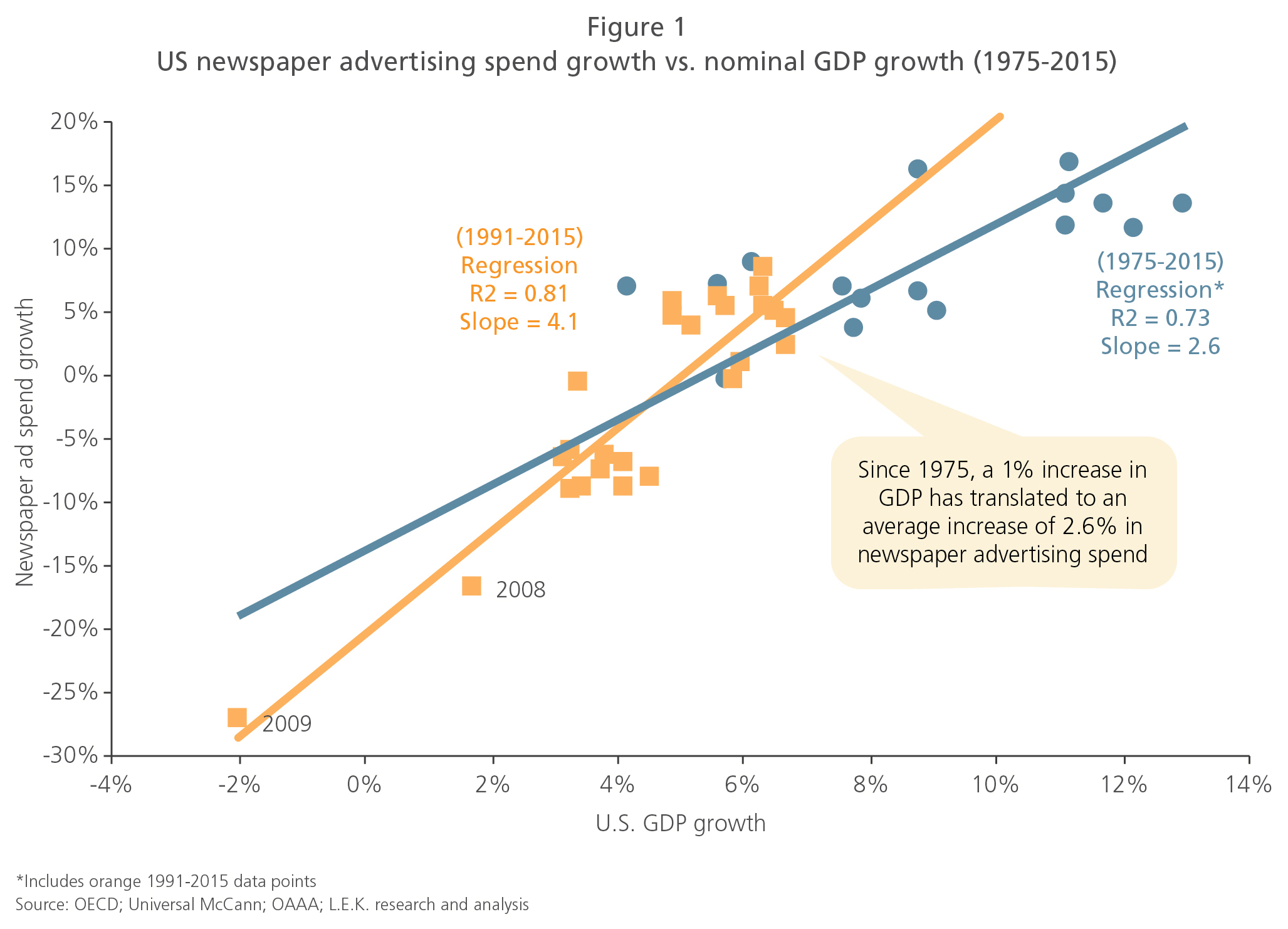

US print advertising spend closely tracks GDP growth

The print advertising industry is the ad format that is most highly correlated with growth in U.S. GDP, an ominous sign for an industry that has seen revenues continue to decline even during the post-Great Recession boom. The correlation registers at R2 = 0.81 over the last 30 years, implying that GDP is the main driver of growth in print advertising.

Moving forward, print advertising may be particularly challenged. The 2008-09 recession represented a reset in print advertising, and it has yet to return to 2007 levels. Further, print has continued to decline in recent years as advertisers shift dollars to digital formats with better targeting and measurement capabilities.

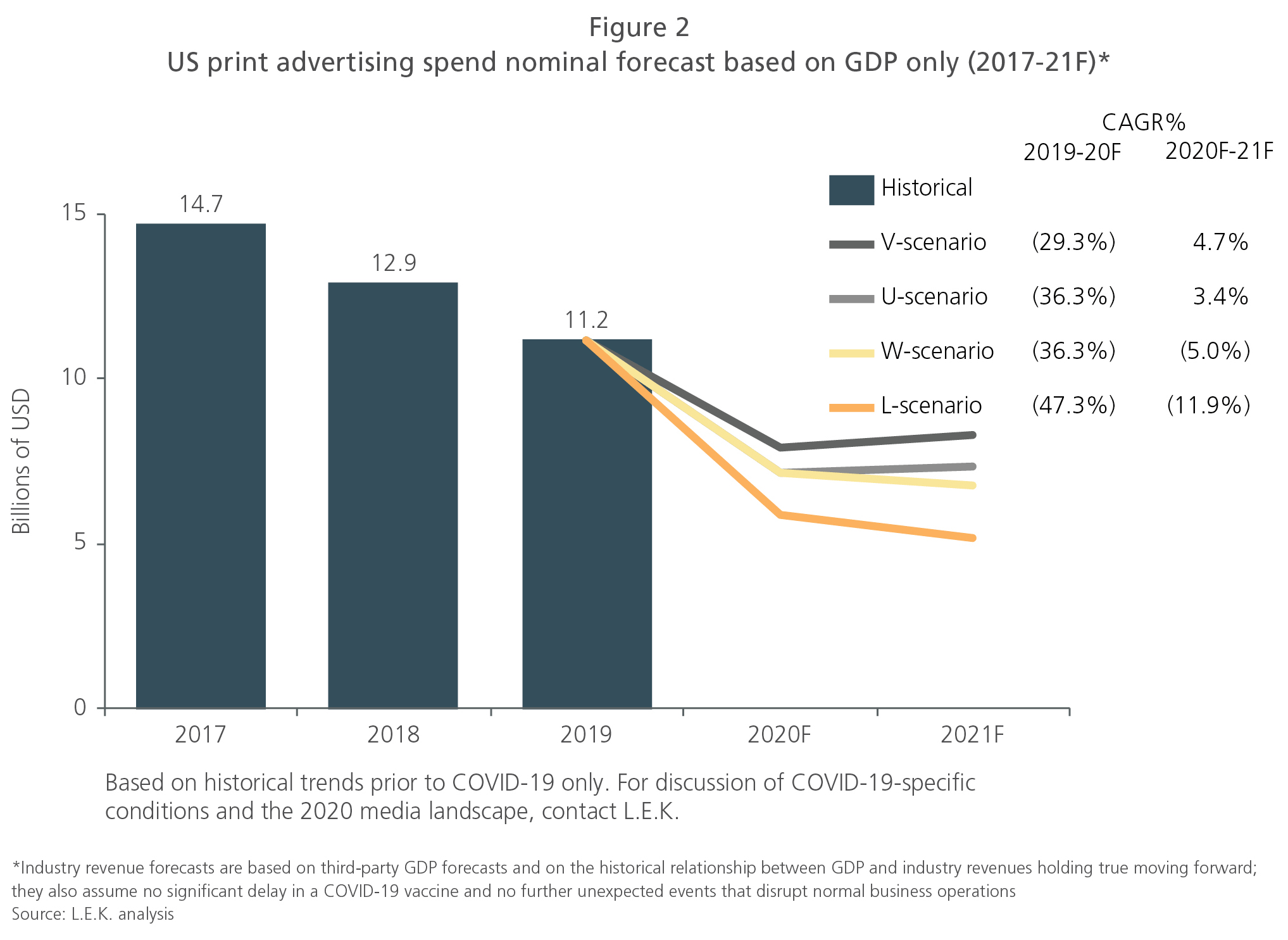

If GDP forecasts and past relationships between GDP/advertising hold, print ad spend is unlikely to reach 2019 levels by 2021

The various consensus scenarios for GDP produce highly variable print ad spend projections, though all project that spend will not return to 2019 levels by 2021.

In the most optimistic scenario, print ad spend is projected to decline 29.3% in 2020, then recover and grow 4.7% in 2021 for an overall CAGR of -14.0% from 2019-21.

Under the U-shaped recovery, ad spend is projected to decline 18.9% p.a. 2019-21.

However, things could be much worse: The W-shaped and L-shaped recoveries project overall declines of 22.2% and 31.9% p.a. 2019-21, respectively.

Given the variability of the projections, what strategic considerations should advertisers keep in mind?

Key takeaways and strategic considerations

Print advertising is in secular decline — The Great Recession accelerated the decline of print that was already taking place. Expect more of the same from print this time around.

Print is local — Print relies on local businesses, which have taken some of the biggest hits from COVID-19. Expect print advertising to remain adversely impacted so long as local businesses remain under stress.

Time vs. dollars — The share of time spent consuming print media remains lower than the share of advertising dollars spent on print. The Great Recession resulted in a big correction, but the comparison of share of time and share of dollars indicates further room to correct.

01272022090155