The advertising agency ecosystem is undergoing another major transformation, comparable to past waves of change such as the dot-com era, the rise of programmatic advertising and the social and mobile booms. What was once a fragmented sector led by creatives is now a battleground for scale, efficiency and tech-fueled performance.

Several factors are responsible: changing consumer behavior, the rise of self-serve tools from platforms such as Google and Meta, and the adoption of programmatic buying and generative artificial intelligence (AI). These trends have reduced marketers’ reliance on traditional agencies while raising expectations for what agencies must deliver. In response, many brands have adopted a growing mix of vendors across media, creative and analytics.

To keep up, marketing leaders have leaned into specialist firms that offer deeper expertise in specific areas. But that shift has introduced new complexity, triggering a familiar cycle: Brands unbundle to access niche capabilities, rebundle to regain efficiency and then add more partners as needs evolve.

How agencies are responding

Four distinct agency models are taking shape. Each reflects a different approach to integration, scale and specialization:

- Holdco consolidation: Legacy giants like Omnicom and IPG are pursuing scale-driven mergers to compete with consultancies and digital platforms.

- Agile challenger networks: Midsize groups such as Stagwell and Attivo are positioning themselves as faster-moving, tech-forward alternatives.

- PE rollups: Private equity (PE) firms are assembling multicapability platforms by combining creative, digital and/or performance agencies.

- Focused specialists: Typically, PE-backed firms super-serve specific customer segments or verticals, like small and medium-size businesses (SMBs) or regulated industries.

Here’s an in-depth look at each of these models as agencies and investors reposition to remain competitive.

Holdco consolidation: Scale plays from the top

The IPG-Omnicom merger (the first major tie-up among top-tier holding companies in years) is progressing toward completion, having received U.S. Federal Trade Commission approval in June 2025. The move reflects how agency giants are responding to growing competitive pressure on two fronts:

- Digital platforms like Google, Meta and Amazon increasingly enable brands to bypass agencies entirely by controlling vast swaths of premium inventory (accounting for over 50% of global digital ad spending in 2025).

- Large consultancies such as Accenture are challenging agencies by offering integrated marketing solutions that combine strategy, technology and execution.

The deal’s genesis reveals the pressure legacy holdcos face: IPG CEO Philippe Krakowsky initiated strategic talks in July 2023 after recognizing that creative strength alone couldn’t offset eroding client budgets and competitive advances. After rejecting proposals from PE and other strategic players, IPG found its match in Omnicom’s technology-first approach.

The combined entity expects $750 million in annual cost savings while creating a $25 billion revenue giant that would rival Accenture Song, the marketing services division of Accenture. If approved, the merger could trigger industry realignment as rivals like WPP, Publicis and Dentsu face pressure to pursue their own consolidation moves, potentially squeezing midsize independents while creating opportunities for boutique agencies to continue to position themselves as nimble alternatives.

Agile challenger networks: Midsize groups on the rise

As legacy holdcos pursue scale-first rebundling, midsize networks like Stagwell and Attivo are thriving with a different approach: agile rebundling. This model combines broad, integrated capabilities with founder-led cultures and faster speed-to-market.

Stagwell

Stagwell (NASDAQ: STGW) bills itself as “the challenger holding company built to transform marketing.” Stagwell has set a goal to double revenue from $2.3 billion to $5 billion by 2029, with a strategy focused on tech-driven acquisitions and partnerships. Its 2024 purchase of UNICEPTA brought AI-powered media intelligence into Stagwell’s Marketing Cloud, while a partnership with Palantir expanded its AI-enabled marketing capabilities.

The results are promising. The Marketing Cloud division posted 31% year-over-year growth in fiscal year 2023, and four of its agencies (72andSunny, Anomaly, Code and Theory, and GALE) earned spots on Ad Age’s 2025 Agency A-List.

Attivo Group

Founded in 2020 and backed by private equity, New Zealand-based Attivo has built a multicapability network through strategic acquisitions. It represents a new wave of players capitalizing on legacy holdcos refocusing their portfolios. Attivo has acquired established agencies like Hill Holliday and Deutsch NY from IPG, picking up heritage brands the larger holdco could no longer efficiently manage.

Attivo’s May 2025 acquisition of AI-powered agency The Next Practice illustrates how quickly these networks can integrate new capabilities.

Stagwell and Attivo, along with others like S4 Capital, The Brandtech Group and Dept, are part of a broader wave of midsize challengers redefining the agency model. These firms are drawing clients away from both global holdcos and niche independents by combining integrated capabilities with greater speed, flexibility and tech fluency. Some are also rethinking how services are delivered. S4 Capital, for example, has moved from billable hours to output-based pricing as AI reshapes the economics of creative and production work.

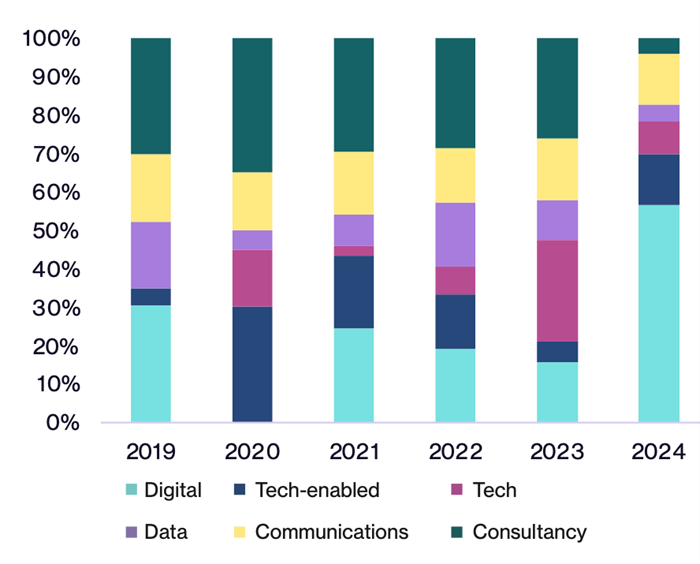

PE rollups: Building value through portfolios

Private equity activity in the agency world has accelerated, with the number of business-to-business services deals (including agencies, consultancies and tech providers) rising 21% year over year in 2024. According to SI Global’s second annual Private Equity Insights Report, more than 50 PE firms now actively target the space. Many are pursuing rollup strategies to build full-service marketing platforms by combining boutique creative shops, digital specialists and performance firms into nimble, integrated networks.

Source: SI Global, May 2025

Platform investment activity rebounded in 2024, with a sharp increase in the number of deals, especially in digital businesses. More than 50% of new investments went to firms categorized as “digital,” a broad label that includes everything from influencer agencies to digital transformation consultancies. While social and influencer marketing remains in demand, many PE firms are building platforms around specific verticals or service areas such as SMB-focused solutions, financial services or retail media.

Recent moves like IPG’s sale of R/GA to Truelink Capital, Huge’s sale to AEA Investors and Svoboda Capital’s investment in Highdive reflect how PE firms are actively reshaping their marketing services portfolios. Huge’s post-acquisition merger with Hero Digital shows how quickly these platforms can pivot toward high-growth areas: 62% of Hero’s clients now use AI or generative AI in their projects, up from just 25% in June 2024.

Focused specialists: Doubling down on a segment

Some PE firms are backing more focused and scalable agency models, investing in businesses with depth in a specific customer type, channel and/or vertical:

- Vertical specialists: These platforms focus on industries where domain expertise and, in some cases, compliance-ready solutions create strong defensibility and retention. Examples include Scorpion and FMG Suite, which deliver tech-powered marketing tailored to home services and legal professionals, among others.

- SMB-focused providers: These platforms typically serve SMBs through subscription-based marketing solutions that combine digital presence, customer relationship management systems and performance tools. Hibu is one example delivering these services efficiently through automation and centralized operations.

- Other focused models: A third category includes platforms built around distinct distribution strategies, such as white-label solutions for agencies or channel-focused models that serve intermediaries like resellers or media partners. These approaches often emphasize scalability through partner networks rather than direct client acquisition.

What this means for investors and operators

For investors, the most attractive platforms demonstrate strong client retention, differentiated capabilities, a clear view of their target segments and the ability to scale efficiently. While PE firms are working to moderate entry prices, competition from more than 50 active investors continues to keep multiples high. Tech-enabled agencies remain a focus, often commanding premium valuations due to their perceived scalability and performance upside.

Each of the four segments presents opportunity, but none is without risk:

- Consolidated holdcos must integrate sprawling networks while preserving creative strengths, managing client conflicts and aligning legacy tech stacks. The failed Publicis-Omnicom merger highlights these challenges, and the proposed IPG-Omnicom deal may face similar hurdles.

- Agile challenger networks benefit from speed and integration but risk overextending lean teams or diluting their edge as they grow.

- PE rollups require stitching together firms with different systems, cultures and models, making careful integration critical.

- Focused specialists must prove that depth in a single vertical or offering can scale without sacrificing flexibility or margin.

Even with strong strategy and execution, agency M&A often falters without client durability, as many firms still rely on individual relationships rather than institutional ones. Investors should look for signs of embeddedness — cross-selling, account growth and multithreaded ties — to ensure clients stay long enough to realize full value.

The next phase of agency evolution

The agency model is being rewritten. Investors are no longer rewarding size for its own sake. They are looking for platforms that scale efficiently, retain clients and deliver results.

Winning firms are moving fast — automating workflows, aligning services with how brands buy and focusing on customer segments where they can lead. Models built around real client outcomes — and not legacy structures — will define the next generation of agency platforms.

Next in this series, we’ll explore what truly makes an agency defensible in today’s market, from proprietary tech to institutional client depth, as consolidation reshapes competitive dynamics.

To learn more about how L.E.K. Consulting helps investors and operators navigate agency M&A, contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC