As the advertising industry struggles through the COVID‐19 pandemic, questions abound about what the future holds, how deep the decline will be, and how quickly the industry may bounce back. In this article, L.E.K. Consulting dives into the historical relationship between GDP and advertising, looks at lessons learned from the Great Recession in order to assess what the future holds for the U.S. advertising industry, and explores the following questions:

- How strong is the relationship between advertising and the rest of the U.S. economy?

- How did ad spend on different types of media perform during the Great Recession?

- Which media are best positioned moving forward?

- What are projections for future advertising spend?

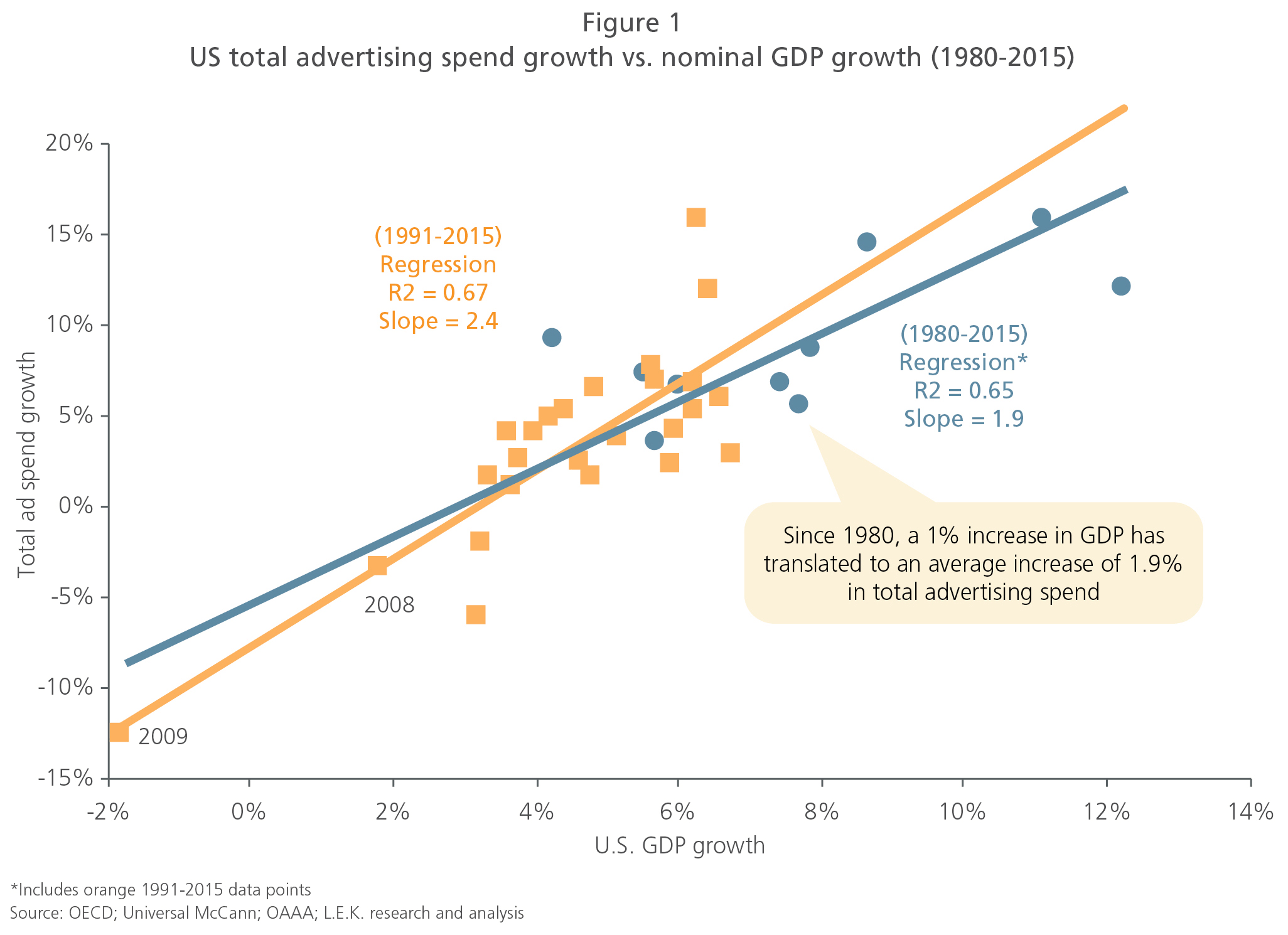

US advertising spend closely tracks GDP growth

Growth in U.S. GDP and total advertising spend has been highly correlated for the last 40 years (R2 = 0.67). That spells bad news for advertising in 2020.

The COVID‐19 disruption has touched nearly every segment of the economy. U.S. GDP contracted at a seasonally adjusted annual rate of 4.8% in Q1 2020, the biggest drop since Q4 2008, despite the fact stay-at-home orders only began to roll out across the country in mid‐March. The outlook for Q2 is even more dire, with some economists forecasting much larger declines.

The good news is that the correlation between GDP and advertising works both ways. In every recession since 1981, U.S. ad spend has recovered quickly to prerecession levels. However, all mediums are not created equal and the shape of the economic recovery will impact the recovery of ad spend.

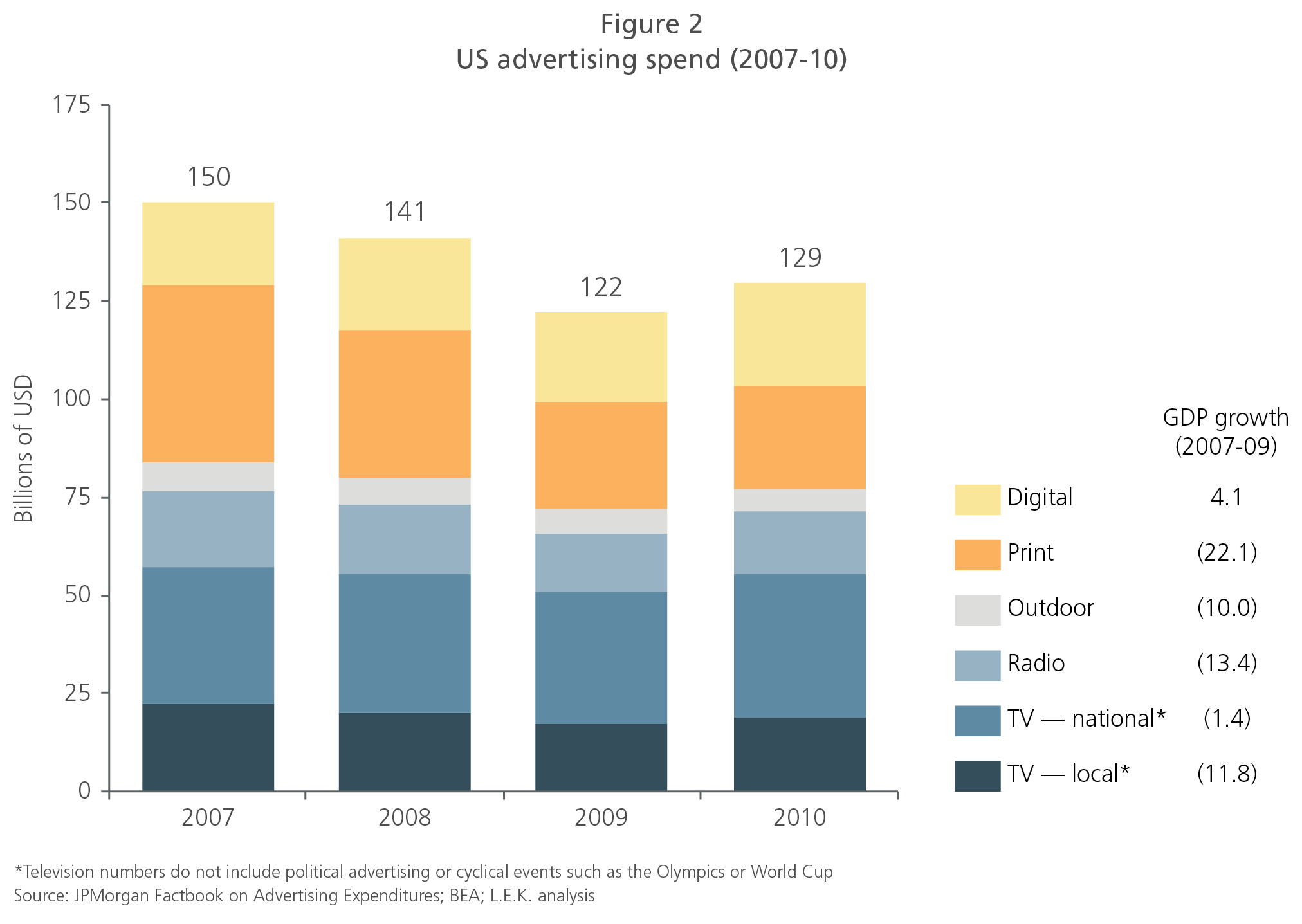

Recessionary periods impact advertising mediums differently

Idiosyncratic factors can have a significant impact on the trajectory of both the decline and recovery of a particular advertising format. For instance, TV’s heavy reliance on upfront purchases protected an immediate pullback but may lengthen the recovery if advertisers are unwilling to make longer-term commitments during the next upfronts.

Additionally, other medium-specific factors, such as local TV’s reliance on smaller local businesses or the lack of car or foot traffic due to lockdowns for the outdoor market, can have a large impact on a format’s overall outlook.

Finally, special attention must also be paid to where each advertising medium sits within its life cycle.

Recessions amplify long‐term trends

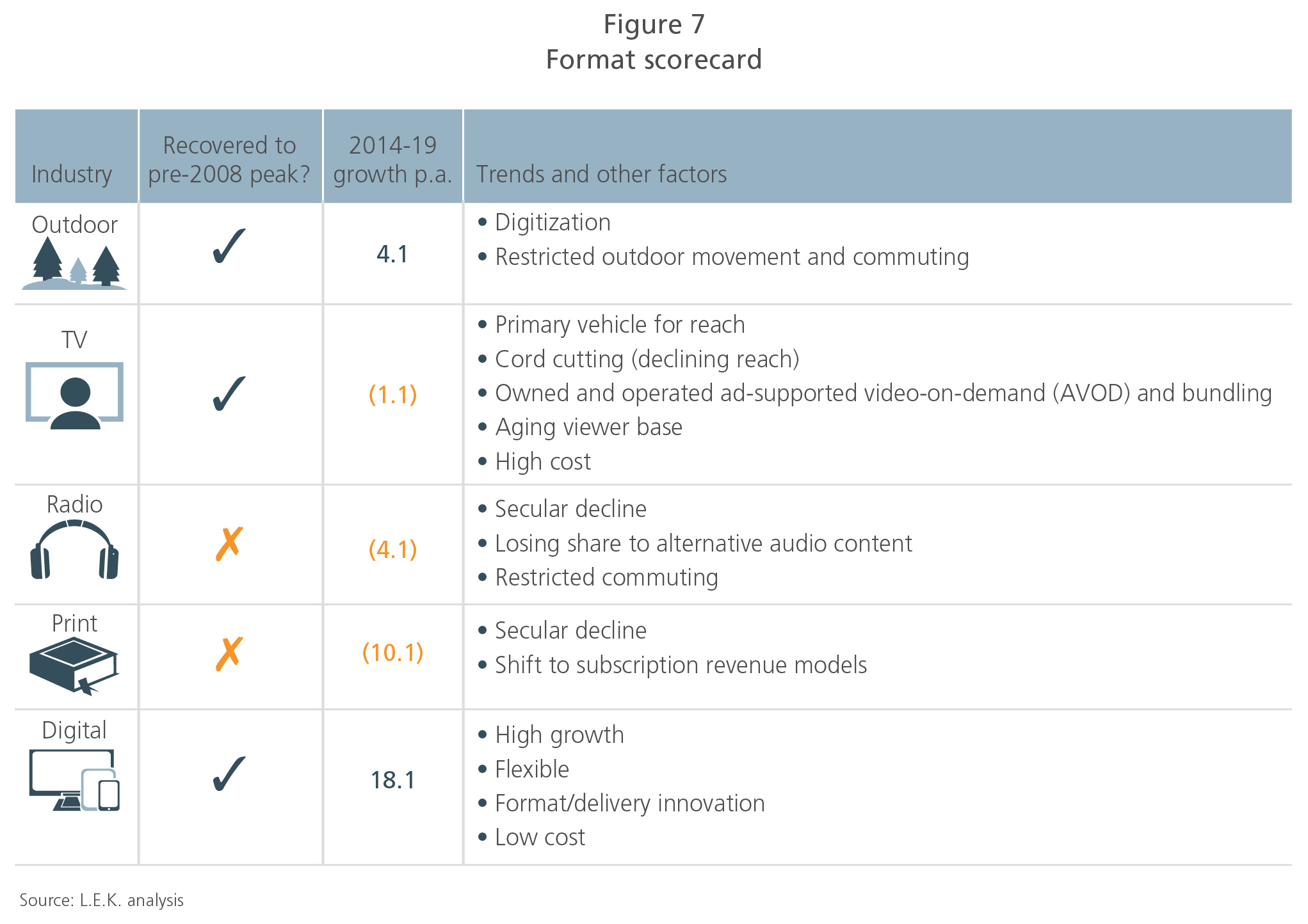

In 2007, digital remained a small piece of overall advertising. However, digital was still in the infancy of its growth cycle, so, despite an overall decline in ad spend of ~19% p.a. 2007‐09, digital saw ~4% p.a. growth over the same period.

Print and radio demonstrate the downside case is also true. Having experienced steady declines since 2000, the Great Recession caused a dramatic pull back, one that these formats have not yet, and likely never will, recover from.

The big question this time is what will happen to TV given that TV largely continued its modest growth trajectory after the Great Recession. Recently, however, despite a strong economy, TV has begun a steady decline. Does this indicate COVID‐19 will result in a permanent reset for TV much in the same way the Great Recession did for print and radio?

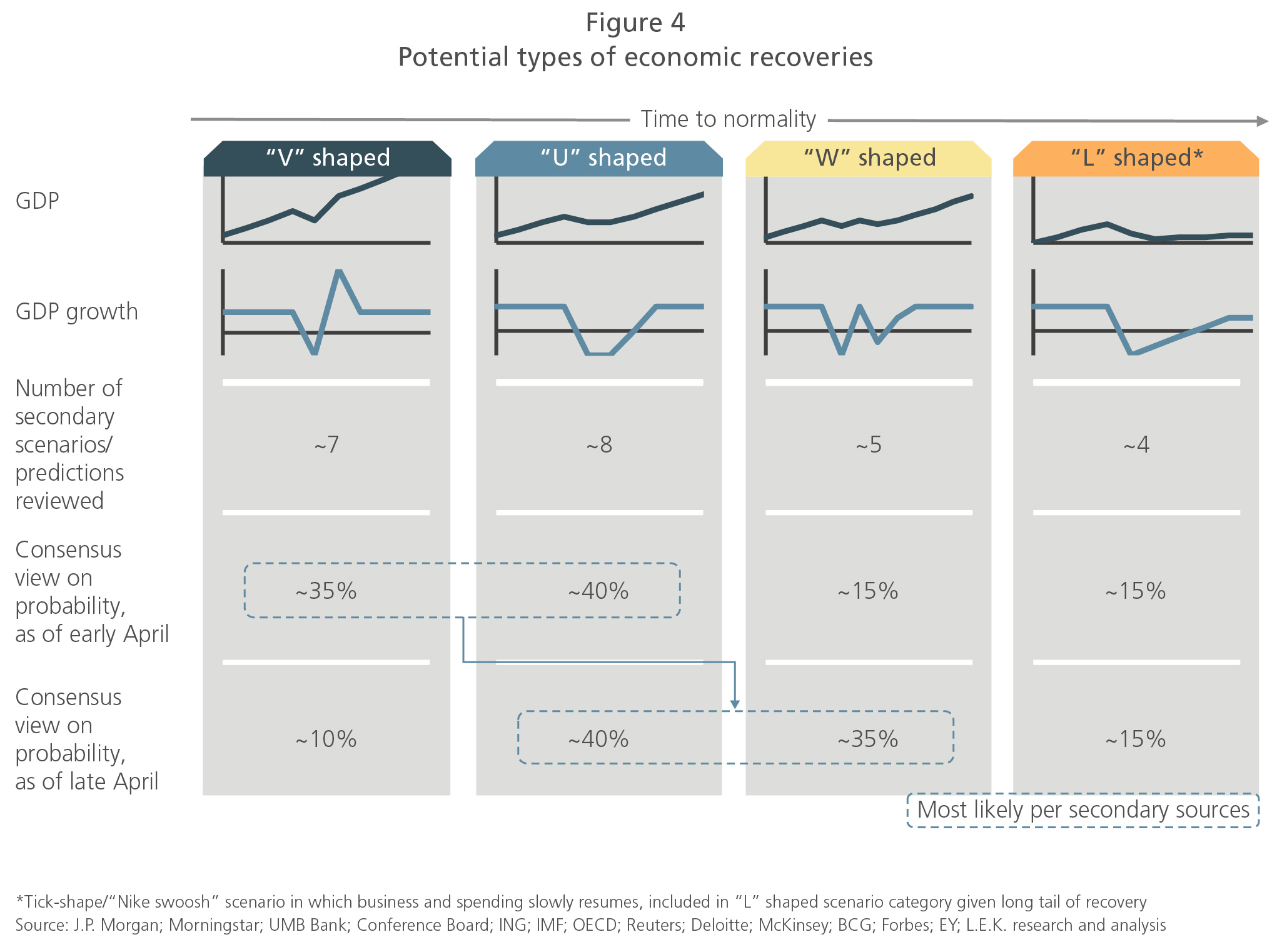

What will the economic recovery look like?

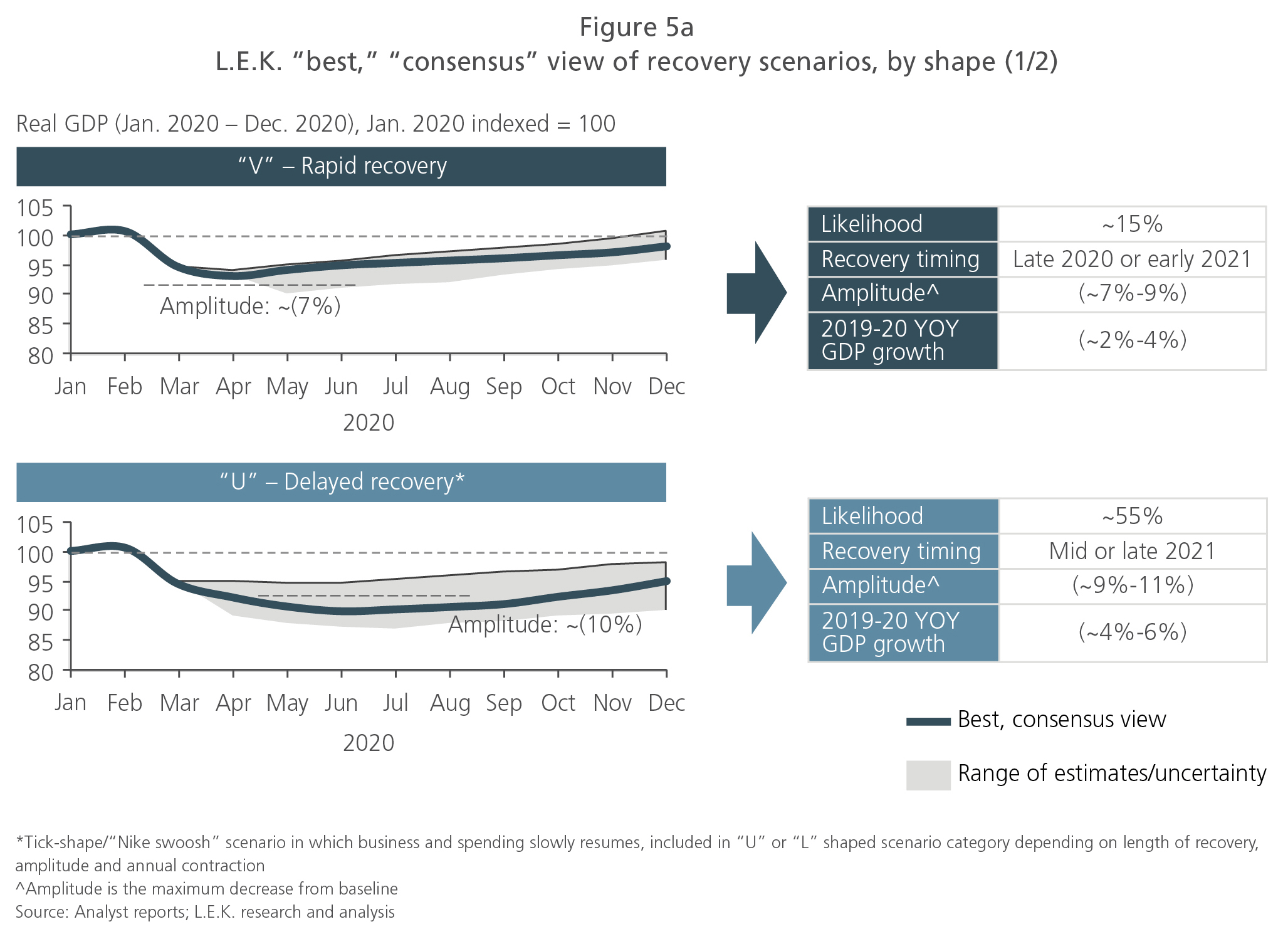

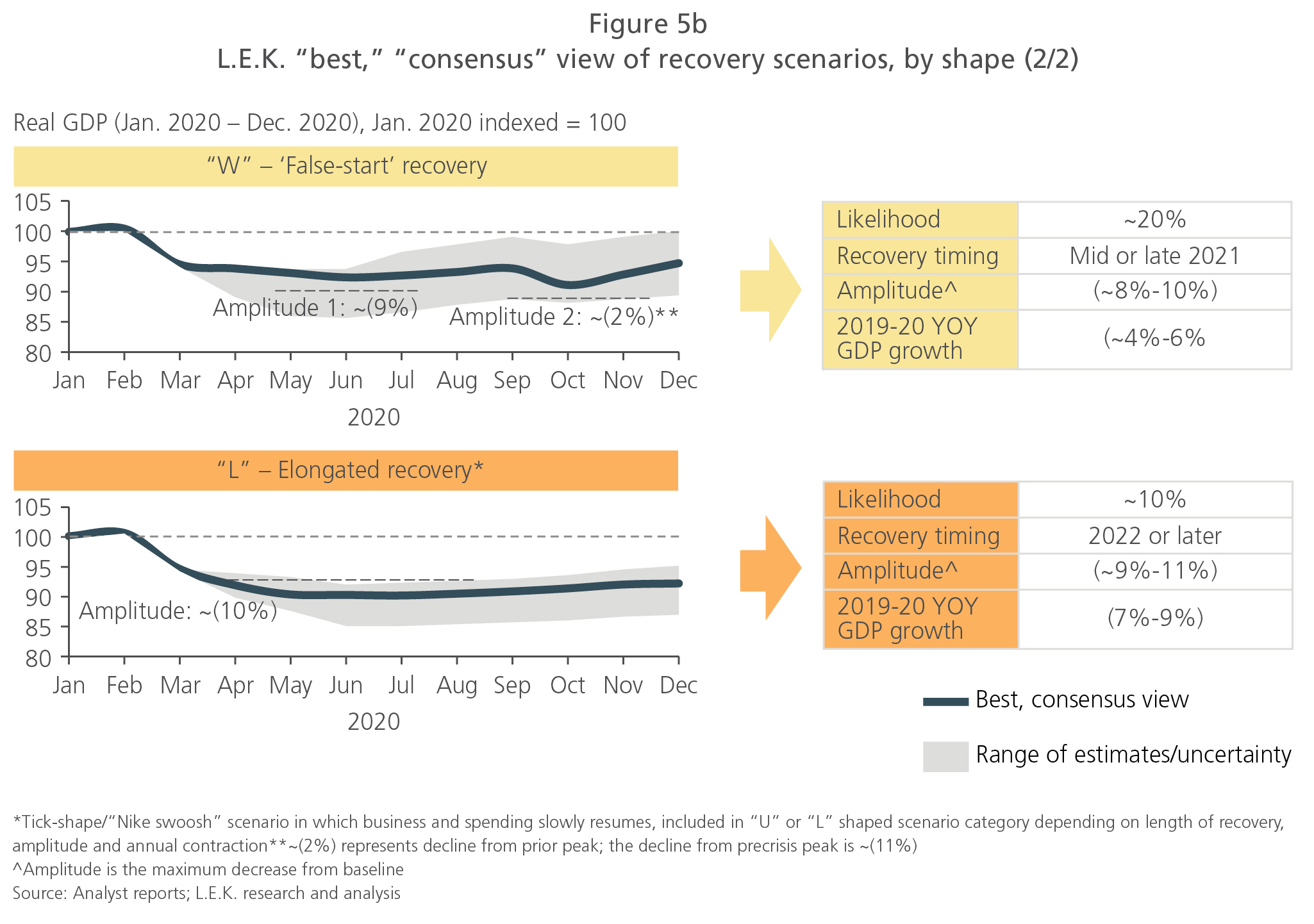

Economics textbooks discuss multiple potential types of recoveries from an economic recession: V-shaped, U-shaped and L‐shaped. We have also included our own W or “false start” recovery scenario.

V‐shaped recoveries exhibit not only a sharp initial decline in GDP, but also a rapid bounce back. U‐shaped recoveries exhibit a more gradual return to full employment and normal economic activity. W‐shaped recoveries are similar to U‐shaped except involve two troughs instead of a single prolonged trough.

Meanwhile, L‐shaped recoveries involve an extended period of depressed consumer spending, economic activity and employment.

The rate at which the economy recovers will have a profound impact on U.S. advertising spend. So what are economists’ projections for the recovery?

Consensus estimates of GDP project 4%‐9% declines in 2020

Economic prognosticators forecast a wide range of future GDP growth. We aggregated a number of different projections to develop a “best consensus” view of V-shaped, U-shaped, W-shaped and L-shaped recoveries.

All three recoveries project a GDP decline in 2020, ranging from a 7.9% drop in the L-shaped recovery to a 3.6% decline in the V-shaped.

In 2021, the V‐shaped economy will be in the midst of a strong recovery with projected growth of 4.6%. The U‐shaped recovery also projects a return to growth of 4.3%. The W‐shaped scenario diverges from the U‐shaped scenario in 2021 with expected GDP growth of 2.3%. We expect GDP to remain largely flat in 2021 under the L‐shaped scenario.

What do each of these GDP growth scenarios mean for advertising spend?

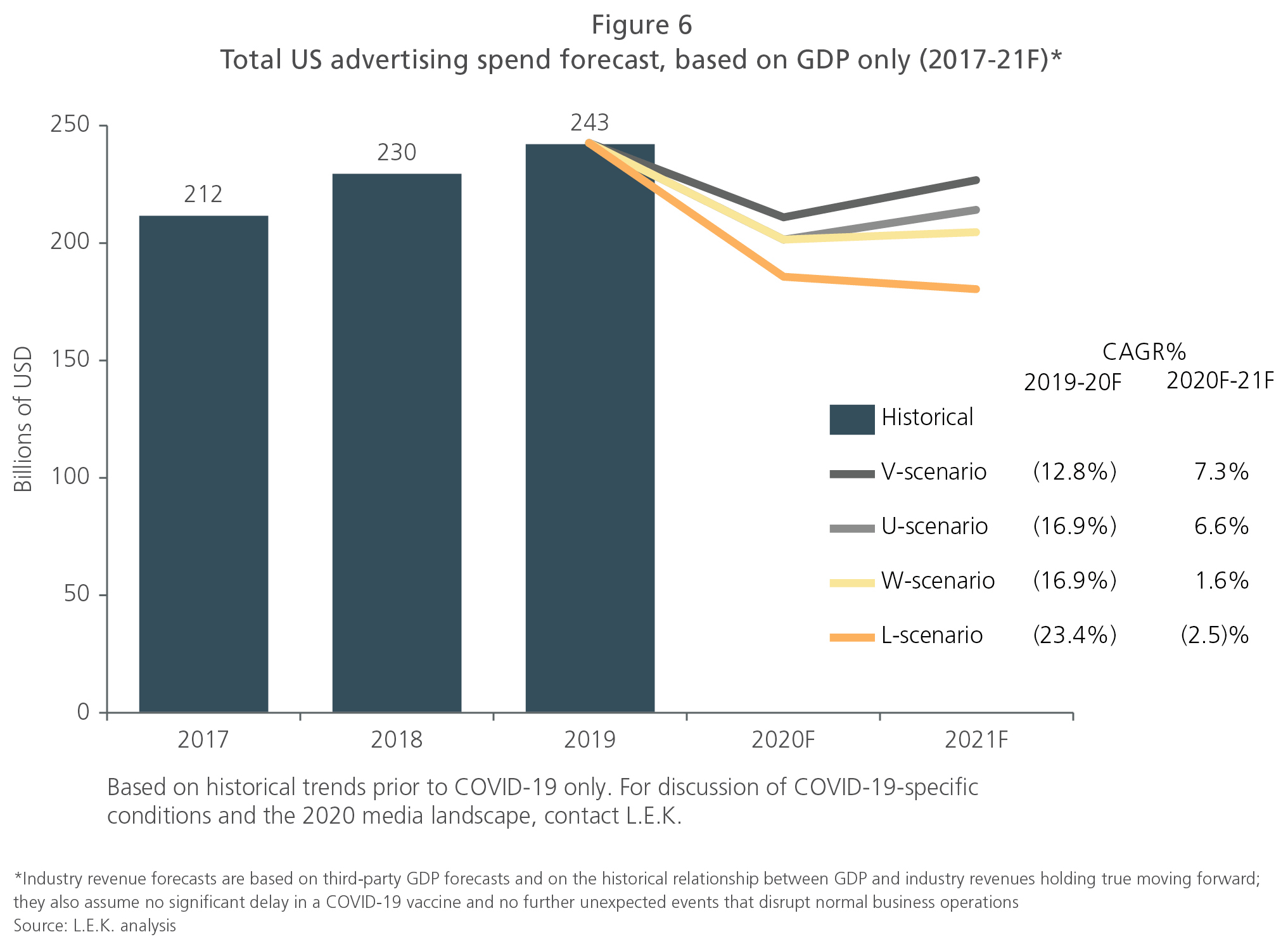

If GDP forecasts and past relationships between GDP/advertising hold, ad spend is unlikely to reach 2019 levels by 2021

The various consensus scenarios for GDP produce highly variable ad spend projections, though all project that spend will not return to 2019 levels by 2021.

In the most optimistic scenario, ad spend is projected to decline 10% in 2020, then recover and grow 3% in 2021 for an overall CAGR of -4.1% from 2019‐21.

Under the U‐shaped recovery, ad spend is projected to decline 6.4% p.a. 2019‐21.

However, things could be much worse: The L‐shaped recovery projects a 22% decline in ad spend in 2020 and an additional 4% drop in 2021, with any recovery occurring further out.

Given the variability of the projections, what can advertisers and publishers do to respond to these unprecedented events?

Format-specific factors

Not all advertising formats are impacted equally in a recession, certainly a recession brought on so quickly and with such drastically different impacts on different forms of media.

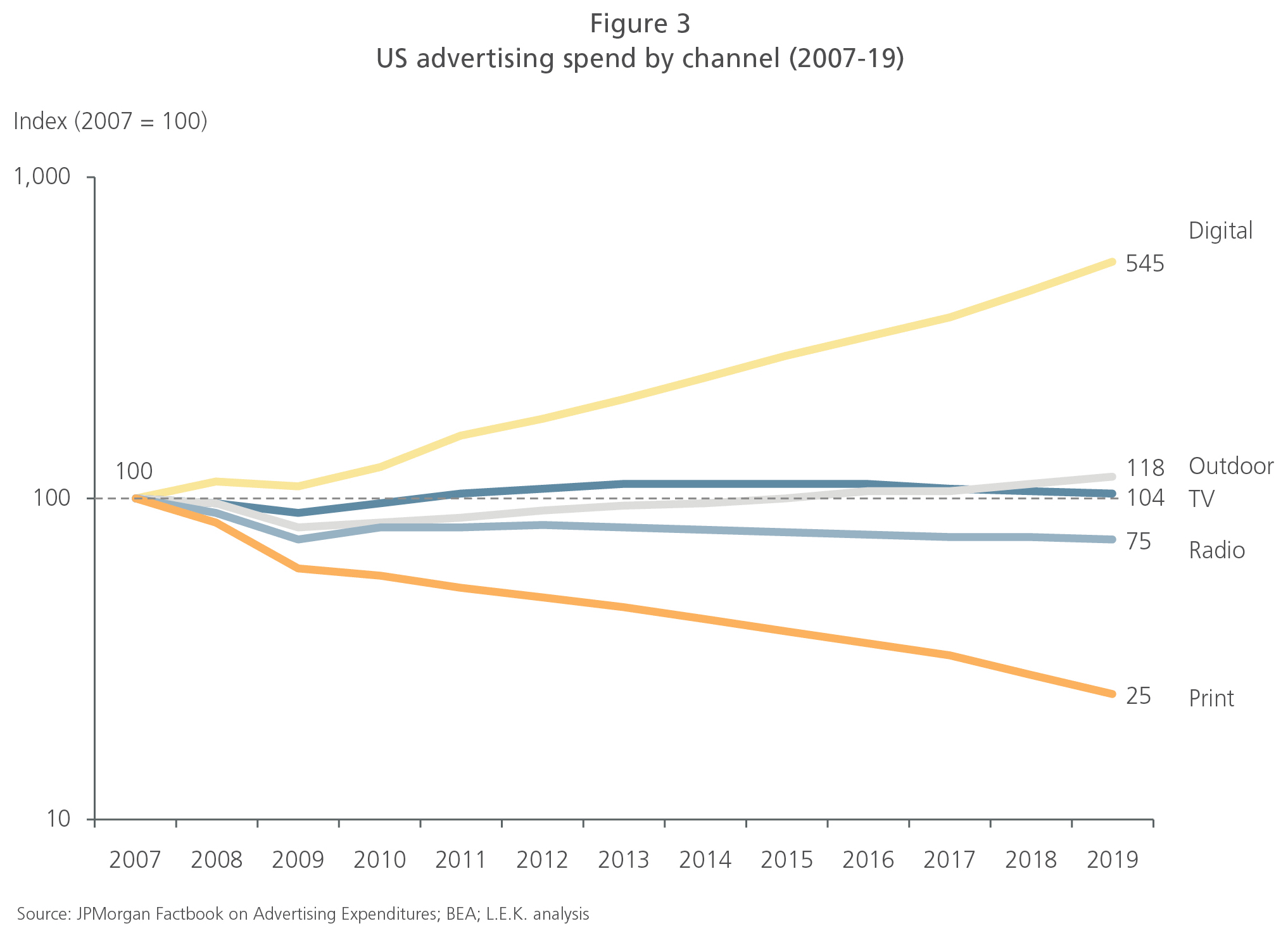

Both digital and outdoor formats have recovered to their pre‐2008 peak and were experiencing growth through 2019. Outdoor advertising is also experiencing a digitization tailwind that should power growth over the medium term.

The outlook for TV is mixed. Entrenched structural factors have long forestalled the widely predicted “death” of television, but as seen earlier, recessions are a catalyst for change. What does that mean for the future of TV and the rest of the advertising landscape?

Key takeaways and strategic considerations

This crisis is different — The rapid nature of unemployment driven by the underlying public health crisis and the accompanying restrictions to movement will cause this recession to differ from those in the past. Job losses have outstripped those of the 2008‐09 recession in a matter of weeks. Additionally, the pandemic source of this crisis and the restricted movement response will impact the recovery in both predictable and unforeseen ways.

The outlook for mediums in secular decline is bleak — The Great Recession accelerated the decline of print and radio that was already in progress. Expect more of the same from today’s laggards.

Look for bright spots, but don’t expect a savior — Certain segments of the economy have benefited from COVID‐19, and publishers should respond accordingly and take advantage of new opportunities. However, don’t expect these industries to wholly make up for losses elsewhere.

Hope for the best and prepare for the worst — While an accelerated or moderate recovery remains possible, the chance for an extended downturn cannot be counted out. Firms must prepare a strategy to handle the potential of a few lean years. These include devising new revenue streams and/or ensuring viability through cost-saving measures.

The new “normal” will be anything but — COVID‐19 may forever change American life, regardless of the pace of recovery. Expect an acceleration of digital trends previously seen in areas such as fitness, the workplace and ecommerce. Additionally, there will likely be broad adoption of virtual platforms for the personal and social life. Finally, health and hygiene will forever be revolutionized. Each of these changes could have a profound effect on the advertising industry.

01272022090129