Key takeaways

-

The $44 billion U.S. spirits market is expected to grow 6% per year through 2022, promising ample opportunities for a broad range of industry players.

-

Millennials play a starring role in industry growth, comprising 32% of U.S. spirits consumption by value.

-

New categories of spirits are gaining popularity, such as tequila, brandy and whiskey.

-

Craft spirits are the next big thing, and larger brands are starting to hop on the craft bandwagon as well.

-

A robust consolidation environment is expected to continue at a healthy clip.

The $44 billion U.S. spirits market is expected to grow 6% per year through 2022, promising ample opportunities for a broad range of industry players. From millennials’ drinking habits to the growing popularity of craft spirits to a robust consolidation environment, we break down 10 trends that will affect the industry going forward.

1. It’s a huge market that is continuing to grow

Based on wholesale prices (WSP), U.S. consumers imbibed nearly $44 billion worth of margaritas, martinis, manhattans and more in 2017 — with no signs of slowing down. That figure is forecast to reach $58 billion by 2022, an annual growth rate of 6%. This optimistic forecast for robust price growth is further buoyed by liquor sales’ relative immunity to economic downturns, as supported by the small but steady growth trajectory in spirits during the 2007-08 recession.

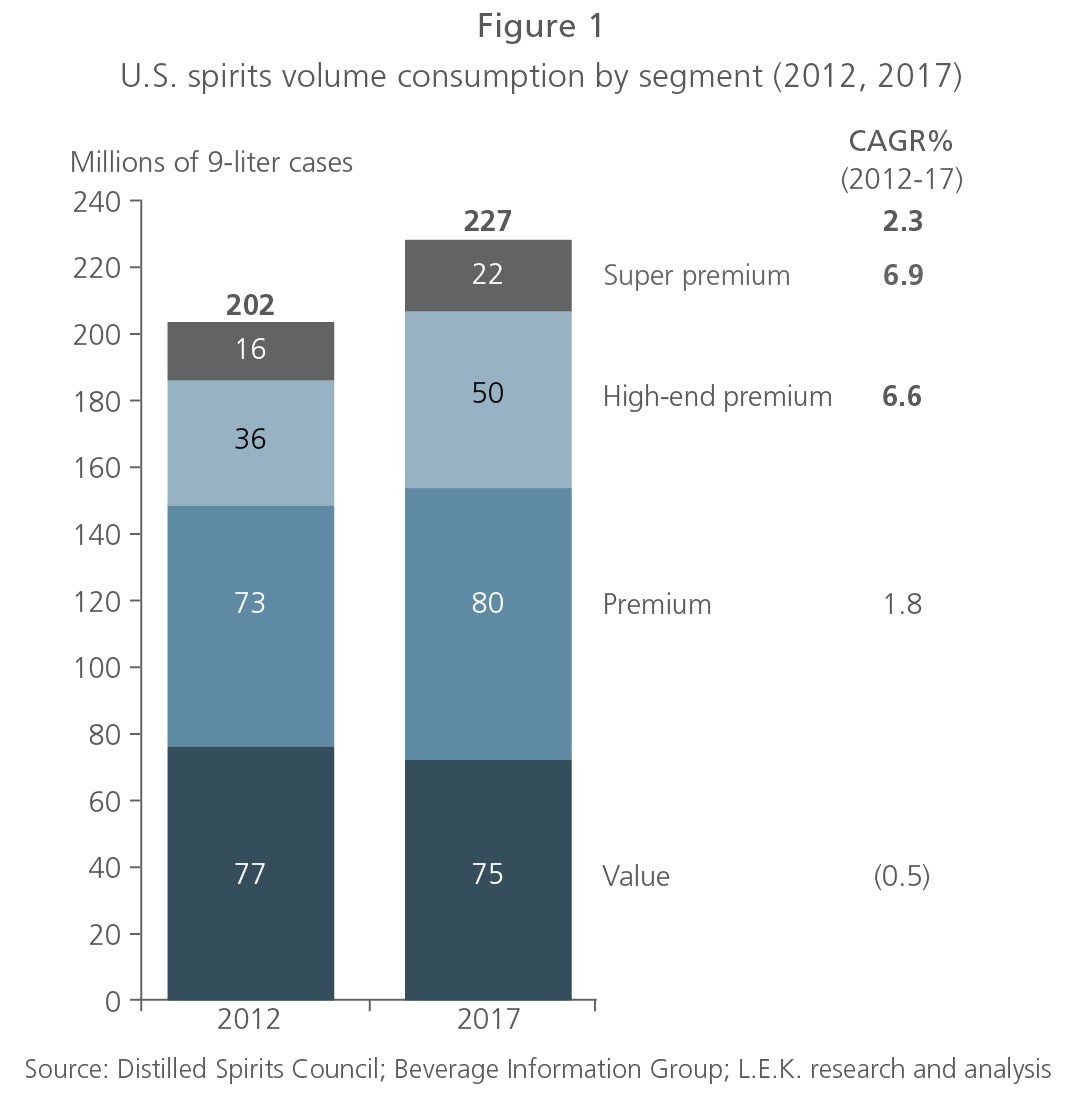

2. Premiumization is propelling overall growth

Consumers, particularly millennials, are bypassing the value and premium liquor store shelves in search of high-end, super-premium products. From 2012 to 2017, the super-premium spirits and high-end premium spirits segments grew 6%-7% per year by volume, significantly outpacing the premium and value segments’ growth and driving the overall increase in spirits consumption (see Figure 1).

What’s causing consumers’ gravitation toward high-end spirits? While continued confidence in the economy and product innovations have drawn consumers to more expensive liquors, millennials, unsurprisingly, are the main story behind this trend. Seeking out a path to tipsiness paved with fewer calories and superior ingredients, millennials are increasingly substituting super-premium spirits at the expense of higher-calorie, low-alcohol-content beer.

3. Millennials are sipping their fair share

While just 29% of the drinking-age population are millennials, they over-index on consumption across all major types of alcohol. In spirits alone, they comprise 32% of consumption by value. And this is expected to continue as millennials mature and their buying power increases. Millennials likely have influenced market growth in one alcohol type over another as well. Spirits’ market share increased to 36% in 2016, up from just 29% of the total market across beer, spirits and wine in 2000, primarily at the expense of beer. Evidence suggests that millennial consumption patterns have played a huge role in this marked shift from beer to liquor.

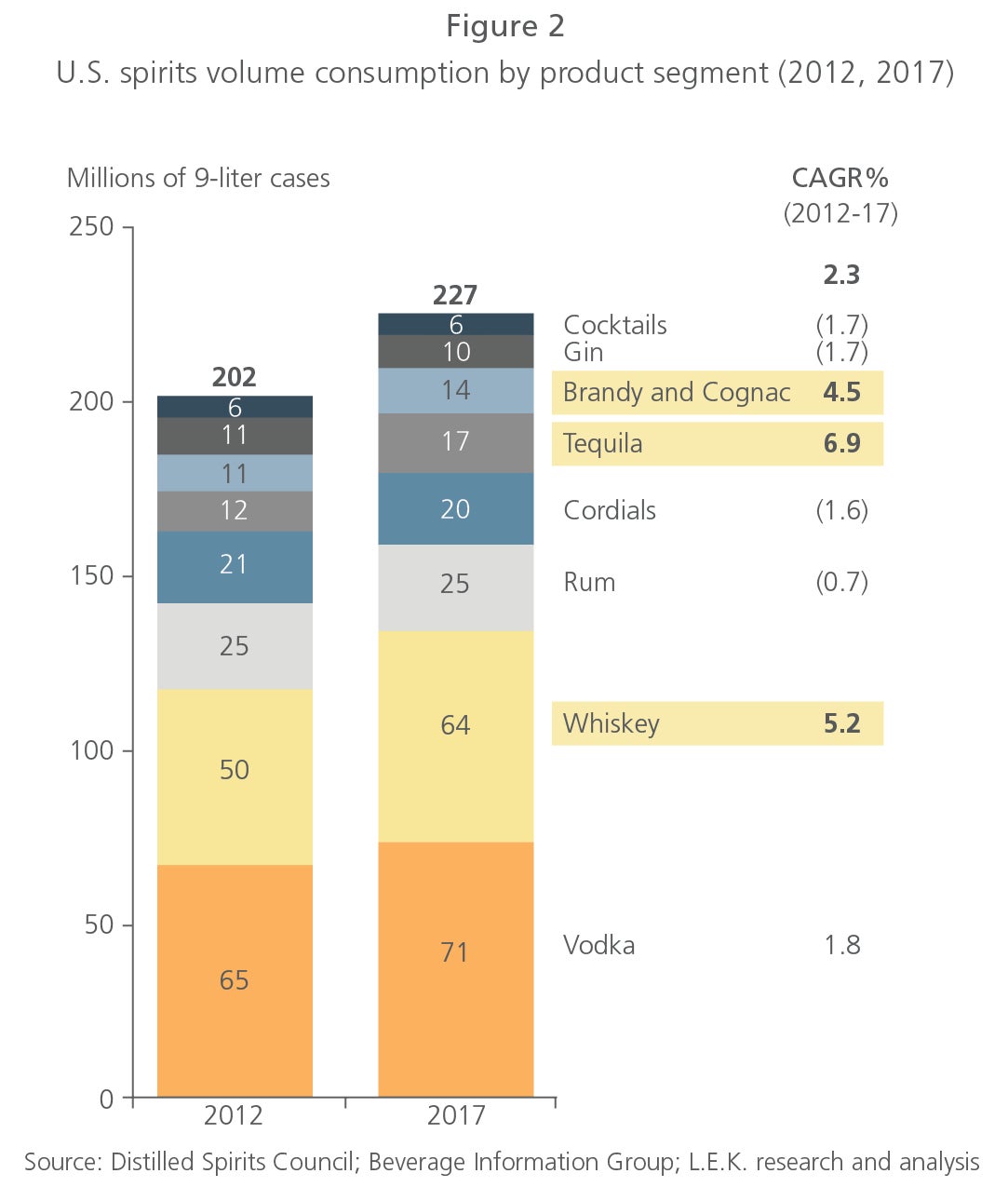

4. Whiskey, tequila, brandy and cognac are winning out

Move over gin, cordials and rum: Whiskey, tequila, brandy and cognac are gaining in popularity, driving the bulk of volume consumption growth from 2012 to 2017 (see Figure 2). And blended malt Scotch whisky is leading the pack as the fastest-growing category, with consumption increasing a whopping 25% in 2015-16.

Why are these categories growing at such an explosive rate? The rise in creative, innovative cocktails and the growing “cocktail culture” in the U.S. have helped make liquors such as super-premium tequila trendy. Product innovations such as flavored liquors and nonconventional and/or experimental aging processes are also a factor. For instance, the flavored whiskey category, with offerings ranging from vanilla to salted caramel, grew by 8.5% in 2017.1 Another example: Iconic Irish whiskey brand Jameson is shaking things up with its Caskmates series, swapping out traditional casks for stout beer barrels.

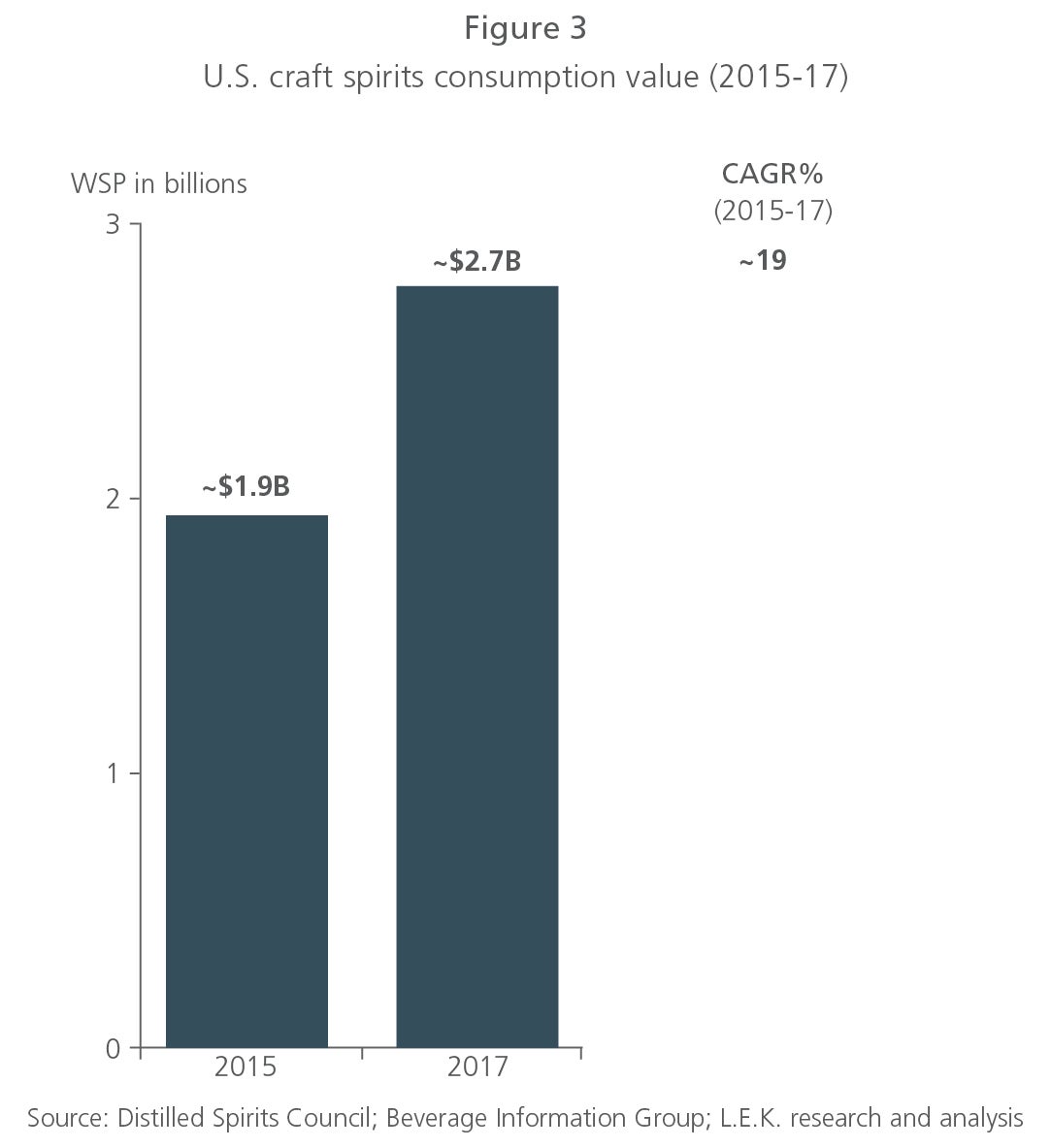

5. Craft spirits are the next big thing

Craft spirits are taking off: The number of distilleries has increased approximately 35% per year since 2011, while the craft spirits market has grown 19% per year since 2015 (see Figure 3). And while lagging the overall category penetration of craft beer producers, the U.S. craft spirits market has grown by approximately 20% per year by value since 2012 and is forecast to grow by approximately 15%-20% per year through 2022.

What defines craft spirits products? While the definition varies slightly, generally craft spirits are produced by a licensed distillery, which must distill and bottle the products on-site. Furthermore, these distilleries are subject to a maximum volume of 750,000 gallons of spirits per year.

Retailers and wholesalers are optimistic about the future growth of craft spirits, believing the market can perform as well or better than craft beer. In fact, 60% of wholesalers think that craft spirits will become more relevant to the liquor industry than craft beer is to the beer industry. Craft beer currently comprises less than 12% of U.S. market share, leaving significant room for craft spirits growth.

6. Large brands are hopping on the craft bandwagon

Major brands see the big opportunities yet to come in the craft spirits category and are developing products to capitalize on this growing trend. And fortunately for them, relatively large distilleries can qualify as craft producers, provided they meet volume limits and aren’t operated by a global spirits producer.

For instance, Maker’s Mark’s Private Select program brings retail customers to its Kentucky distillery to custom finish cask-strength bourbon. Visitors select the barrel where the bourbon will “finish,” ultimately yielding 240 unique bottles. Another example: Our/Vodka, a unit of Pernod Ricard, is distilled in local microdistilleries worldwide and then sold under the local distillery’s brand (e.g., Our/London, Our/Los Angeles). Our/Vodka currently has distilleries in Amsterdam, Berlin, Detroit, London and Los Angeles, and additional distilleries in Houston, Miami and New York are scheduled to open in 2018.

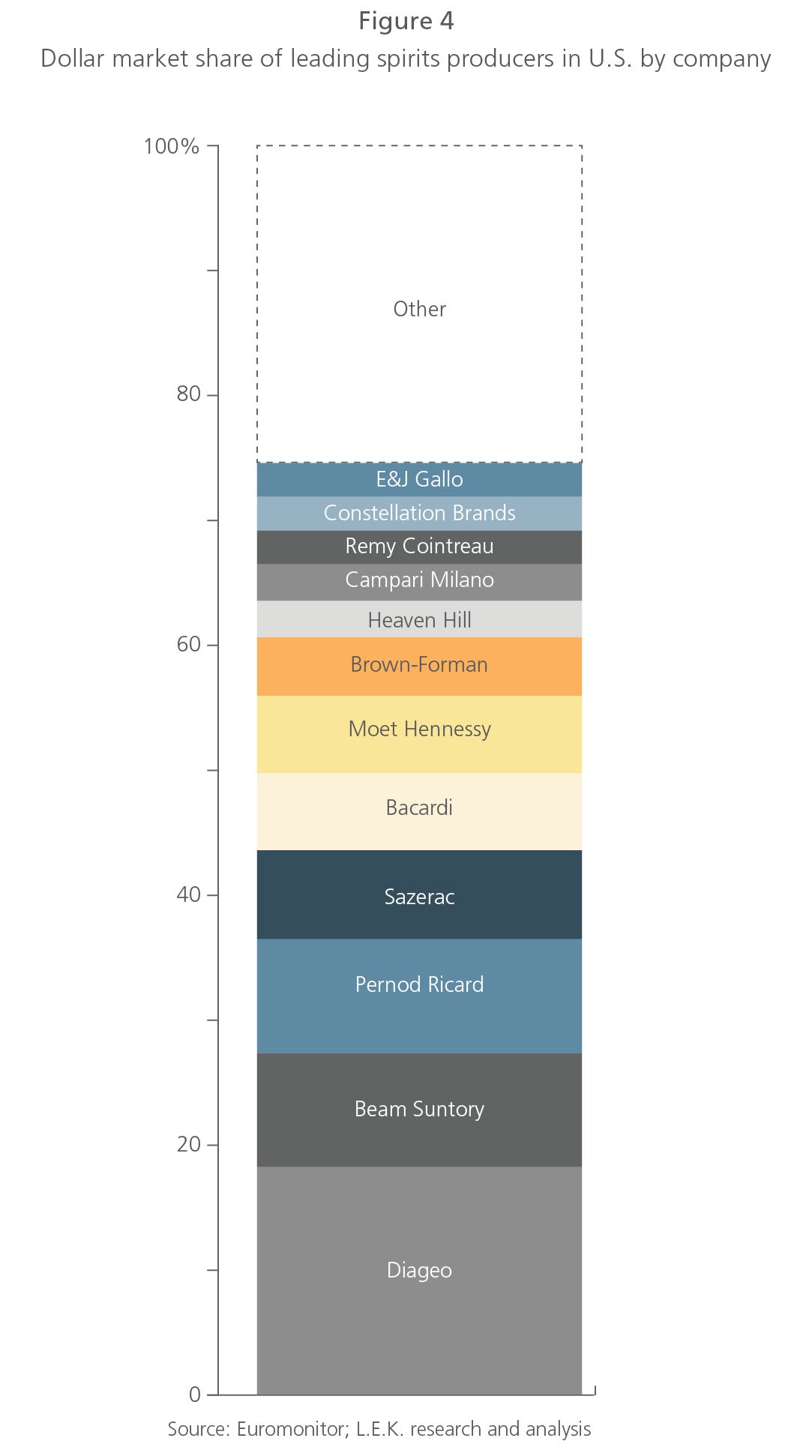

7. A robust consolidation environment is expected to continue

Industry M&A and consolidation activity has been high, with 25+ known deals since 2014. It’s no surprise, then, that the top seven spirits producers account for approximately 60% of the U.S. spirits market, with Diageo as the clear market leader (see Figure 4).

Despite this high concentration of spirits producers, however, consolidation is expected to continue at a healthy clip through 2018. In particular, diversified independent distilleries and focused independent distilleries are attractive candidates for acquisition in this buyer’s market.

8. Drinking at home beats going out

Unlike for beer and wine, spirits consumption by venue has been growing across both on- and off-premises channels. However, “drinking in” has driven much of the growth due to myriad factors including the competitive retail landscape where there are deals to be had. And this growth is expected to continue outpacing on-premises consumption, as the environment offers huge growth opportunities that “drinking out” currently does not.

9. Good things come in small packaging

With demand for greater variety and portability in many consumer goods categories, the spirits market is following suit — and with good results. Smaller packaging sizes (ranging from 50mL to 100mL) are seeing above-average growth. For instance, consumption of 50mL bottles increased 18% by volume from 2016 to 2017, while consumption of 100mL bottles increased 11% over the same period.

Despite success in beer and wine, canning and “bag in box” spirits packaging isn’t quite there yet. Still in nascent stages, new formats for spirits are expected to face adoption hurdles due to consumer perceptions, shelf-life limitations and lack of canning partners. There are exceptions, though, such as Fireball whiskey and canned, premixed cocktails.

10. Ecommerce channels are expected to grow

These days, consumers can buy just about anything from the comfort of their home, and spirits are no exception. Direct-to-consumer (DTC) and other ecommerce channels that sell spirits have the potential for strong growth from a small base.

DTC players have employed different business models to legally sell to consumers directly. For one, distilleries are selling direct to consumer at a physical location or online. Third-party cocktail clubs (e.g., SaloonBox) are gaining popularity in the “cocktail culture,” where clubs deliver expert-curated cases of spirits and cocktail ingredients; retail partners deliver the liquor, while the cocktail ingredients are shipped directly. A third business model, employed by the likes of startups such as Drizzly, is ecommerce delivery platforms that deliver liquor purchased from local retailers directly to consumers.

1 “Major Spirits Players Innovate to Keep Pace with Consumers’ Changing Tastes,” Shanken News Daily, August 9, 2018.

09272019110952