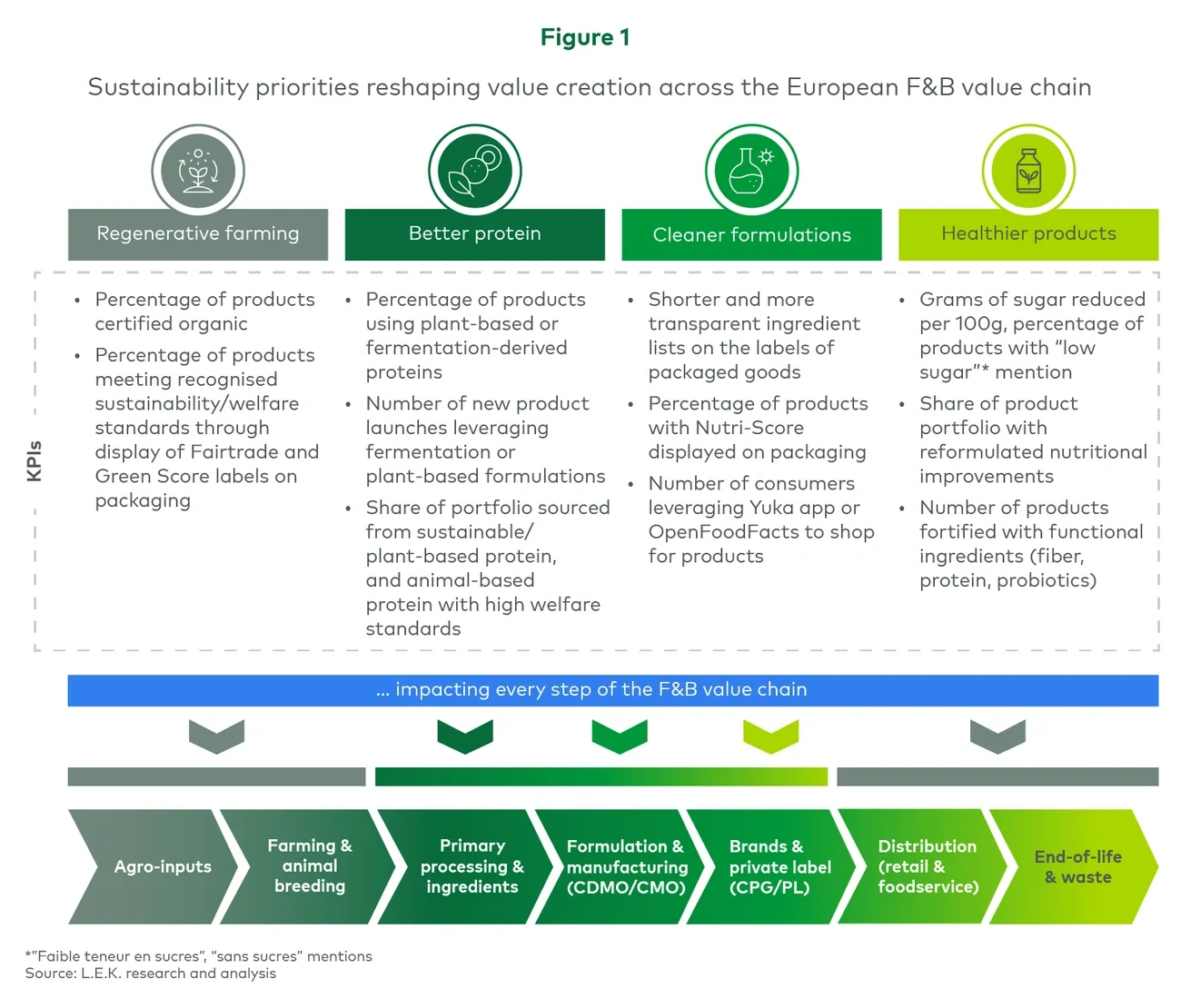

Across Europe, the pursuit of healthier and more sustainable diets is reshaping supply chains and product portfolios. What began as a movement among conscious consumers now influences how value is created and captured across the food and beverage sector (see Figure 1).

Europe’s Sustainable Food Shift: Where the Next Wave of Value Creation Lies

Europe’s Sustainable Food Shift: Where the Next Wave of Value Creation Lies

February 18, 2026

Image

At a recent lunch on the topic, hosted in partnership with Lincoln International, we illustrated how this shift has gathered pace.

A shift in consumer behaviour

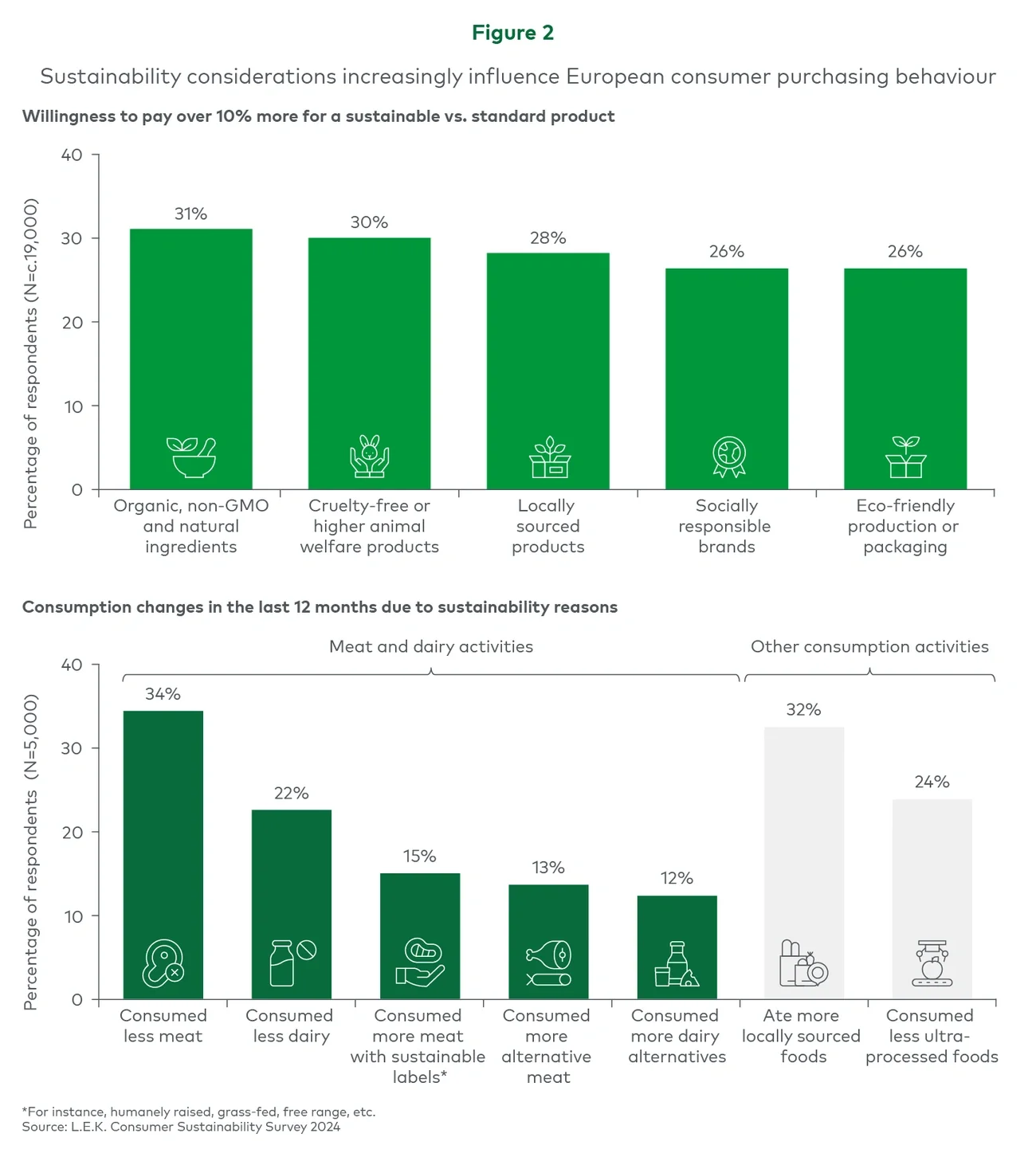

European consumers have moved beyond signaling good intentions. They are changing what they buy and how they assess quality, even in the face of squeezed disposable incomes (see Figure 2).

Image

L.E.K.’s 2024 Sustainability Survey found that almost 60% are willing to pay more for products with proven nutritional benefits, and nearly half now seek sustainable alternatives even in tighter economic conditions.

Digital transparency tools such as Yuka have also made product data an everyday reference point, reinforcing accountability across brands.

Policy pressure with commercial consequences

Europe’s regulatory framework is no longer an abstract goal-setting exercise. The Farm to Fork Strategy and Common Agricultural Policy are directing substantial funding toward organic and regenerative production. Updated labelling and information standards are tightening definitions and rewarding verifiable sustainability claims.

Increasing consumer demand and regulatory measures have created clear incentives for manufacturers to reformulate, although progress varies by category and price tier. Major food companies have reduced additives, cut sugar and salt, and introduced nitrite-free product lines in response to Nutri-Score and consumer scrutiny.

The result is a more transparent and disciplined market in which compliance and competitiveness increasingly align.

Innovation and capital flow through the value chain

The transition is generating distinct areas of opportunity across the value chain. Below, we identify four in particular:

- Biostimulants and regenerative inputs: Biological solutions are improving yields and soil resilience while reducing fertiliser use. The European biostimulants market, now around $1.4 billion, is expanding at roughly 10% a year, driven by better product performance and strong policy support.

- Clean-label functionality: Ingredient innovation continues to be driven by the naturalisation of formulations (replacement of synthetics, shorter and more recognisable ingredient lists), while increasingly focusing on delivering taste and texture parity with conventional products to secure repeat purchase.

- Traceability and sourcing systems: Digital platforms and certification networks are turning supply-chain transparency into measurable equity.

- Waste reduction and upcycling: Waste management is shifting from compliance to efficiency, capturing new value in energy, ingredients and logistics.

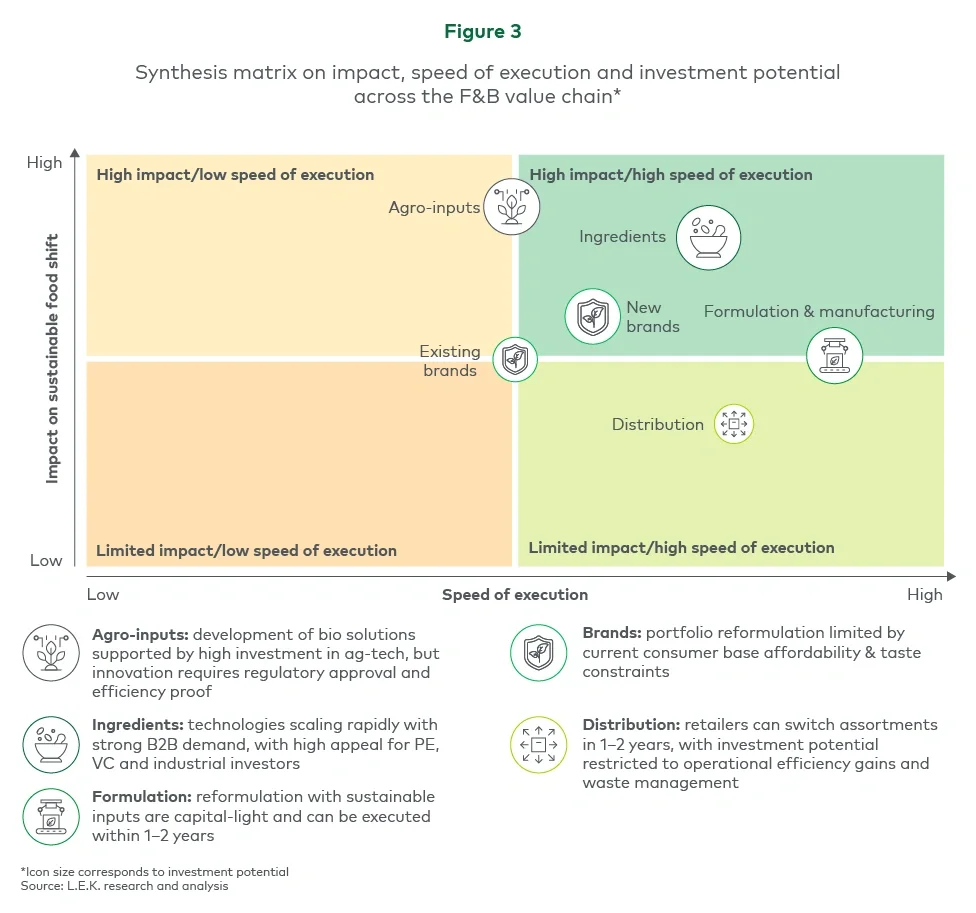

Each area is underpinned by investable science, repeatable business models and visible environmental impact (see Figure 3).

Image

Investment momentum and consolidation

Recent M&A activity across Europe shows where strategic investors are placing their bets. Ingredient and formulation specialists have attracted sustained attention, offering scalability and steady B2B demand. Regenerative farming platforms and biocontrol companies appeal to investors seeking IP-based defensibility and predictable returns. Emerging brands, meanwhile, are focusing on verified sourcing and functional nutrition as differentiators.

Sustainability is proving to be an engine of pricing power and brand preference. Capital is following the operators that can demonstrate both environmental and financial performance.

However, critical challenges remain. Price-sensitive consumers still limit the reach of organic products; flavour and texture continue to constrain plant-based adoption; and inconsistent labelling erodes trust. Each issue has a technical solution: cost reduction through regenerative sourcing and scale efficiencies, sensory improvement through R&D partnerships, and transparent certification backed by evidence rather than claims.

The strategic horizon

Our analysis points to a set of clear priorities for executives hoping to shape the pace of progress:

- Strengthen supply-chain resilience and cost competitiveness through regenerative, diversified and more efficient sourcing models.

- Accelerate ingredient naturalisation at scale, while ensuring sensory and functional parity with conventional formulations.

- Embed verified data and certification to build trust, ensure compliance and support credible sustainability claims across the product lifecycle.

The sustainable food shift is well underway, but unlocking its full potential depends on converting it into disciplined strategy and measurable results — while addressing the constraints that could otherwise slow mainstream adoption.

Contact us to find out more.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC

Related insights

You might also be interested in these insights.

English