The expanding market for over-the-top (OTT) services continues to reshape the consumer-video landscape, putting increasing pressure on traditional pay TV providers while creating an ever more crowded and competitive field of newer players. In the following Executive Insights, L.E.K. Consulting sizes up some of the top platforms vying for online video supremacy, including perspectives on how the current pandemic will impact key players, as well as strategies for entrants seeking streaming success in the years ahead.

The past decade brought a seismic shift in the world of video as consumers increasingly opted out of pricier pay television packages in favor of lower-cost (and in some cases, free) OTT services. At last count, top providers Netflix, Hulu and Amazon Prime Video had a combined U.S. subscriber base of around 130 million and counting. But the “Big 3” of OTT have plenty of company — today, there are well over 100 different streaming services, covering niche topics like indie films and auto racing as well as vintage TV programming and more.

Some big names are set to launch imminently, including NBCUniversal’s Peacock and HBO Max. They join recent entrants such as short-form specialist Quibi, Apple TV+ and Disney+, the latter of which is already making a major splash with its well-stocked library of back-catalogue feature films and TV shows (including Disney classics) and original titles such as “The Mandalorian.”

Though the market may appear overextended, such services are in fact more popular than ever: According to Leichtman Research Group, roughly three-quarters of all domestic households currently maintain at least one OTT service, a nearly 45% increase in the past five years. L.E.K.’s own research found the average U.S. household now subscribes to approximately 2.8 subscription video on demand (SVOD) services, up 9% from a year prior. The COVID-19 crisis and associated lockdowns are further fueling demand — in a recent analysis by Morning Consult, 19% of respondents stated they would spend more on movie and TV streaming due to the pandemic.

OTT gains continue to come at the expense of traditional multichannel video programming distributor (MVPD) services: Recent data from MoffettNathanson shows approximately 81 million MVPD households in 2019, down roughly 17% from more than 98 million just five years ago, and many analysts, as well as L.E.K.'s proprietary consumer research, suggest there are more declines to come. Convenience, breadth of content and compelling value continue to drive OTT consumption, with demand stemming in large part from younger viewers, who continue to tune out pay TV in favor of OTT — according to our estimates, millennials currently subscribe to 4.6 different SVOD services, not counting the various free ad-based video on demand (AVOD) services they use.

Netflix still reigns supreme

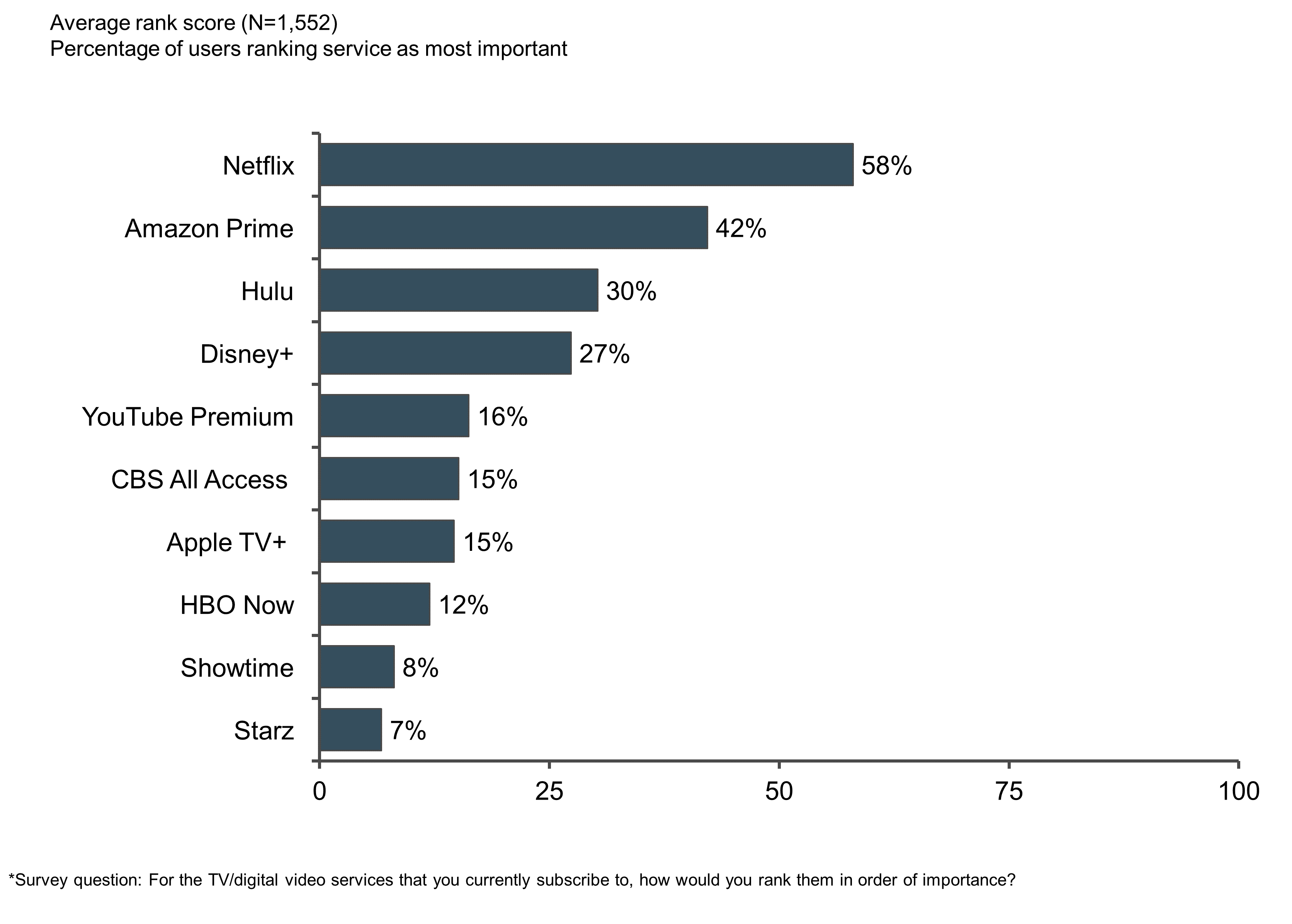

With over twice as many subscribers as Hulu or Disney+ and at least 20% more than Amazon Prime Video, Netflix remains the streaming king, serving approximately 61 million U.S. viewers as of year-end 2019. How has the company managed to maintain its edge? By keeping consumers satisfied with both high-quality content and a large selection of options. Our recent TV/OTT Consumer Study found that 58% of subscribers with multiple SVOD services considered Netflix the least expendable (see Figure 1).

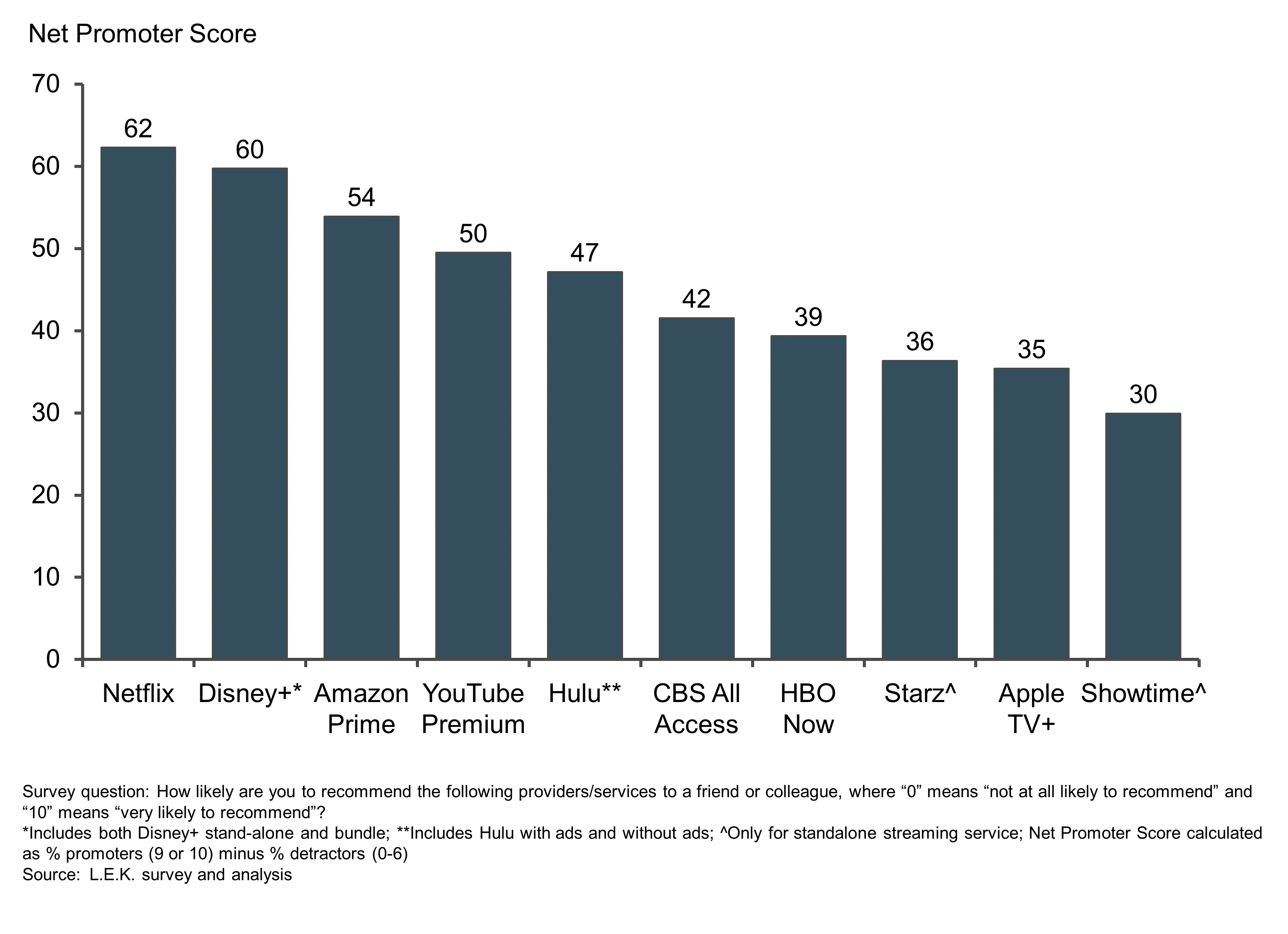

The service also garners an industry-leading Net Promoter Score of 62 ― compared with 54 for Amazon Prime Video and 47 for Hulu (see Figure 2).

Though Netflix pushed through a rate increase just last year (boosting its Premium tier from $14 to $16 monthly), subscribers still consider the service the best bang for the buck, according to our study, and therefore could be amenable to future price hikes so long as content remains up to par. So strong is the company’s hold on its OTT subscriber base that it has been able to withstand the loss of popular TV shows such as “The Office” and “Friends” to competing services (according to our study, fewer than 1 in 5 subscribers would drop Netflix if their favorite show was dropped). This is due in large part to the overwhelming appeal of Netflix’s original content — series like “Stranger Things” and “Mindhunter” remain tremendously popular, and some 8 in 10 viewers said they viewed Netflix originals as high quality and were excited for new releases. Given all of this, Netflix seems capable of fending off all comers and maintaining its seat at the head of the table for the foreseeable future — in fact, its lead may be extending.

Disney+ making a big splash, but production delays are looming

Disney+, the OTT platform launched by The Walt Disney Co. late last year attracted some 29 million subscribers in its first three months, vaulting into third place behind Netflix and Amazon Prime Video, and notably ahead of Disney’s own Hulu (counting SVOD-only service and excluding live TV subscriptions). This growth rate only increased with the onset of COVID-19, with sign-ups allegedly tripling in March 14-16 vs. the prior week.

What accounts for the Disney platform’s astounding success rate to date? For one, Disney+ appears to have found a niche in the market by appealing in large part to families with younger viewers — compared with Netflix, Disney+ users are significantly more likely to have children under 18 in their households.

While Netflix and Amazon Prime increasingly lean on original programming as content owners claw back content from the streamers, library content has been the key driver of Disney+ adoption, with users gaining access to titles like “Star Wars” as well as a vast treasure trove of Disney and Pixar films, TV shows, and shorts, some available in streaming form for the first time ever.

Despite its overwhelming success out of the gate, several factors could dampen Disney+’s future domestic growth. Some 37% of households in the U.S. with kids under 18 (a core demographic) are already subscribed, according to our survey findings (a slightly more recent survey by Ampere Analysis puts this figure at 42%). Indeed, enthusiasm appears to have already leveled off — we found that only around 10% of nonsubscribers were likely to sign up over the near term. It also remains to be seen whether the Disney catalog can keep viewers engaged long term. It is likely that Disney will need to continue to invest in compelling original content like “The Mandalorian” to stay in the hunt as the OTT leader.

However, this could be a problem in the near term. According to an analysis by NScreenMedia, the shutdown of production around the globe driven by COVID-19 leaves Disney+ with an estimated 100 shows in development, stemming the flow of the new content so critical for customer retention (especially when consumers are watching more hours than ever before). Conversely, Netflix’s strategy of dropping all episodes at the same time means that production of an entire series must be completed well ahead of launch. The result? Netflix can continue to release new content at current rates for several months without disruption according to public comments from Ted Sarandos, Netflix’s head of content. Once consumers have exhausted Disney+’s current library, will they turn back to Netflix for something fresh?

Other OTT contenders: Already fighting an uphill battle, made all the more difficult by the pandemic

While some argue that the COVID-19 pandemic and associated self-isolation regime will benefit new launches through consumers’ increased time spent consuming content and propensity to trial new services, we believe that the secondary impacts, including key content gaps due to halted production, depressed advertising spend due to the closure of many advertisers’ businesses and the significant economic uncertainty facing consumers, will result in a more hostile environment for new and nascent services.

![]()

AppleTV+ launched within weeks of Disney+ last November. To date, brand recognition, coupled with a generous year of free service with purchase of an Apple device, has enabled AppleTV+ to amass a significant following (some estimates put the subscriber number higher than that of Disney+, though it’s unclear how many are highly engaged with the service). Unlike leading competitors, the service offers a relatively limited library with few marquee titles, which doesn’t bode well for expected churn once free trials end.

![]()

WarnerMedia is banking on the decadeslong reputation of HBO as THE home of premium quality TV content with the rollout of its forthcoming HBO Max, the SVOD service that will offer both premium-tier HBO programming and new original and library titles. Though HBO brings to bear a hefty subscriber base (estimated at around 25 million linear and 10 million OTT subscribers, respectively, according to research group MoffettNathanson), the $15 monthly price tag for HBO Max could prove challenging for those already carrying multiple OTT services. While it’s still too early to know for sure, given the limited information about the service at the time of fielding, our recent survey indicates only marginal appeal for the service beyond existing HBO subscribers; this interest is likely to be further depressed in uncertain economic times, especially if the service is missing some of its planned marquee launch programming (for example, the eagerly anticipated “Friends” reunion).

![]()

Can Peacock fly without the Olympics? NBCUniversal was (and reportedly still is) planning to launch Peacock this month, with a free ad-supported tier, a premium “limited ads” tier and a $10/month ad-free tier. Our survey suggests that the ad-supported version of Peacock shows decent potential uptake, but there was limited consumer interest in the ad-free version. That’s likely what NBCUniversal is aiming for, though, prioritizing the (potentially better) AVOD economics ahead of fighting over highly competitive SVOD dollars. However, despite a reported 15,000 hours of original and library content at launch, the service was relying heavily on the Olympics to give it an early boost. Launching without Olympics content will create a massive dent in advertising revenue and likely inhibit consumer demand.

![]()

Then there’s the recently launched Quibi, which delivers something altogether unique — original programming with episodes capped at 10 minutes or less (hence the moniker “quick bites”). Available in mobile form only, Quibi seems pitched mainly at Gen Z and some millennial consumers and is priced accordingly ($5 monthly with ads, $8 without ads). Though our research suggests that initial interest will be somewhat muted (though our survey fielded in December 2019 before any major marketing efforts by the company and did not include respondents under 18), compared with other services, Quibi offers true differentiation, and as such bears watching going forward. However, as with the other new launches, the pandemic and associated self-isolation may cause problems — it’s not ideal to launch a service designed for mobile consumers who are “on the go” when everyone is stuck at home. That being said, it appears Quibi will not be affected by production stoppages — management stated in late March that only two shows will be delayed and that all other planned shows will be available as scheduled.

Strategies for streaming success

As the OTT world grows increasingly crowded and competitive, being successful will vary among both traditional and digital media players. Those who succeed will be those with a clear and well-defined streaming strategy. Ultimately, content is still king in the OTT world, both in terms of quality and volume, and without killer content success will be hard to come by. But consumers are showing a willingness to add to their SVOD stack, suggesting that there is room for new and existing services to play. Success, however, has a few key prerequisites.

Content. In the world of OTT, content is everything, requiring that players not only have consistently high-quality programming but also sufficient volume. Services must deliver enough compelling original/exclusive content along with sufficient breadth so that subscribers can find something to watch each and every time they log in.

Understanding and defining your audience. Disney+’s success has been driven, at least in part, by its clear appeal to families. Quibi too has a strategy that appeals to a unique and well-defined audience (Gen Z and young millennials). Successful services will have a deep understanding of their target audience(s) and focus content, product and marketing efforts accordingly.

Make it easy. Streamlining the user experience can also be a differentiator. An intuitive user interface can help a service stand out among the crowd. And a better search and recommendation engine can solve the “decision paralysis” that accompanies many services today.

Convert free trials and manage ongoing churn. Once the restrictions on travel and out-of-home entertainment are lifted, consumers may look to slim their OTT stack down to pre-COVID-19 levels. Make your service indispensable through a well-thought-out and clearly communicated future slate of high-profile content releases, longer-term offers, and a finely tuned recommendation engine that makes consumers believe they still have plenty of content to get through before running out of something to watch.

Price pack architecture. Finally, the proper business model is important. Will your audience accept ad breaks included in an AVOD model in return for a lower monthly fee? (Spoiler alert: Our survey says the answer is probably “yes.”) Are they willing to pay more for higher fidelity streams? Refining your pricing, packaging and tiering through a well-thought-out price pack architecture strategy is key, especially as services move away from a standard $10/month pricing.

For a broader review of how the COVID-19 pandemic is impacting the media sector writ large, take a look at additional perspectives from our colleagues around the globe: Hours Up, Dollars Down: COVID-19’s Impacts on the Media Sector to Date.

07302021140737