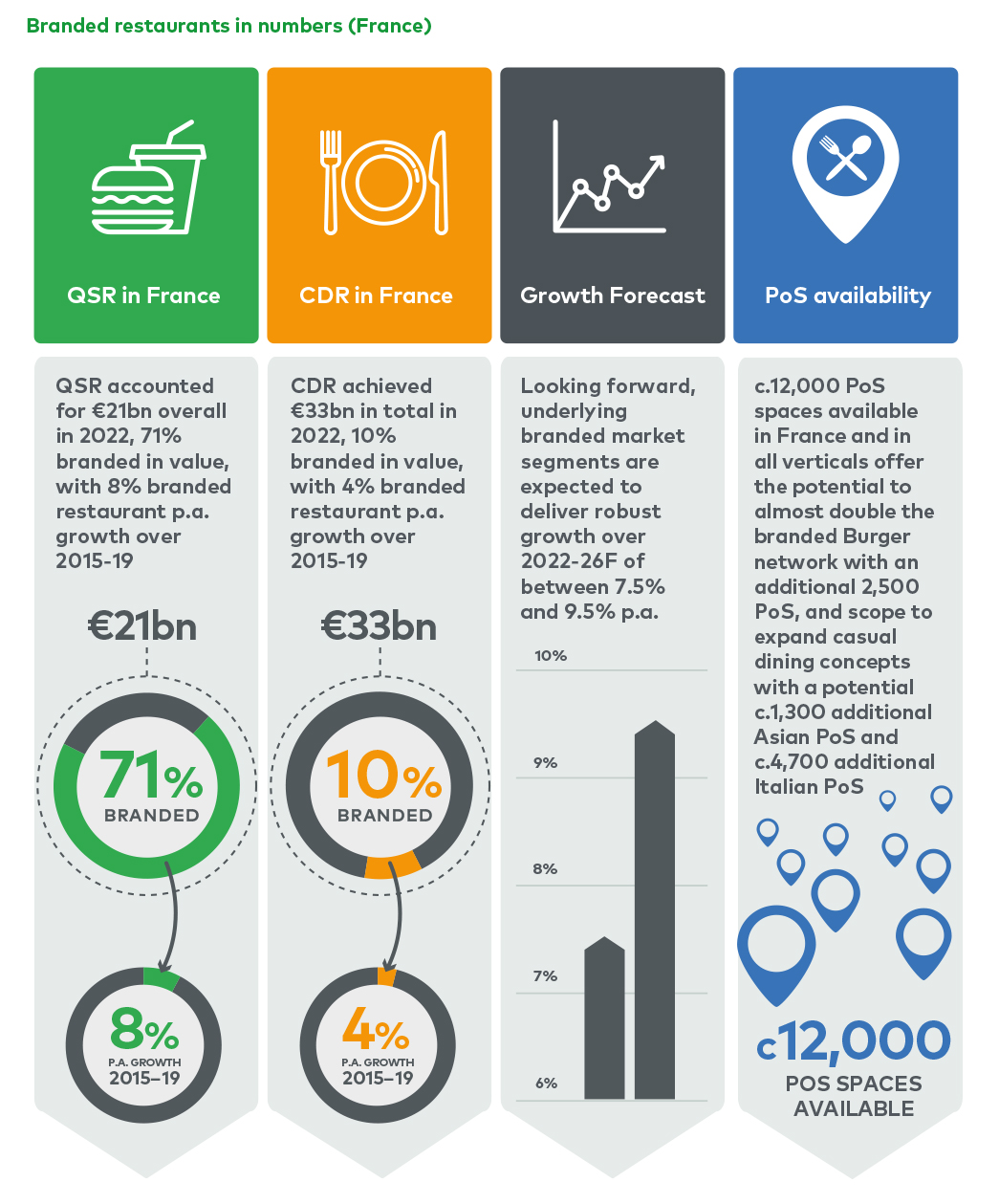

Taking a closer look at the French market helps to create a better understanding of the dynamics at play. The French restaurant market is considerable, worth €54bn in 2022. Positive demand and supply side trends such as consumer time poverty and an increase in out-of-home meals ensured continued growth at a rate of c.5% p.a. in the run up to COVID. Lunch vouchers, new consumption movements, new cuisines, a desire for quality eating and omnichannel development allowing home delivery, click and collect, takeaway and drive- throughs have all played a part in supporting this growth.

Brands have grown even faster, at 7.0% p.a. pre-COVID (2015-19), and branded restaurants in both QSR and CDR categories accounted for c.€19bn of the market in 2022, beating pre- pandemic highs. Convenient and affordable, QSR burger is the leading market segment, with the highest share of brands and franchises backed by strong growth and resilience. Similarly, in the casual dining segment, brands offering concepts such as Italian, Asian, and Grill are steadily gaining share over independent restaurants.

Franchising — the recipe for success?

Branded concepts offer a range of advantages for consumers including affordability, quality, and consistency, while for operators they provide the opportunity to industrialise to drive efficiencies. Even in casual dining, consumer preference for branded propositions is robust, creating significant headroom for expansion and new market entrants. Network growth is helping brands to grow faster than the overall restaurant market with franchising the main enabler. Franchising is attractive to both franchisors and franchisees. For brand owners the efficient, fast rollout, more productive franchising income and capex-light development all help to create strong value. While for entrepreneurial franchisees turnkey concepts with well-known brands generating traffic from day one, coupled with strong operational support and robust economics make for an attractive business proposition.

Within the French franchise market, the restaurant segment for both QSR and CDR was the third largest in value in 2022 (c.€9bn) after the Grocery (c.€28bn) and home equipment categories (c.€9bn). Franchised restaurants have outperformed franchise industry averages, growing at an overall c.7% p.a. in value over 2015-22 vs. 5% for all franchises, and QSR performing particularly strongly at 8% p.a.

How the advantages of brands add up

Brands offer valuable scale – providing not just market leading capabilities such as development, franchising, roll-out, marketing, operations, procurement, market intelligence, information systems and M&A, but also the bargaining power to maintain lower rents, discounted bank loans rates, cheaper F&B and utilities costs, and advantageous terms with delivery partners. The end result is a price competitive advantage that independents struggle to match.

While COVID did cause a short-term decline in the French restaurant market, branded concepts and QSR resisted better than independents and casual dining restaurants. Value for money, adaptability to omnichannel, trusted and consistent products, and better economies of scale have all contributed to this resilience.

Conclusion

Whether investors are attracted to the clear white space for category penetration offered by QSR, or by the gradual displacement of independent CDR restaurants over time, all can look forward to a menu of opportunities across the European branded restaurant sector. Recognising how and when to take advantage of these opportunities can take knowledge and expertise. To hear more about our work in this exciting sector, please contact a member of the team.