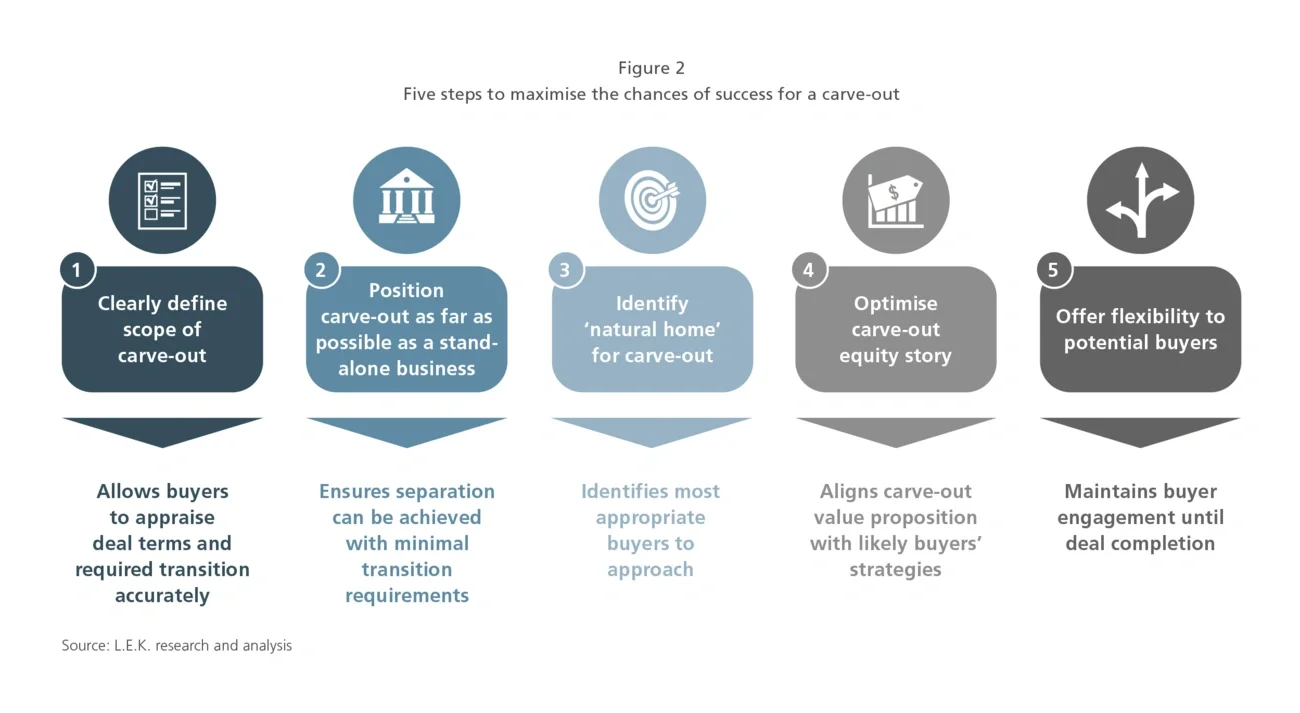

4. Optimise the carve-out’s equity story for its identified natural home

- Once the carve-out’s natural home has been identified, the seller should refine its value proposition and promote the business to the most appropriate buyers/investors.

- It is crucial to outline the benefits to buyers, in particular how they could gain from the addition of the portfolio (e.g. through synergies, cross-selling effects).

- Where necessary, minimal scope/transaction perimeter refinements may be considered to reduce friction for a potential buyer (e.g. apportioning additional shared services with the carve-out to ensure operational independence is maintained).

5. Offer flexibility to potential buyers

- Early management interaction should be offered to buyers to identify their specific needs and requirements and to keep them engaged throughout the process (e.g. often informal discussions or expressions of interest may precede the formal process or even prompt the seller to consider the carve-out).

- Potential scope refinements and changes in the deal structure should be anticipated in advance (e.g. optionality around geographies or groups of products) and offered to buyers, if feasible, to maximise the chances of deal execution. However, care must be taken to ensure the remaining portfolio is attractive to other potential buyers.

Strategic focus before as well as during the carve-out process is vital

Many carve-outs or divestments do not materialise, require multiple attempts to achieve a sale or take several years to complete. The culprit is often faulty execution rather than a change in strategic direction.

External, strategic support is valuable throughout the carve-out journey to facilitate execution and ready the asset for formal due diligence scrutiny. Specifically, we find strategic support to have the most impact in five key areas:

- Asset strategic review and vendor due diligence to provide a third-party perspective and articulate the value proposition

- Organisational planning to prepare for the transition

- Identification of suitable buyers

- Negotiation support

- Deal terms modelling to understand the potential value creation for the carve-out