The renaissance of healthcare logistics

Healthcare logistics sits at the intersection of three durable forces: structural healthcare demand, rising therapy complexity and rapid digital enablement. Regulatory intensity, specialized infrastructure and high consequence of failure create defensible barriers to entry, while fragmentation creates consolidation opportunity and AI creates disruptive growth and value creation potential.

For strategics, the imperative is capability acquisition before valuation multiples and competitive intensity rise further. For private equity, healthcare logistics offers recurring revenue, margin durability and clear buy-and-build pathways. For founders, the market presents a generational opportunity to institutionalize and scale highly attractive, mission-critical businesses.

As healthcare logistics becomes not merely a delivery mechanism but a determinant of clinical success, the segment should be on the radar for strategics and investors across the ecosystem.

The next phase of value creation will be defined by those who recognize this shift and act on it decisively.

Healthcare logistics at an inflection point

Healthcare represents approximately 10% of global gross domestic product with spending growing at 5%-plus annually in many markets. It has long attracted investment due to its structural resilience, regulatory barriers and persistent inefficiencies. As urgency from the ballooning costs of an aging global population is paired with technological advances, many segments of the healthcare market are seeing significant investment and transformation. Historically, healthcare logistics has been relatively overlooked by investors, but no longer.

The healthcare supply chain is an extremely demanding logistics environment. Precision, compliance and speed are nonnegotiable. Billions of dollars in life-critical products move daily across manufacturers, distributors, 3PLs (third-party logistics providers), freight forwarders and last-mile specialists, under strict service levels and regulatory oversight. A variety of factors have accelerated the need for maturation of the healthcare logistics ecosystem, including supply chain shocks from COVID-19; ongoing geopolitical volatility; margin pressure in pharmaceuticals, medical devises and diagnostics manufacturers; and the consolidation of healthcare providers into larger, more sophisticated customers.

Furthermore, technology advances are unlocking new operating models to transform logistics from an asset-heavy service function into a data-driven, insight-led platform opportunity. Consequently, what was once viewed as a niche extension of general freight is increasingly recognized as a high-margin, defensible and strategically critical vertical.

This report is one of three total pieces co-authored by L.E.K. Consulting and Lincoln International, delves into why we believe the market is witnessing an inflection point in the evolution of the healthcare logistics market, which provides a unique opportunity for investment.

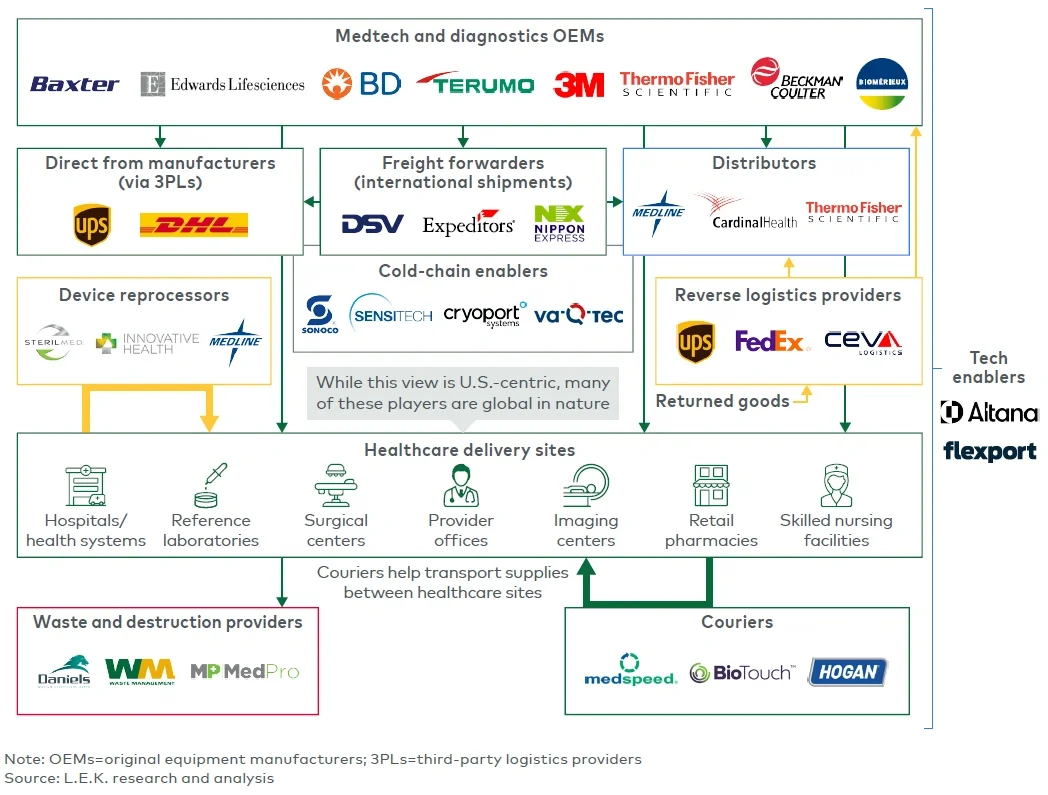

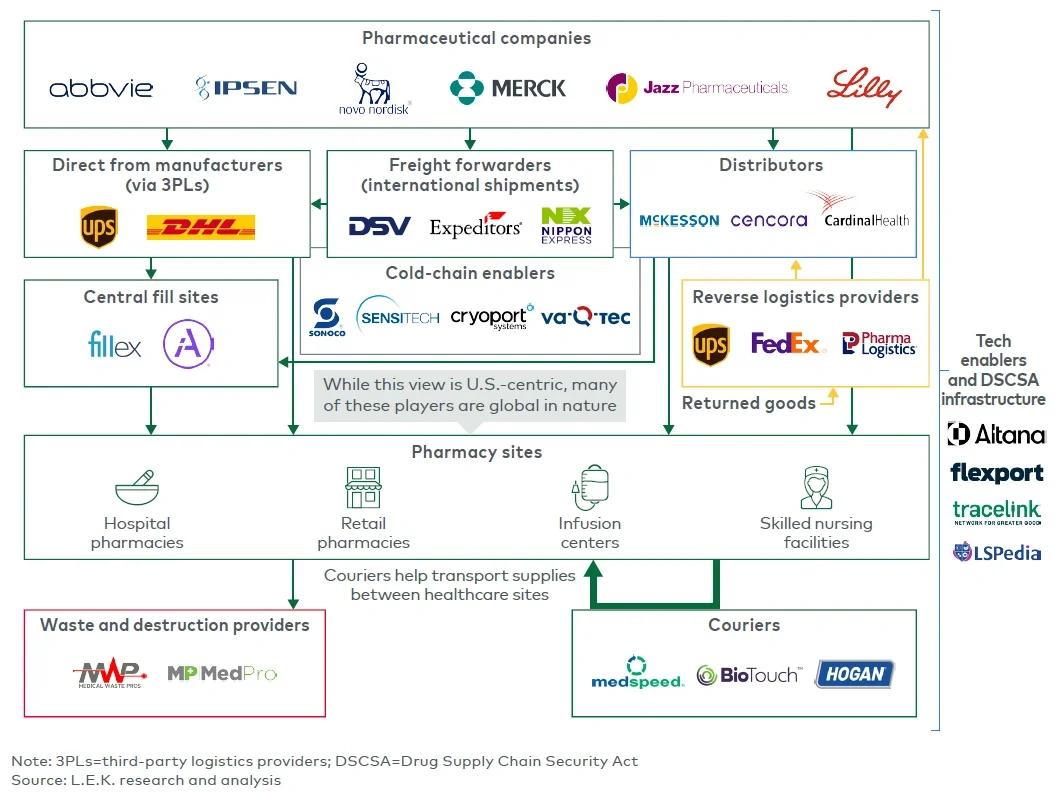

A mapping of the healthcare logistics ecosystem

Healthcare logistics is not a single market but rather an interconnected set of market sub-segments with specialized operators managing the flow of products and information between manufacturers and providers (see Figures 1 and 2).