What should provider organization leaders do now? We recommend the following:

Catalog current research activities. Many provider organizations do not have a full understanding of current research activities, costs and value.

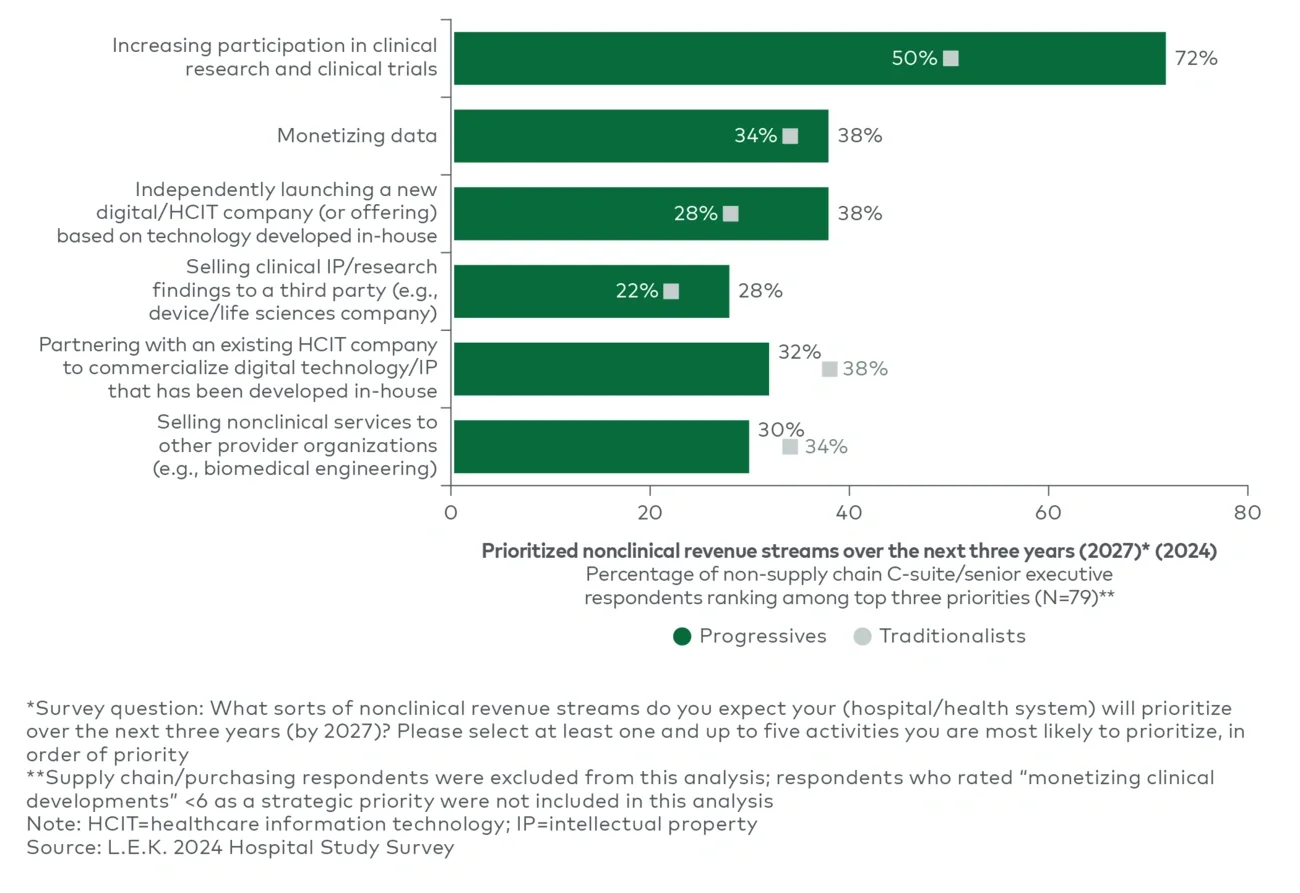

Conduct gaps assessment. Identify capability gaps and blockers to increased clinical trial participation as well as opportunities to close these gaps.

Define priority service lines and target manufacturers. Prioritize research focus based on clinical needs and value to the community and the system, and identify and open discussions with manufacturers that are active in those spaces.

Forge (flexible) partnerships to start to build out the infrastructure. Select and onboard partners to close identified gaps and scale infrastructure (from point solutions to contract research organization partners) but retain flexibility in a fast-changing space.

4. Driving specialty pharmacy and embedding precision medicine at the point of care

U.S. prescription drug expenditures are projected to reach $2.5 trillion by 2035, surpassing one-quarter of total U.S. healthcare spend. This growth will continue to be driven by targeted and high-cost specialty drugs, especially as gene and cell therapies, biologics, and targeted treatments become more prevalent.

To succeed in 2035 — in terms of both patient outcomes and financial sustainability — provider organizations will need to effectively participate in this growing area.

Additionally, genomics is no longer the exclusive domain of academic centers or disruptive startups. Community-based health systems and physician groups are beginning to weave genetics into everyday decision-making, gaining access to the $3 billion data and insights spend pool (across biopharma, provider and payer use cases). Yet we believe the lion’s share of value will accrue to organizations that move beyond test volumes and focus on clinical activation and driving clinical value.

What leading provider organizations will master |

|---|

| Specialty pharmacy operations | Successful providers will develop exceptional patient access (for medical and pharmacy benefit drugs), inventory management and procurement infrastructure (including direct contracts with manufacturers) |

| Clinical integration of precision medicine | Genomic sequencing and AI-driven diagnostics will enable more-personalized treatment plans, particularly in oncology, neuroscience and rare diseases but increasingly in primary care |

| Patient access and convenience | Successful providers will develop patient access points that are convenient and cover the spectrum of specialty drug routes of administration (e.g., ambulatory infusion, home, in office) |

| Strategic 340B and network optimization | As the 340B program evolves, health systems will need to adapt their pharmacy networks and contract strategies to maintain compliance and financial viability |

| Proactive drug pipeline intelligence and life sciences partnerships | Given the speed at which new therapies enter the market, leading providers will need to have deep visibility into drug pipelines and partner with manufacturers to ensure access |

What should provider organization leaders do now? We recommend the following:

Prepare proactively for various 340B scenarios with a clear action plan to follow should various potential changes to the program be enacted.

Proactively embed genomics at the point of care to capture an outsized share of a rapidly growing market and create data assets competitors can’t match (see our recent learnings regarding how to approach this).

Assess the drug pipeline to identify therapeutic areas and manufacturers around which to build new relationships and programs in the coming years.

Assess current specialty pharmacy operations, particularly related to drug access, patient access/authorization timing, revenue and acquisition cost.

Chart a path to close any identified gaps in current operations (relative to benchmarks and best practices), including potential partnerships.

Build out the delivery footprint, potentially with ambulatory and home infusion operating partners (especially as investment in these industries continues).

5. Establishing the supply chain as a competitive advantage

Supply chain inefficiencies don’t just impact margins — according to the American Hospital Association, in 2024 39% of providers canceled patient appointments due to product shortages.

In today’s complex healthcare landscape, mastering the supply chain is essential. Providers that integrate supply chain intelligence with financial and clinical operations gain cost advantages, operational stability and better patient outcomes. Those that fail to adapt face higher costs, inefficiencies and care disruptions.

By 2035, supply chain mastery will define high-performing organizations, evolving from a back-office function into a strategic pillar of financial sustainability and care delivery.

What leading provider organizations will master |

|---|

| Integrated clinical and financial supply chain systems | Real-time interoperability between supply chain, finance and clinical data will enable better cost control, inventory management and service continuity |

| Resilient and dynamic procurement and sourcing strategies | AI-driven demand forecasting, vendor diversification and proactive contract management will reduce cost variability and exposure to disruptions |

| Tech-enabled cost containment | Automation, AI-driven procurement tools and predictive analytics will help control rising material and operational costs |

| Postacquisition integration excellence | As provider organizations continue to grow through M&A, supply chain optimization offers a real value-creation lever |

What should provider organization leaders do now? We recommend the following:

Assess the potential impact of tariffs and identify potential alternate sources to manage down supply costs if necessary.

Assess the current supply chain for resiliency and identify opportunities to diversify supplier networks and improve sourcing agility.

Start the work to integrate clinical and financial supply chain systems.

Identify, select and integrate AI-driven supply chain analytics to predict inventory needs, prevent stockouts and optimize procurement strategies.

Conclusion: The road to 2035 starts today

The healthcare providers that will lead in 2035 are already laying the groundwork today. Mastering these five areas — specialty pharmacy, AI, care delivery transformation, supply chain and research — will define the next era of healthcare leadership.

At L.E.K., we help provider organizations navigate these transformations with strategic clarity and execution expertise. To discuss how your organization can develop a roadmap to 2035, contact us today.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC