In early 2023, L.E.K. Consulting and the World Economic Forum released a special report on the outlook for global health and healthcare to the year 2035. This multipart series of L.E.K. Executive Insights builds on those findings and focuses on implications for the U.S. healthcare “provider” organizations — organizations that directly deliver healthcare services (health systems and hospitals, physician groups, post-acute care facilities, etc.).

Pressure is mounting to reduce healthcare spending (or ‘bend the cost curve’)

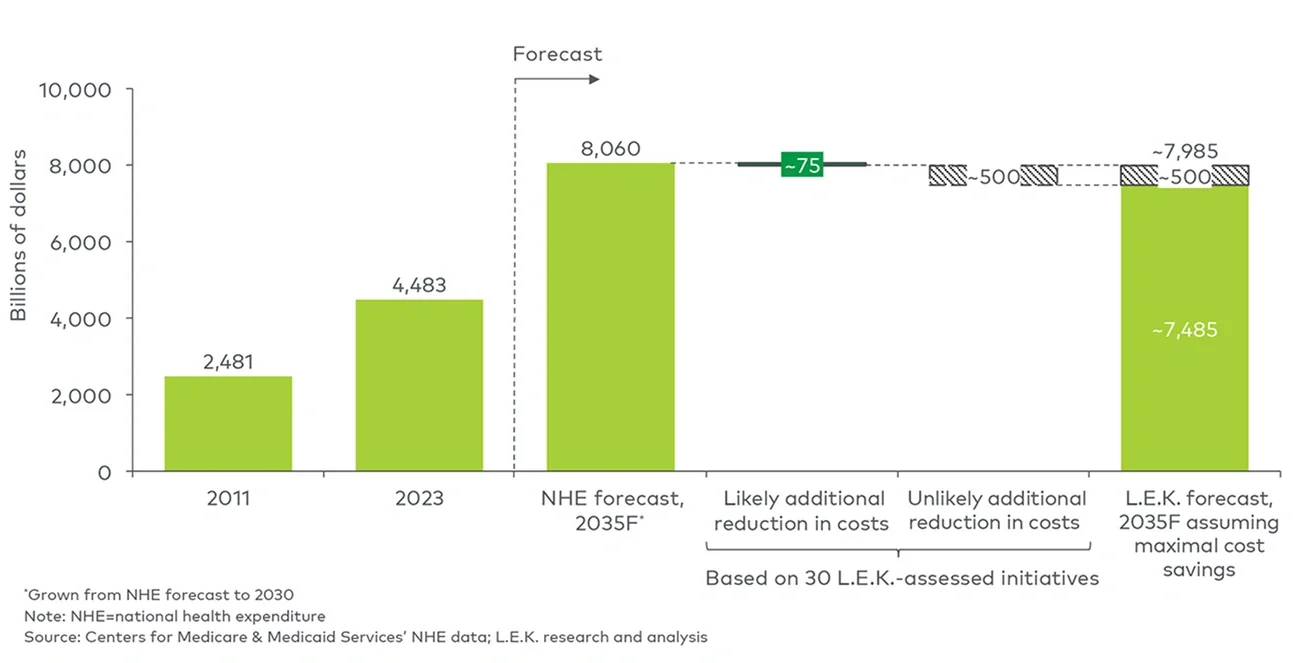

Annual U.S. healthcare expenditures have reached a new high of about $4.5 trillion. The U.S. spends more than 1.75x per capita on healthcare than other developed nations and still lags on key health indicators. Over the past decade, U.S. healthcare expenditures have risen by approximately 5% annually, consistently outpacing inflation (roughly 1.8% annually).

Beyond the impact of inflation, drivers of this upward trend — population aging and the increasing prevalence of chronic conditions (the primary driver) and the introduction of new (and costly) care innovations (a secondary driver) — show no signs of abating. Cost pressures such as labor and supply chain costs and clinician shortages also continue to challenge bottom lines.

At the current pace, U.S. healthcare expenditures may reach $8 trillion by 2035, more than 20% of forecasted total U.S. gross domestic product. While the principal goal of extending life remains paramount, public pressure is mounting to achieve better health outcomes at a lower per capita cost.

Potential cost limiters are either ineffective or unlikely to be implemented

The transition to value-based care and the introduction of new technologies have positively impacted the U.S. healthcare ecosystem but have yet to deliver a meaningful reduction in total U.S. healthcare spend. Employers and public plan sponsors (e.g., the Centers for Medicare & Medicaid Services (CMS) and other federal/state agencies) are ultimately best positioned to place downward pressure on healthcare spend, but structural impediments (e.g., employer fragmentation, risk for employee/constituent abrasion) have prevented both groups from effecting significant change.

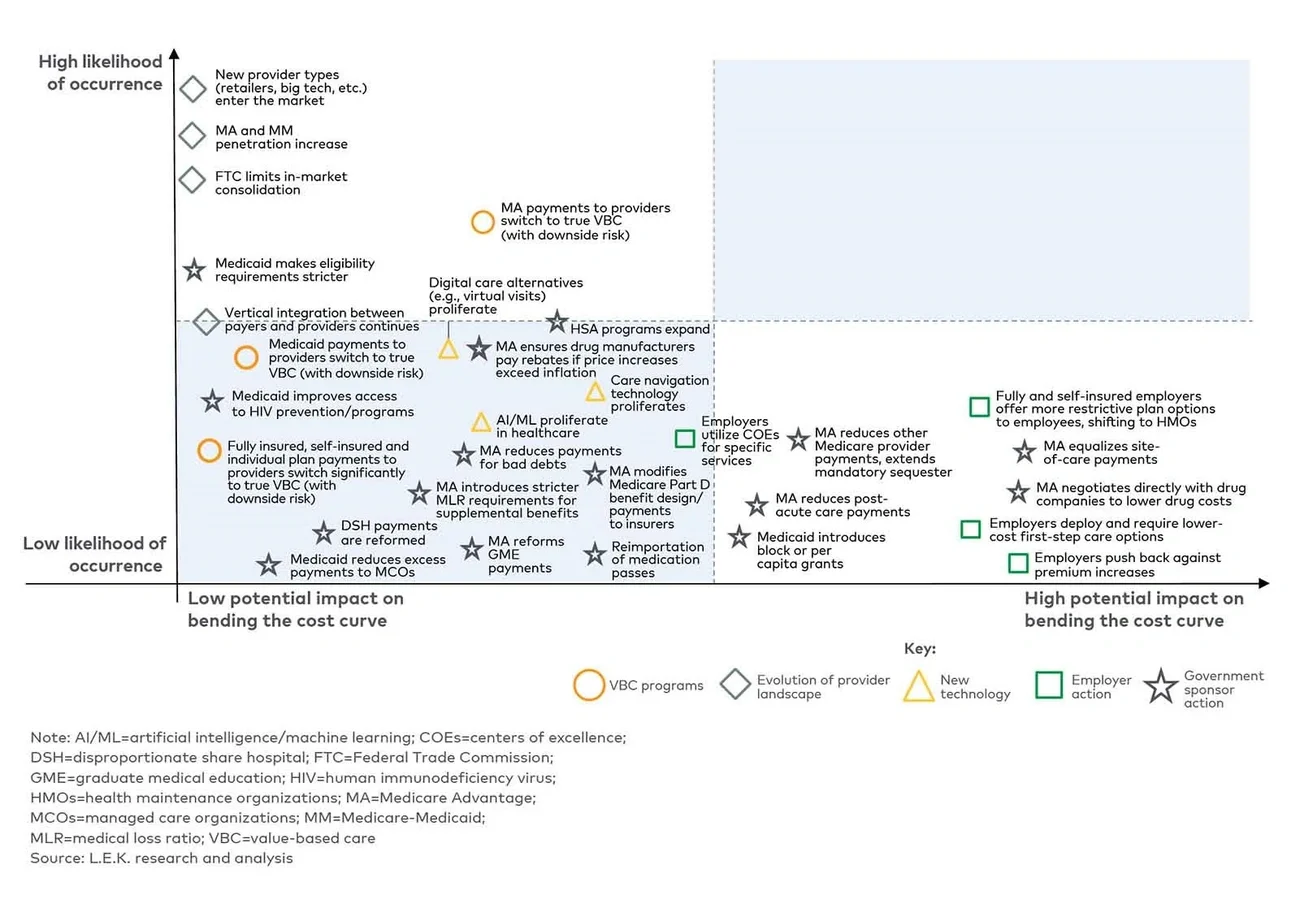

To evaluate whether a significant reduction in healthcare expenditure is likely by 2035, L.E.K. analyzed the magnitude and relative implementation probability of 30 in-flight or potential spend-reducing initiatives.

We found that while these 30 initiatives could drive an approximate $500 billion reduction in healthcare expenditure by 2035 (representing around 6% reduction in spend), the impact is likely to reach a more modest $75 billion (a roughly 1% reduction in spend) as the most significant spend-reducing actions are unlikely to be implemented.

While they are unlikely to yield a significant reduction in spend, many of the initiatives outlined below will drive continued market evolution and a redistribution of spend across healthcare market segments, with the large and ever-growing healthcare market continuing to attract investment and innovation (see Figure 1).