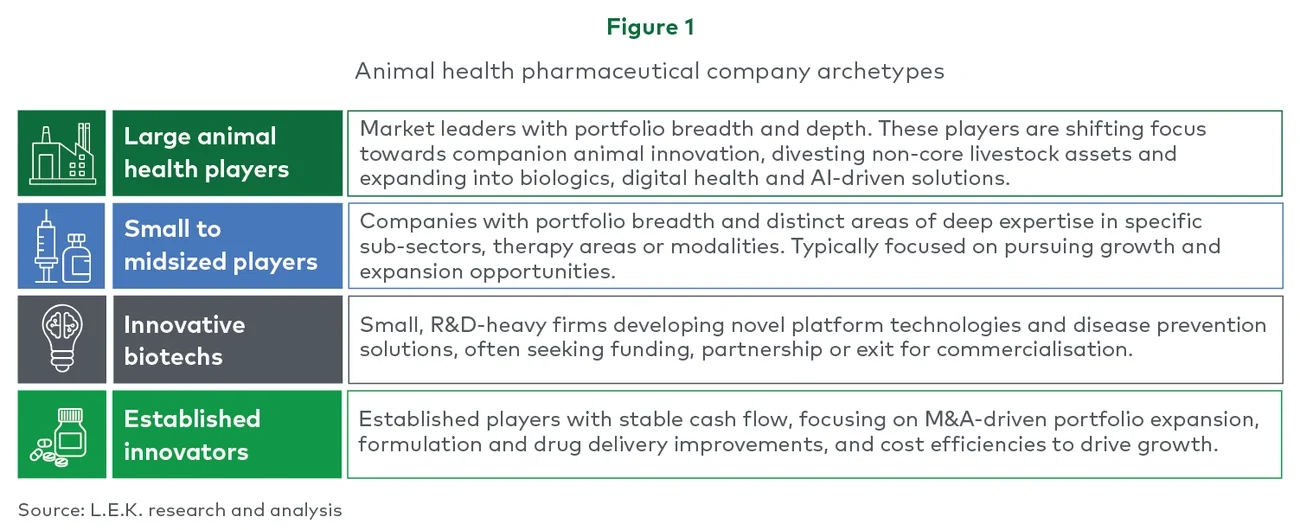

Large animal health players: Market leaders with overall portfolio breadth and depth

The animal pharma industry is led by a dominant group of successful multinational companies — including Zoetis, MSD Animal Health, Boehringer Ingelheim and Elanco — that have driven sector growth and fuelled innovation, both organically and inorganically.

Although these large players continue to serve both companion and livestock segments, their strategic focus in recent years has increasingly leant towards advancing the companion animal market. Several important factors have generated this shift.

First, the companion animal market has demonstrated superior growth potential, triggered by increasing pet ownership, the rising tendency to treat pets as family members, the escalating penetration of pet insurance and a growing prevalence of chronic conditions in ageing animals. In response, leading animal pharma players have ramped up investment in innovative therapies, such as monoclonal antibodies, cell and gene therapies, and AI-based diagnostics tailored to treating and prolonging the lives of pets.

At the same time, the livestock pharmaceutical segment faces mounting economic and regulatory pressures, contributing to relative deprioritisation of certain areas. Concerns over sustainability and antimicrobial resistance have led to stricter regulations on antibiotics use, even as changing consumer preferences for plant-based and food-technology alternative proteins and reduced meat consumption in some regions have constrained market expansion.

Moreover, livestock producers operate in a price-sensitive environment, limiting their ability to absorb cost increases and reducing margins for pharma companies. As a result, while large actors continue to invest in livestock health, they are focusing more and more on complementing their strongest livestock portfolios and developing higher-value innovations, such as vaccines, precision livestock farming and sustainability-related solutions.

This strategic shift has also led to the divestment of some non-core livestock businesses, freeing up capital for investment in high-growth companion animal segments.

Zoetis’s recent M&A activity can be viewed as a case study for this trend. In 2022, Zoetis acquired a Cambridge (UK)-based animal biotech, PetMedix, that develops antibody drug candidates, targeting areas of unmet clinical need in addressing both chronic and terminal diseases that affect dogs and cats. Then, in 2024, Zoetis agreed to divest its medicated feed additive portfolio to Phibro Animal Health for $350 million, allowing Zoetis to prioritise higher-value solutions, including vaccines, biologics and genetic programmes.

Small to midsized players: Portfolio breadth with distinct areas of expertise

Midsized animal pharma companies typically blend portfolio breadth with distinct areas of deep expertise in specific sub-sectors, therapy areas or modalities, whereas smaller players tend to concentrate on a certain geography, sub-sector, or set of therapy areas and modalities, and use this as a base for further expansion and growth.

Companies in this category usually operate with a leaner R&D budget and emphasise market expansion and cost efficiencies. Unlike larger animal pharma companies, they are less likely to divest assets, and instead actively seek scale advantages through acquisition and partnership.

For example, Ceva Santé Animale, one of the largest midsized players, has significantly grown its livestock biologics business through acquisitions while also expanding its companion animal business through the 2024 acquisition of pet biotech Scout Bio. Huvepharma's acquisition of AgriLabs in 2018 likewise strengthened its foothold in the US livestock pharma sector.

Innovative biotechs: Developing a pipeline and partnerships

The animal biotech sector, while smaller than its human counterpart, is sparking greater interest due to its potential for breakthrough therapies. These biotech companies are developing clinical pipelines with a variety of novel therapies, including cell and gene therapies, biologics, vaccines, and alternatives to traditional antimicrobials.

Companies such as LEAH Labs are working on CAR T-cell cancer therapies for companion animals, for example, while Anivive is leveraging AI to accelerate drug development in this space.

Though they sometimes lack the resources to scale and commercialise their innovations independently, this can make innovative biotechs attractive acquisition targets or partnership propositions for established industry incumbents and savvy strategic investors.

Take Kindred Biosciences, for example, which developed a deep pipeline of novel biological therapies for companion animals before being acquired by Elanco for $440 million in 2021. This acquisition — along with Ceva’s purchase of Scout Bio, among others — highlights the appetite among large players for de-risked, late-stage biotechs that can complement their portfolios.

Animal biotech companies are also pursuing innovation in the livestock sector, such as publicly listed ECO Animal Health, which has produced next-generation antibiotics for pigs and poultry that meet current guidelines for responsible use of antimicrobials.

Established innovators: Building portfolios via M&A and incremental innovation

Legacy brand and generics companies and other established innovators often rely on product lifecycle management strategies, such as incremental innovation in formulations or delivery mechanisms. They often seek to expand geographically in order to sustain or build market presence, or acquire smaller generics companies or license successful legacy brands to augment their portfolios and improve operational efficiencies.

With products already established in the animal treatment paradigm, these companies can turn stable, cash-generating growth into opportunities for investment in either M&A or comparatively low-spend, incremental R&D.

Norbrook, a Northern Irish manufacturer of differentiated veterinary pharmaceutical products, has steadily boosted its generics range, manufacturing capabilities and geographic reach alike through targeted acquisitions. And Chanelle Pharma, acquired in 2024 by UK private equity firm Exponent for an estimated €300 million, has assembled one of the largest animal generics portfolios in Europe, leveraging its R&D expertise to generate data for new registrations and its extensive manufacturing capabilities to scale production globally across a range of dosage forms.

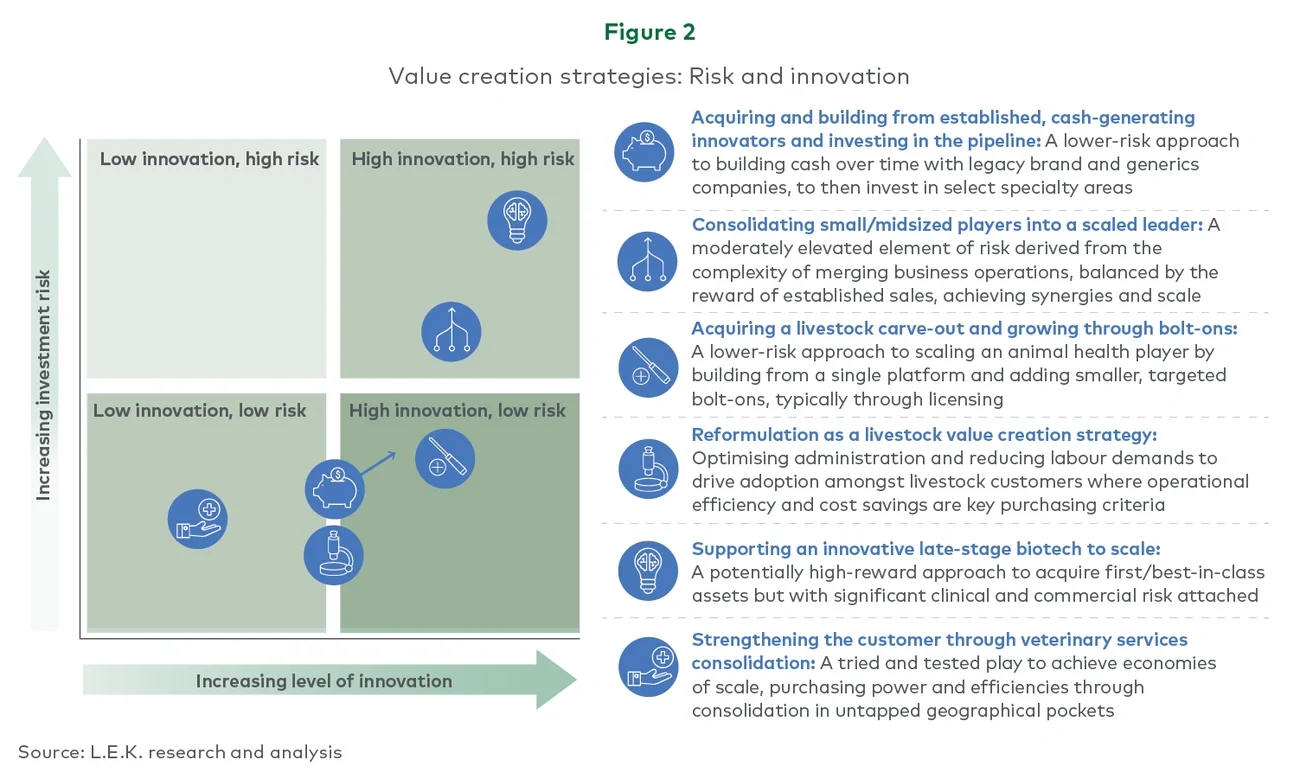

Investment strategies for growth and value creation

Within the shifting landscape of animal pharma, CEOs and investors can pursue a range of strategies to build value in the sector. Each of the four archetypes described above presents different opportunities for acquisition, consolidation and growth. L.E.K. has explored several strategic investment plays that align with market trends and show potential for strong returns (see Figure 2).