In most states, managed services organizations (MSOs) let investors deploy capital into law firms without violating ethics rules that prohibit nonlawyer ownership. Recent regulatory opinions have clarified how these structures can work within existing rules.

For more on how MSOs are structured, see Part I of our series. Part II focuses on the investment case: deal economics, practice area fit and what separates successful platforms from failed ones.

MSO payment models

MSO investors deploy capital through infrastructure acquisition (office leases, technology systems, equipment, operational contracts) and growth investments (marketing spend, intake operations, business development). The MSO is compensated through a management fee defined in the management services agreement.

Two payment structures dominate:

Flat-fee model: A midsize firm generating $20 million in annual revenue might pay an MSO $18 million annually to handle all nonlegal operations. If the MSO’s actual costs are $15 million, it earns $3 million in profit while the firm retains $2 million. The fee remains fixed regardless of firm performance.

Cost-plus model: A smaller personal injury practice with $5 million in revenue might use cost-plus pricing, reimbursing the MSO for operating costs plus a 15% margin. If the MSO invests $8 million to scale marketing, driving firm revenue to $12 million, the MSO earns $1.2 million in profit. The structure remains compliant because the margin is fixed, not tied to legal revenue percentages.

The critical variable is durability. Investors underwrite the management services agreement as the foundation, typically a long-term contract with renewal and termination protections. Since the MSO fee is paid before partner distributions, successful deals build alignment through fair market value fees, scope adjustment terms and rollover equity.

Value creation at the MSO level

Returns come from two mechanisms:

Margin expansion: Operational efficiencies from standardized processes, vendor negotiations and technology deployment allow the MSO to reduce costs while maintaining service levels.

Platform scalability: Shared services across multiple firms or practice groups create economies of scale. Centralized intake, unified technology systems and consolidated vendor relationships spread fixed costs across a larger base.

Practice area characteristics determine where these mechanisms create the most value.

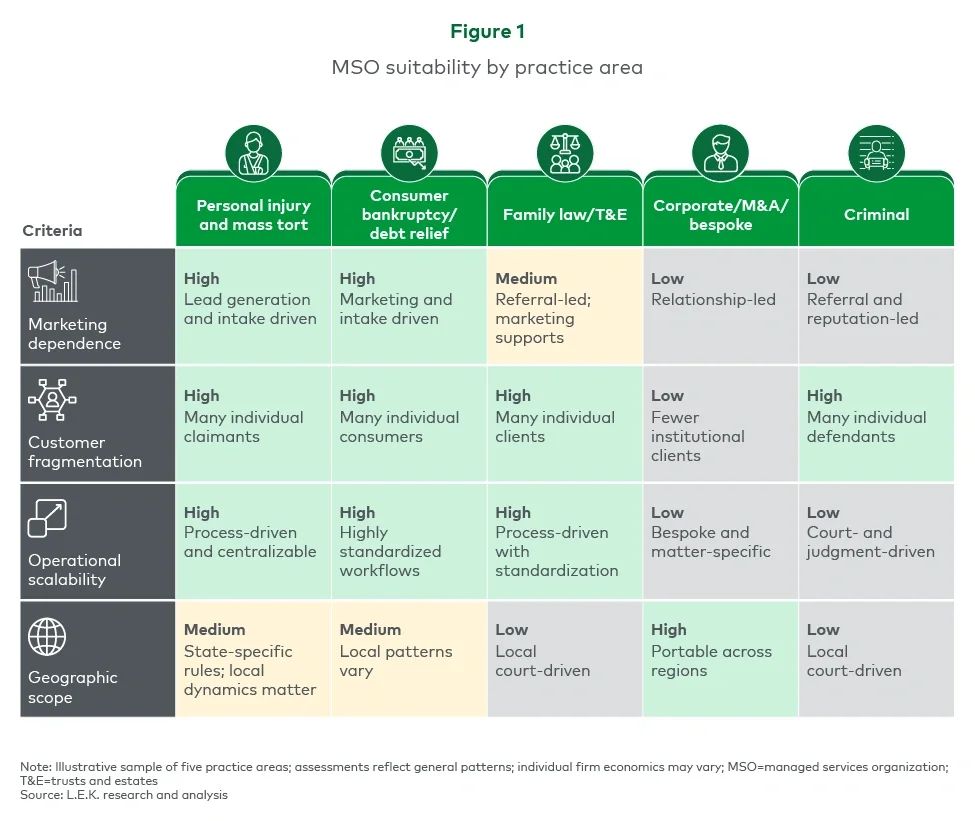

MSO suitability by practice area and investment criteria

Not all legal practices benefit equally from MSO dynamics. Practice areas can be evaluated for fit across several criteria, including:

- Marketing dependence: The degree to which scalable marketing investments generate client flow as opposed to relationship-driven or referral-based acquisition

- Customer fragmentation: Whether the practice serves a high volume of individual clients or concentrates on fewer, larger relationships

- Operational scalability: The degree to which workflows are repeatable and can be standardized across cases

- Geographic scope: Whether the practice can operate across multiple jurisdictions or is tied to local courts and relationships

Evaluating a nonexhaustive sample of practice areas illustrates how these criteria shape MSO fit (see Figure 1).