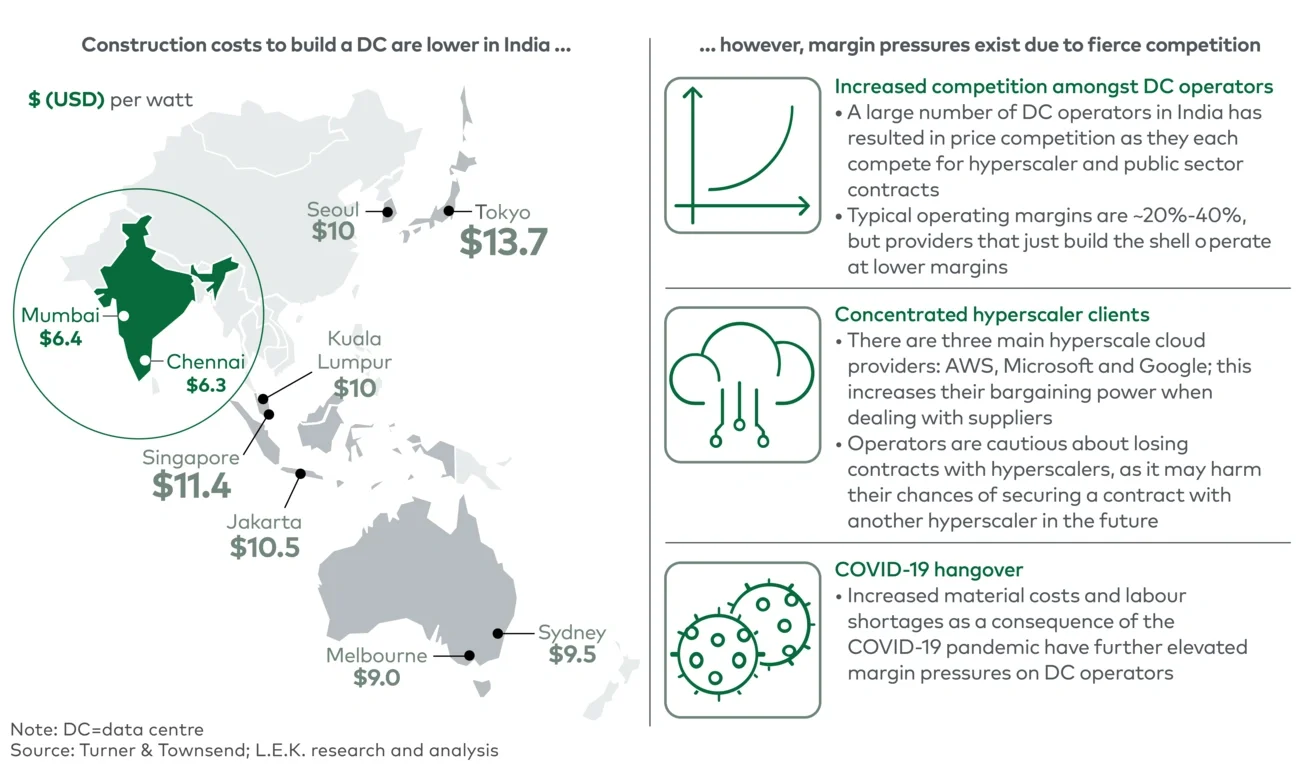

Introduction

India’s DC industry stands as a critical pillar in the country’s digital transformation. Experiencing significant growth in recent years, it has entered a high-velocity market phase marked by new technologies, evolving models and intensifying policy focus.

Recognising the overlooked potential in this space, L.E.K. Consulting has developed an extensive market primer helping decision-makers evaluate India’s accelerating DC landscape.

This edition of Executive Insights summarises the key highlights from our primer to equip stakeholders with actionable insights on India’s DC sector. We touch upon the market overview, growth catalysts and outlook shaping this rapidly developing industry. We hope to arm decision-makers with concise intelligence to take advantage of the substantial opportunities this market offers.

Key demand drivers

India’s DC industry is at an important juncture, where strong underlying demand drivers are converging with strong policy catalysts to propel growth potential over the coming decade. Despite India still being in the early stages of digital development compared with its global peers, the market fundamentals signal an inflection point where the stage is set for rapid acceleration to meet the country’s digital infrastructure needs.

The key factors propelling this bullish thesis are:

- Digitisation – Annual GDP expansion of 5%-7% and increasing tech spend will drive data demand. Consumer digitisation, with the internet reaching 99% of India’s population by 2030, fuels increasing need for data infrastructure.

- Cloud adoption – Public cloud spend in India is growing at 18% p.a. as software-as-a-service models are increasingly utilised due to increasing digital transformation. Data localisation needs are also contributing to DC growth.

- Supportive policies – Central and state governments are offering incentives such as land banks, electricity subsidies and tax breaks to boost digital infrastructure.

- Global connectivity – India’s strategic location and continued investment in subsea cables and expanding fibre networks enable global data access and exchange. This transformational growth in India’s DC industry will be underpinned by increasing data traffic, technological innovations, global tech ambitions and a favourable regulatory ecosystem.

Current market overview

Market size and key players

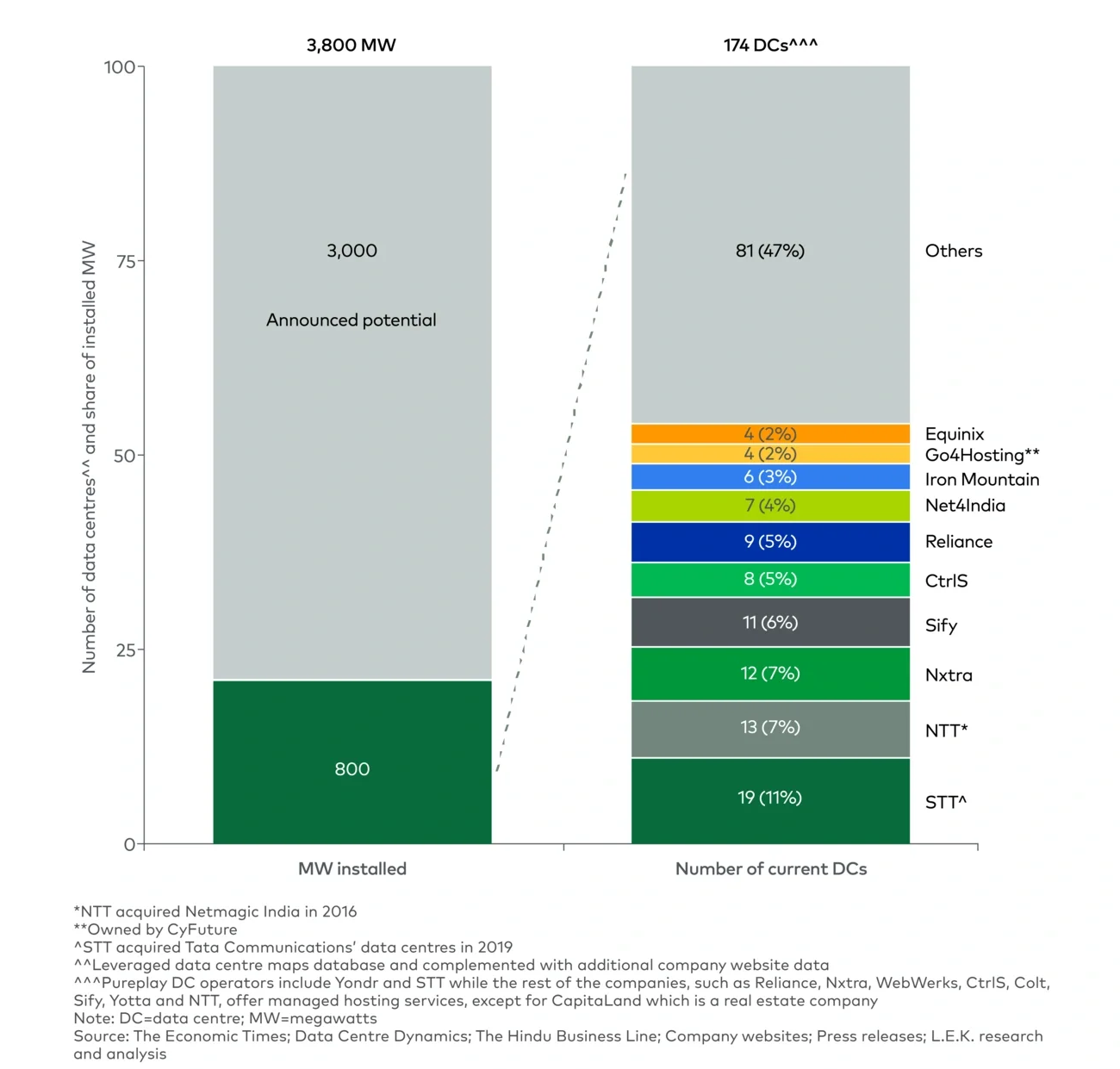

The Indian DC market has a current capacity of approximately 800 megawatts (MW), with the top five DC operators accounting for nearly 40% of this capacity. Investor confidence in the market is high, as demonstrated by operators’ future investment intentions, having disclosed plans to add 3,000 MW of potential DC capacity over the next few years, contingent on the realisation of announced plans and projects (see Figure 1).