In the 1980s, the UK achieved 2.2% per year improvement in productivity in real terms (i.e. above inflation). Whilst this growth may seem modest, it implies a doubling in labour productivity every 32 years, and therefore that a typical Generation X worker — born in the 1960s — could expect to earn double what their parents earned, even after taking inflation into account.

In the 1990s, the pace of productivity improvement increased, averaging 2.8% per year, or a doubling in productivity every 25 years.

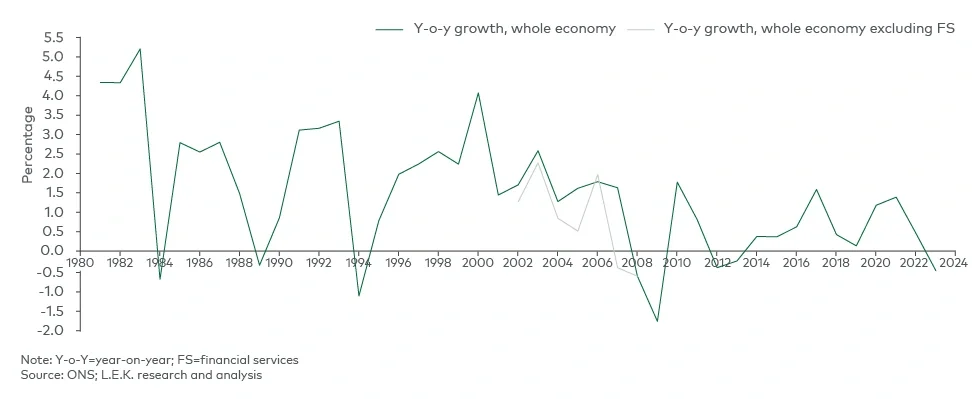

The global financial crisis of 2007-2009 (GFC) dominates the landscape of productivity growth in the 2000s and 2010s, and many have commented on the apparent step change that can be observed on either side of the financial crisis. From 2001 to 2007, productivity growth averaged 1.8%, and from 2010 to 2019 — in the wake of the GFC — it was only 0.4% per annum. (At this rate of growth, it would take fully 160 years to double productivity, which pushes the boundaries of economists’ understanding of ‘in the long term’.)

But is the GFC — and the constraints that it imposed on the availability of capital — at the heart of the decline? Perhaps not, and certainly not entirely.

What is less often observed is that this 2008 bust — which began in the global financial services (FS) sector — was preceded by an equally dramatic boom which saw the FS sector in the UK grow labour productivity by 55% from 2001 to 2007. Once the impact of this small element (noting that FS accounts for around 8% of the UK economy) is removed, the productivity growth in the rest of the economy was only 0.8% per annum from 2001 to 2007, equating to a doubling in productivity every 85 years — a lifetime, not a generation.

This is the UK productivity puzzle, and it seems to date from at least the early 2000s.

Generation Z children, born in the 2000s, are today graduating and entering a workforce that is barely more productive than when they were born. The problem is older than Facebook (2004), YouTube (2005) and Twitter/X (2006) — and indeed older than ‘Strictly Come Dancing’ (2004), ‘The Apprentice’ (2005) and ‘The X Factor’ (2005).

With all these new ways to communicate, to connect to information, and to find talent, why have we not solved the productivity puzzle?

There is a huge prize at stake. Had the UK’s productivity grown at the 1980s-1990s average rate (2.5% per year across both decades), today we would each be earning 36% more, or an extra £37 per hour.

But what are the causes?

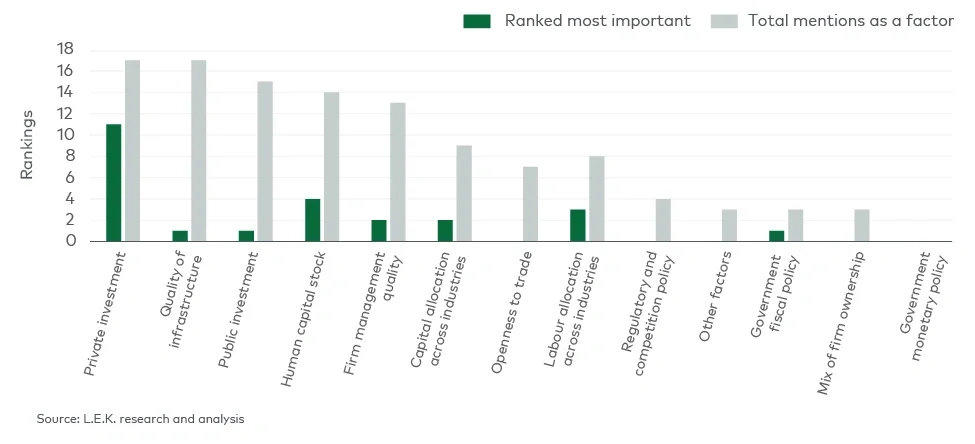

In a July 2024 survey of the literature and expert views, L.E.K. asked 26 UK academic experts on productivity for their views on the causes.2 The results are shown in Figure 2.