Australia’s economic conditions in 2024 presented significant challenges, impacting the M&A environment. Sector-specific dynamics and strategic investments shaped the landscape. We have made three key observations:

Observation 1

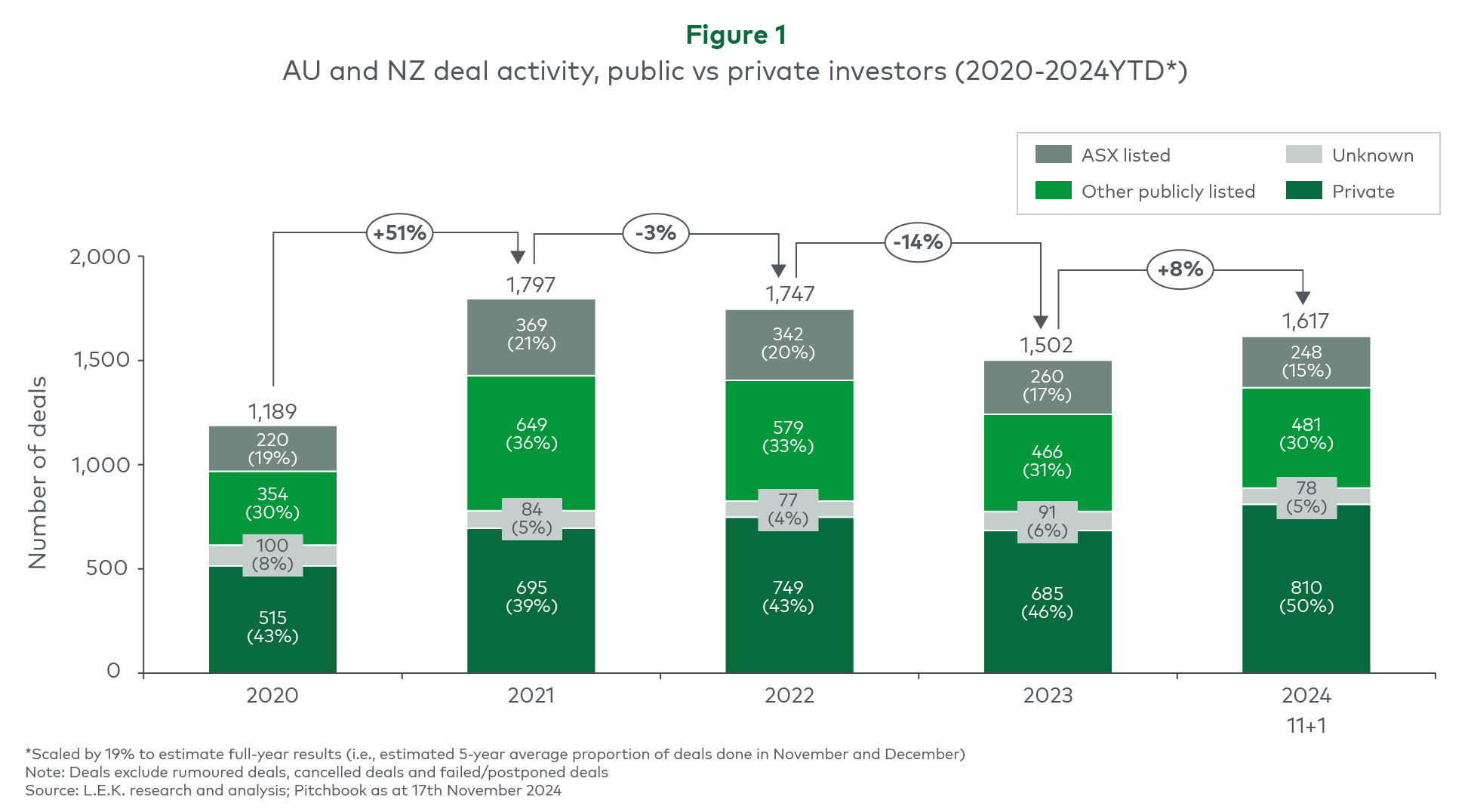

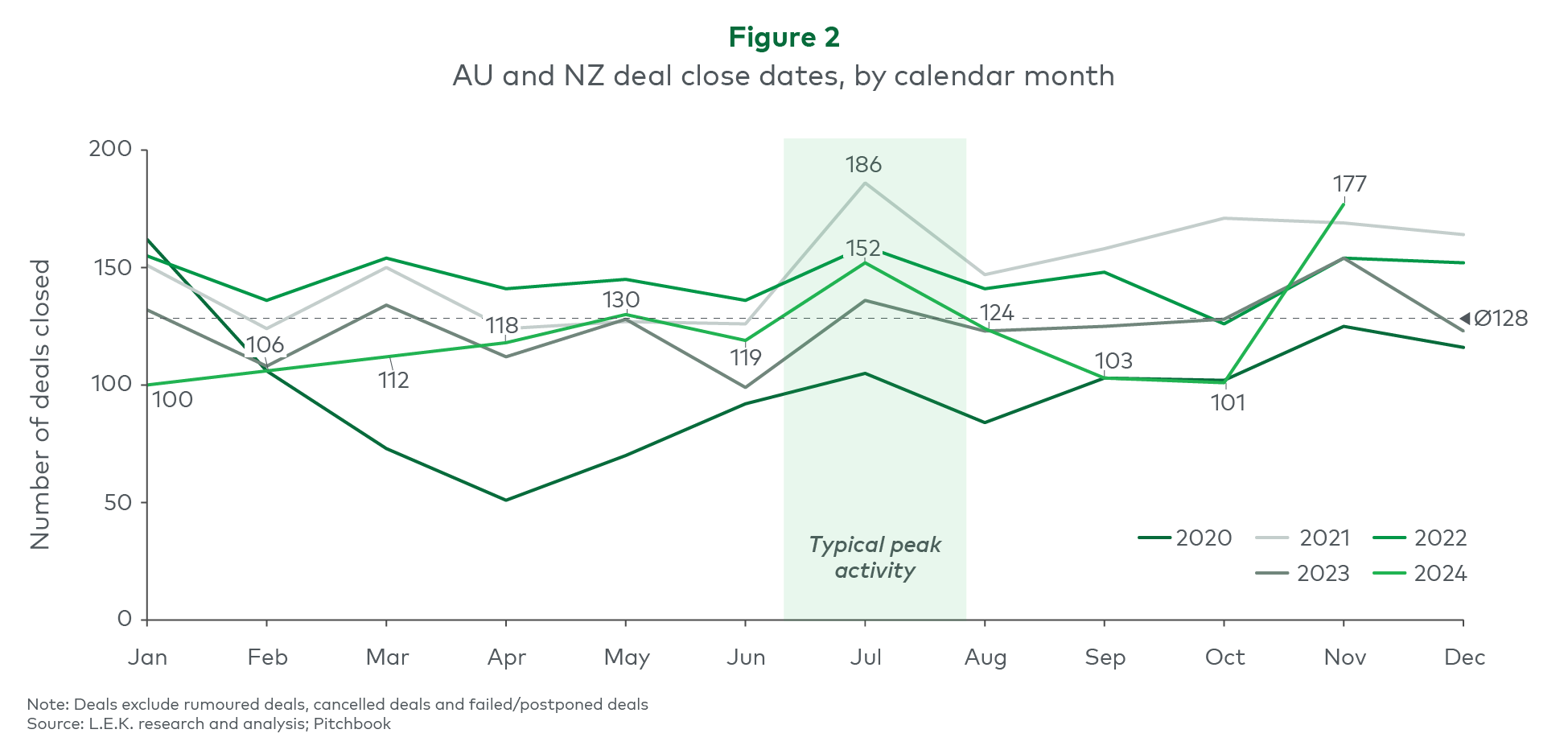

The volume of M&A deal activity in 2024 is likely to be approximately 5-10% higher than in 2023: ANZ deal activity for 2024 remained suppressed after the post-COVID-19 boom years of 2021 and 2022, but it is expected to land slightly above 2023 levels (see Figure 1). There are promising signs of a rebound, as evidenced by the jump in deal activity in Q3-Q4 (see Figure 2):

- In 2024, persistently high interest rates continued to impact financing costs for leveraged buyouts and suppressed appetites for large acquisitions.

- A valuation gap between buyers and sellers persisted, scuppering several marquee transactions in 2024. However, this did not impact all sectors equally. There are signs that this gap is beginning to close and is arguably narrower than that in 2023.

- The increase in activity and rebound during the second half of 2024 can be attributed to easing inflation (e.g., Australian CPI was 2.1% in September compared to 3.8% in June) and a softening labour market, which encouraged consolidation as companies sought to manage costs and remain competitive. November was one of the strongest months since 2021.

- Private capital investors have consistently contributed to a significant volume of deals each year since 2021. In 2023 and 2024, they drove approximately 50% of all transactions, indicating the reliability and resilience of the private capital market in ANZ.

- Could this be a “new normal”? We don’t believe so, as changes in the mix of deal types, industry sectors, and types of investors indicate different expectations and levels of confidence for 2025.

Observation 2

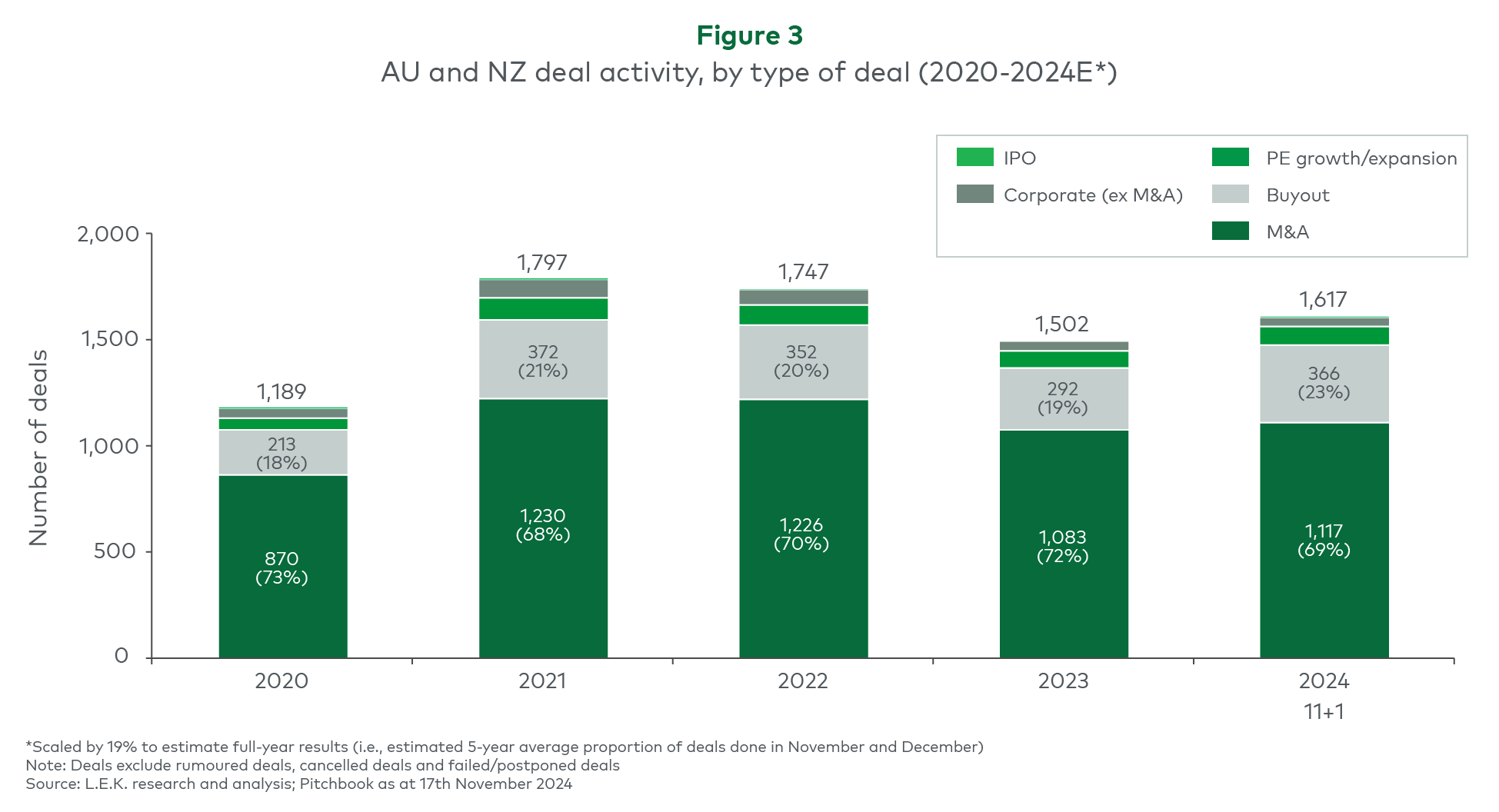

There was an uptick in the number of private equity (PE)-led buyout transactions compared to the previous year (approximately 25% higher than in 2023 and only about 2% less than the watermark year of 2021). Furthermore, buyout deals have been gradually increasing as a proportion of total transactions and now represent 23% of deal volume (or 28% including PE growth/expansion).

On the other hand, corporate-led M&A, which has consistently represented the most volume (approximately 68-72% of total deals over the past five years), was up only 3% in 2023 and decreased as a proportion of the overall volume (see Figure 3).

Observation 3

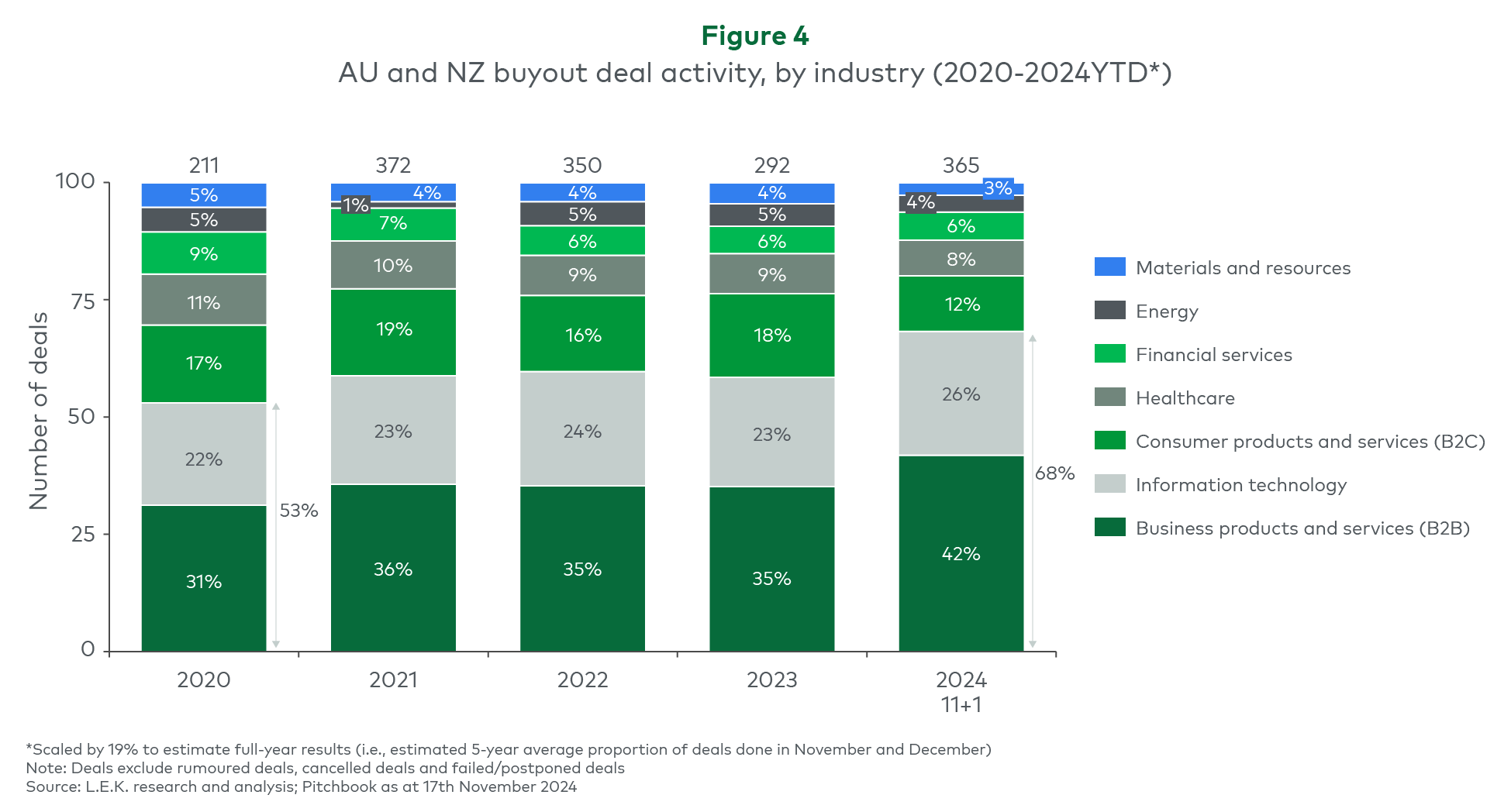

Buyout funds in ANZ continued to concentrate their investments in 2024 around two key industry sectors — business products and services and technology. In 2020, these two sectors accounted for 53% of buyout transactions, and they have been increasing over the past five years to represent approximately 70% in 2024 (see Figure 4).

This trend indicates that buyout funds are strengthening their investment theses around businesses that are resilient to economic downturns, benefit from digitisation, have stable cash flows and offer the potential for consolidation.

PE investors appear increasingly comfortable investing in people-based businesses without obvious competitive moats. These themes have continued to justify successful investments and exits for buyout funds looking at typical three-to-four-year hold periods.

Healthcare and consumer products and services sectors, which have traditionally been a key part of the landscape, saw significantly lower volumes in 2024 (and even lower on a value basis). This partly reflects a lack of assets reaching investable/exit stage, but there have been a number of other contributing factors. For example, in the healthcare sector, ongoing regulatory and funding concerns (private health insurance, NDIS, etc.) have negatively impacted the performance of assets or contributed to uncertainty in the near term. However, there are positive signs for both of these sectors in 2025, and a number of assets are expected to hit the market.

What lies ahead?

We are optimistic about 2025. We expect general uncertainty to continue into Q1 next year as a new administration takes control in the U.S., the Australian elections get underway and mixed economic data continues to impact the interest rate outlook. From Q2 onwards, we anticipate interest rates softening, the ACCC Merger Clearance Reform Bill impacting volumes and asset owners bringing some of the 2024 paused processes back to market, potentially driving volumes above 2023-24 levels.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

02072025130241