Key takeaways

-

L.E.K. conducted a study of more than 100 leading U.K. retailers across 11 different consumer categories to assess the strength of their market positioning, examining the three key dimensions of digital presence, physical presence, and brand and offer.

-

Our analysis explains which retailers have a leading digital presence, why variety retailers score highest on both physical presence and brand and offer, and which individual retailers are best in class.

-

Lessons from the leading brands include: the importance of social media in the digital mix, traffic volume as the foundation of a digital platform, why a right-sized store network is key to balancing cost and convenience, and how range breadth and depth drives customer satisfaction.

The U.K.’s retailers are bearing the full force of the digital storm that is sweeping through the economy. Amid the COVID-19 lockdown, high streets are deserted and shopping has moved almost entirely online for all but essential items. However, with the government now planning for a return to normality, it has never been more important for retailers to ensure that all aspects of their strategy are fit for purpose, and to invest in order to maximise consumer engagement, understand customer needs and wants, and track changing shopping habits.

Retailers striving for success in this environment need to develop a high-performing digital proposition, optimise their physical presence and excel with their brand and offer. Historically, companies could afford to focus on one or two of these dimensions, but now they need to optimise their strategy across all three to win the battle for customers and continue to grow.

But where is investment best made? Who are the market leaders when it comes to digital marketing? What underpins their standout performance? And what are the lessons for companies still wrestling with their strategy in this rapidly evolving sector?

To find out, we conducted a detailed study of more than 100 leading retailers operating across 11 different consumer categories1. For each company, we examined its performance across a number of key dimensions related to market positioning, covering digital presence, physical presence, and brand and offer. In order to develop a view of their relative positions, we ranked each company into deciles across a set of detailed metrics for each dimension.

The results for each company were then aggregated, enabling us to create the L.E.K. Retail Power Index 2020. This Executive Insights details our findings, providing a unique insight into:

- Which retailers have a leading digital presence, and why clothing is the best-performing category

- Why variety retailers score highest on both physical presence and brand and offer dimensions

- Which individual retailers are best in class for each dimension

- The lessons for all retailers looking to create a robust market position

Dimension 1: Digital leaders

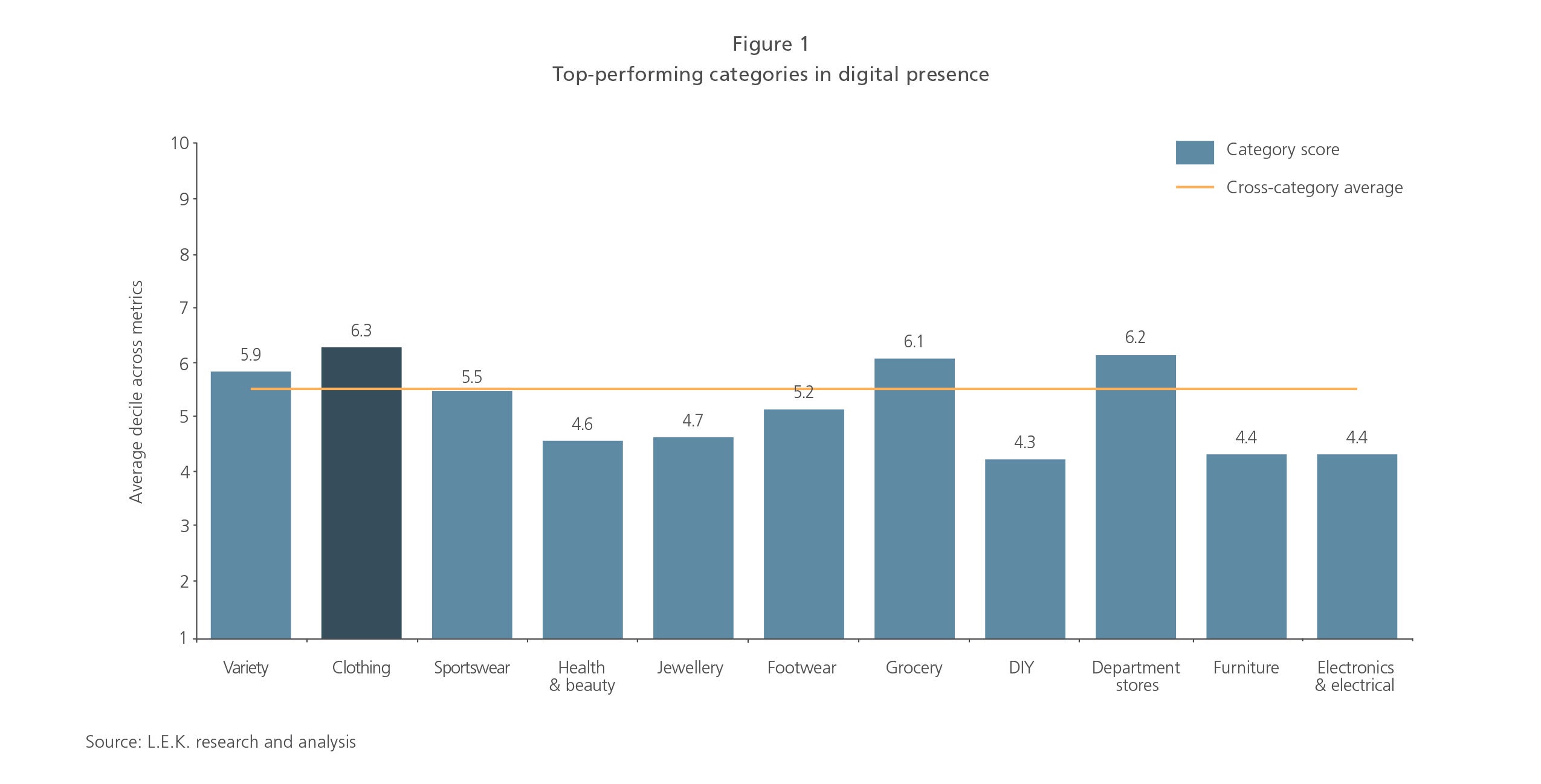

We examined retailers’ digital performance across 11 categories and observed that clothing retailers, on average, performed better than others, with department stores and grocery close behind (see Figure 1).

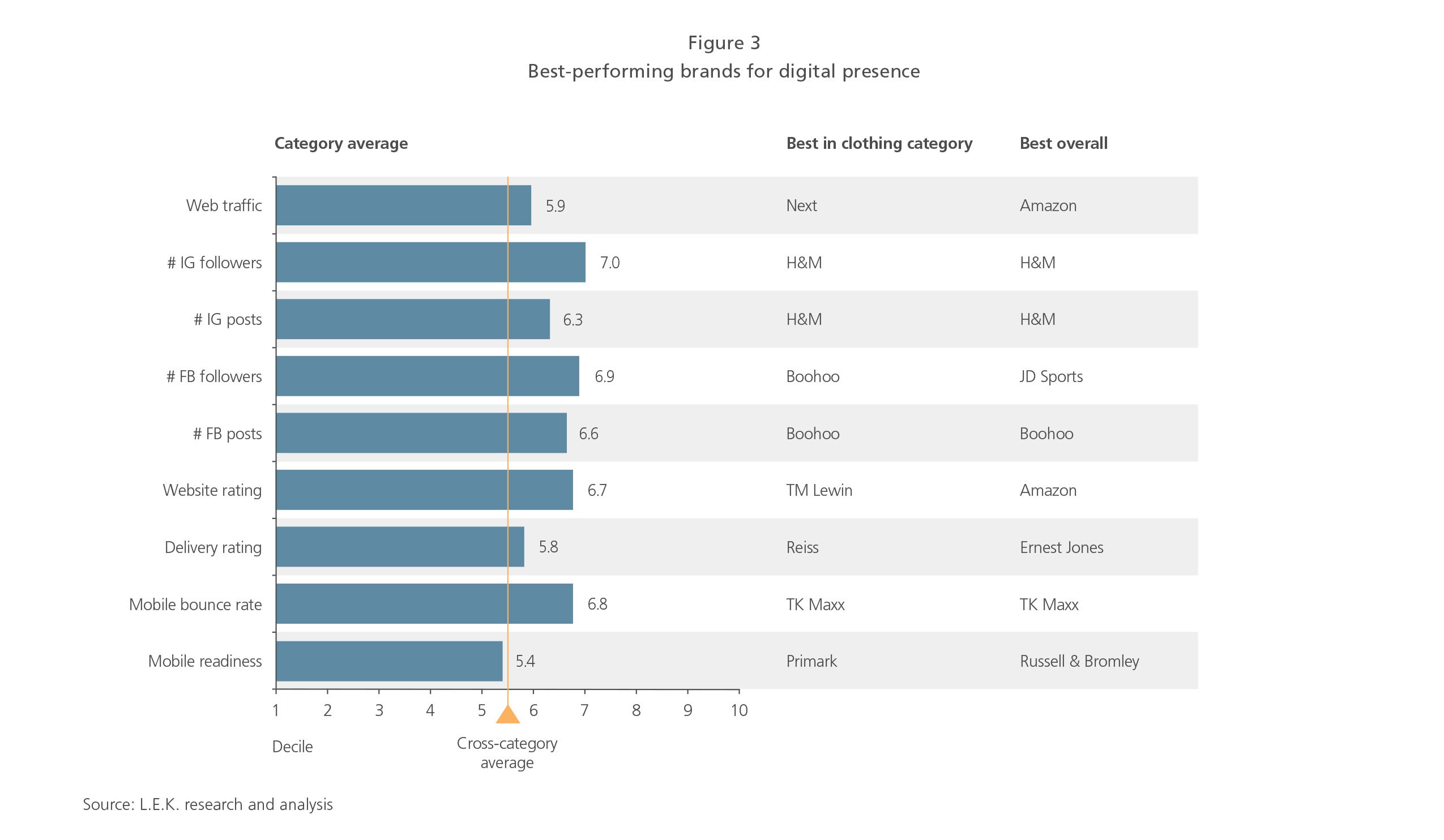

Within clothing, we looked at 34 companies across a variety of digital metrics, including reach, activity, experience and mobile performance. The top performers were value retailers Primark and Boohoo, but no individual retailer stood out on all dimensions, and even the category leaders had specific weaknesses in addition to their clear strengths. We noticed that the top five digital performers are in the top 10% or 20% of companies when it comes to both Instagram and Facebook followers.

Across the digital metrics measured, Boohoo scored highly for its online shopping experience and for a very strong social media presence.

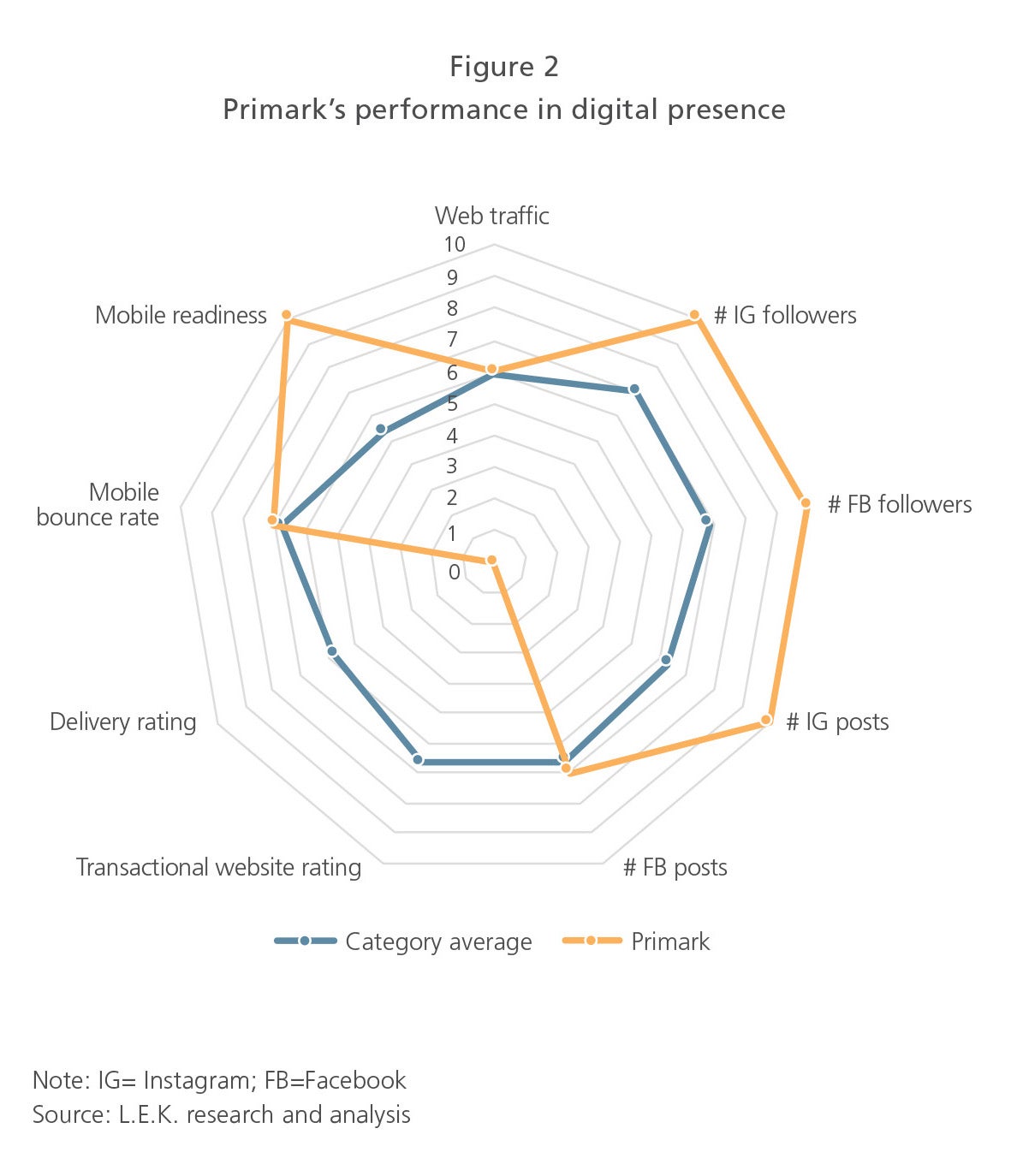

Primark certainly wages strong digital campaigns — which partly explains its superior brand strength (see Figure 2). With more than eight million followers on Instagram and six million on Facebook, the retailer generates significant interest on social media by employing such diverse strategies as using pictures of customers in Brooklyn and collaborations with influencers and reality TV personalities. However, it still lacks a transactional website, which limits its ability to convert all the brand equity directly and measurably into sales.

One example of highly developed digital strategies outside clothing is JD Sports, the leader in the sportswear category and one of the few brands that score highly for digital strength (see Figure 3). In footwear, Size? and Footasylum (both owned by JD Sports) are also scoring high in digital presence. Size? in particular has focused on improving its digital strength through social media activity. In 2018, it posted more than 2,000 times on both Facebook and Instagram — significantly more than the 500 to 1,000 posts produced by competitors.

Dimension 2: Physical presence leaders

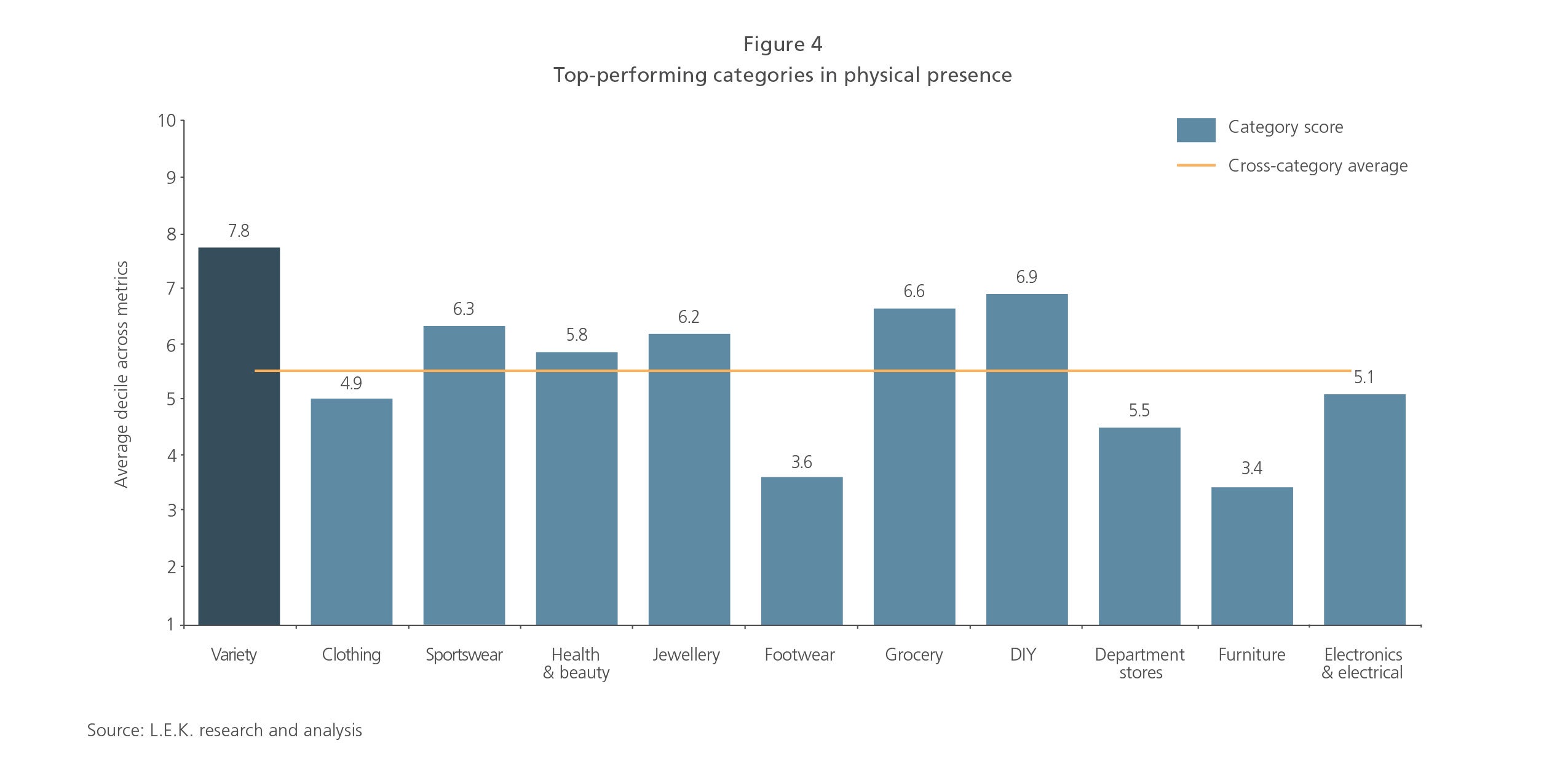

We assessed retailers for the size of their network and the perceived ease of visiting a store. The top-performing category for physical presence was variety retailers (see Figure 4), with B&M the top performer. It opened 39 net new stores in FY 2018 and 44 in FY 2019, and now boasts some 600 retail outlets.

However, the best individual companies with the strongest physical presence come from other categories. Boots and Argos have store networks noted for their convenience, ease of access and ease of collection. Argos’s merger with Sainsbury has yielded a significant increase in presence through implanting Argos stores or collection points in many Sainsbury stores.

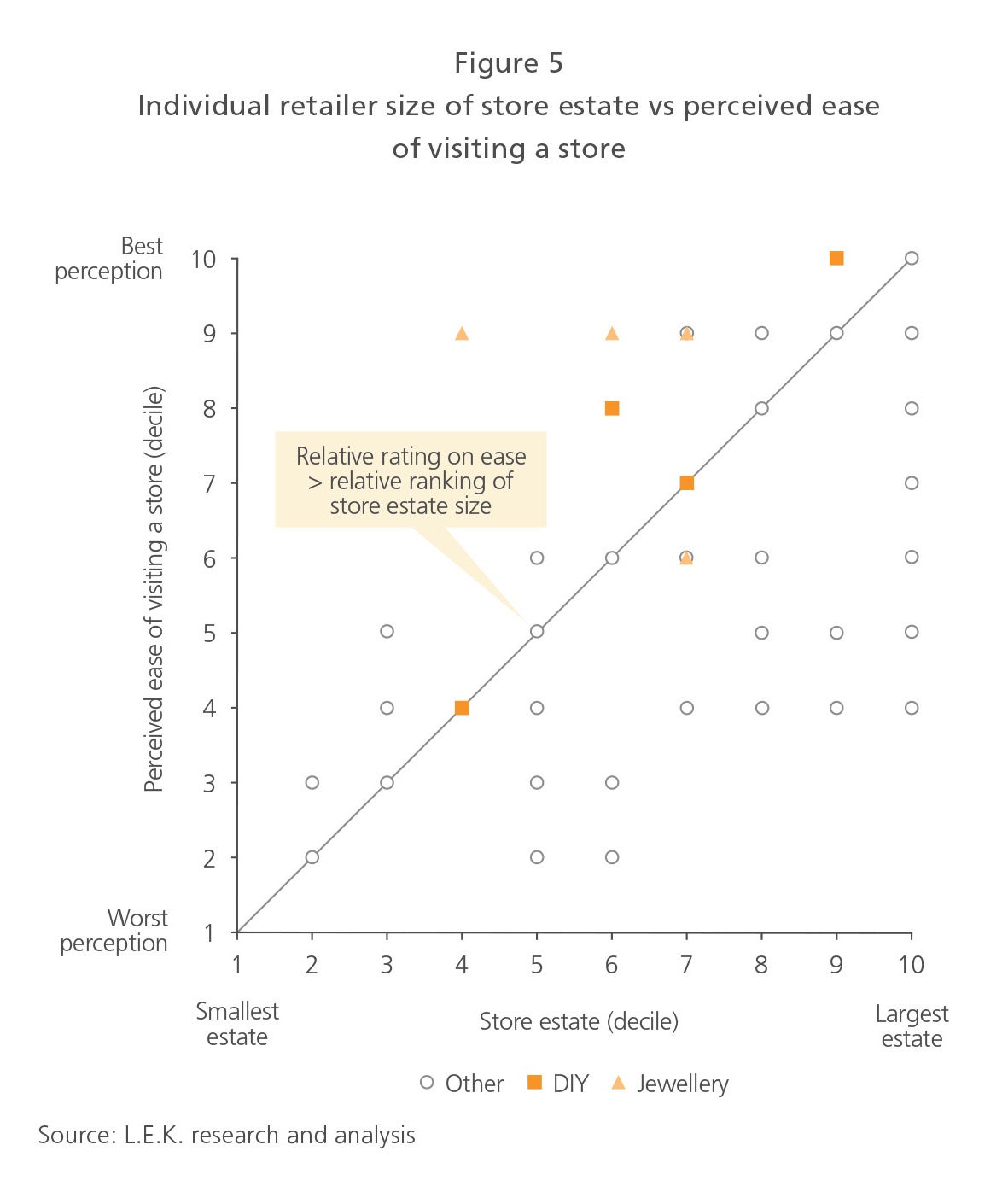

Of course, with the growth of online sales and the recent COVID-19 lockdown, having a large store presence may well prove to be a disadvantage. Given this reality, two categories which attracted our attention because they may be well positioned in terms of physical presence are jewellery and DIY. Retailers from both groups tend to be rated higher on perceived ease of visiting a store relative to the size of their store estate (see Figure 5). Screwfix has recently opened 20 stores, taking its total to around 600, and has developed a convincing click and collect service while achieving industry-leading margins.

Dimension 3: Brand and offer leaders

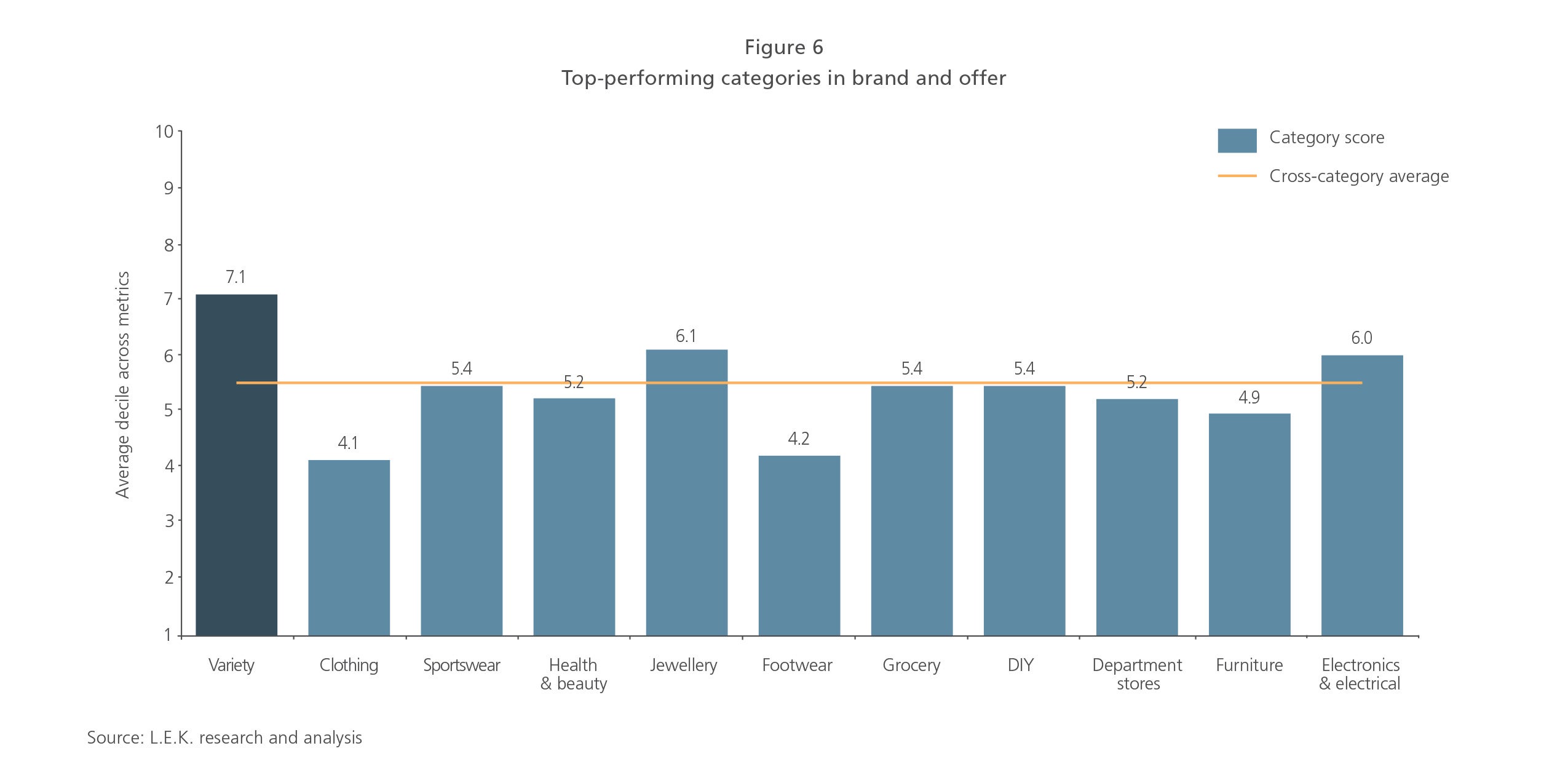

In addition to their leading position in physical presence, variety retailers are also the top-rated category for brand and offer (see Figure 6). We measured the performance of four major companies — B&M, Home Bargains, Poundland and Poundstretcher — for brand awareness, consideration, usage/purchase, advocacy (Net Promoter Score, or NPS), sales promotion effectiveness, advertising effectiveness, breadth and depth of product range, and propensity of customers to make impulse purchases.

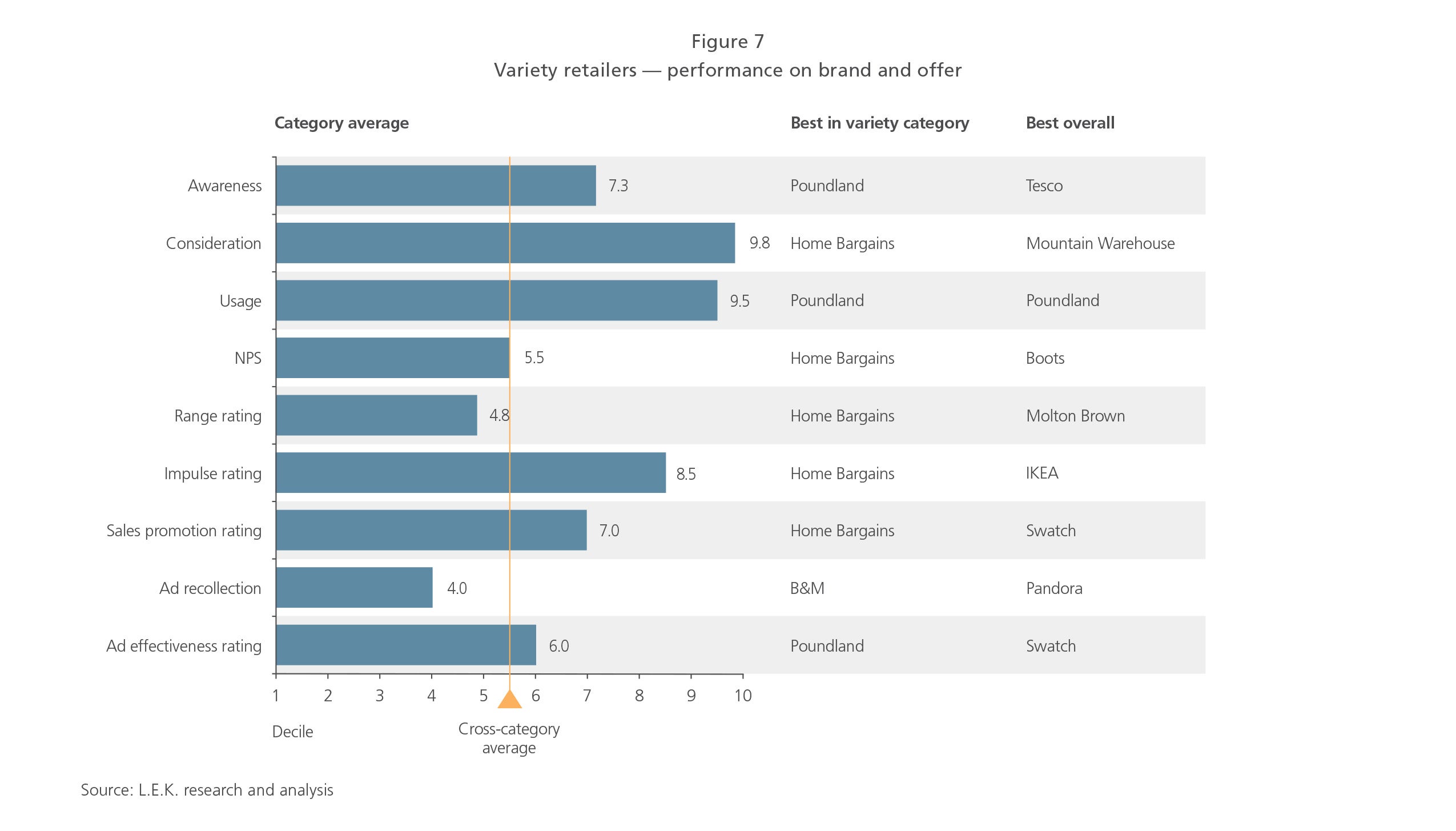

The company that really stands out for the strength of its brand and offer — in this category and for the retail industry as a whole — is Home Bargains, which averaged in the top 30% of companies across our brand and offer assessment criteria. In particular, the retailer scored highly for its wide product offering, the effectiveness of its sales promotions and its success in driving impulse purchases (e.g. through its ‘Star buys’ discount range, which is located at the front of the store and updated weekly).

Outside variety retailers, there are other examples of highly developed brand and offer strategies. For example, Molton Brown achieves high scores on range (see Figure 7).

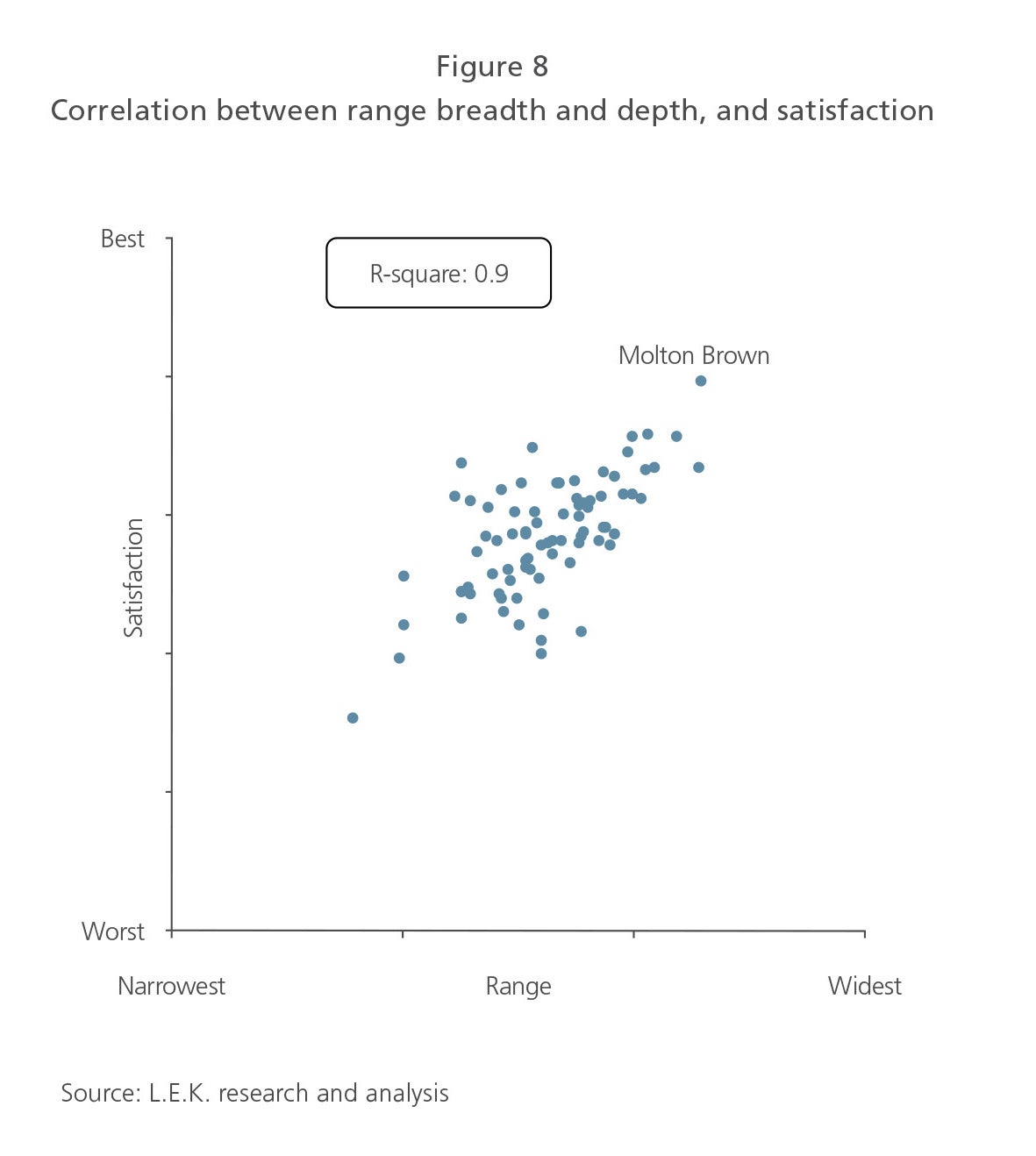

We observed that wider and deeper ranges correlate with higher satisfaction scores across all categories (see Figure 8). Molton Brown is a case in point: it achieves one of the best ratings on range breadth and depth and receives an industry-leading customer satisfaction score.

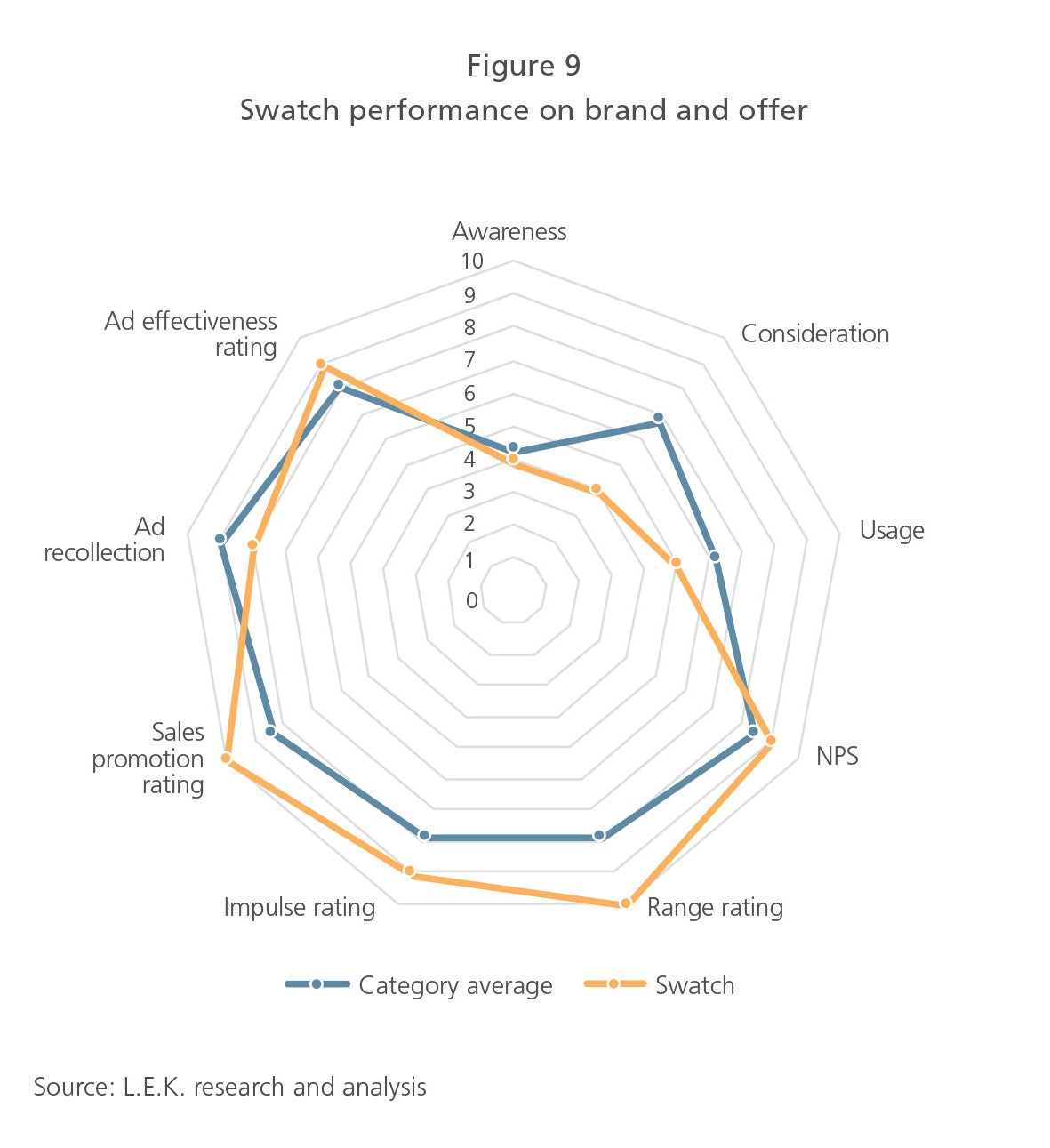

When it comes to sales promotions and ad effectiveness, Swatch runs particularly effective advertising campaigns, with existing customers readily able to recollect the core messages and acting upon advertising campaigns (see Figure 9).

For example, Swatch released a Brexit-themed watch that included a date for when the UK was scheduled to leave the EU and that enabled wearers to choose a specific pattern. This provocative product generated a lot of engagements on social media — the result of careful marketing planning on how to position the brand and get people in the target audience talking about the product.

Lessons from the leading retail brands

The L.E.K. Retail Power Index brings to light some standout companies and categories that can serve as role models for other UK retail brands. From our analysis, we draw out four key characteristics that category leaders exhibit and which differentiate them from their peer group.

1. Social media is key for digital strength

All of the top five digital performers in our survey are in the top 10% or 20% percent of companies when it comes to both Instagram and Facebook followers, which gives them a broader reach than their competitors’. Improving social media presence requires good content generation — top performers also post more frequently on social media than other retailers. Creative content can be pushed to the right customer segments through targeted advertising and the use of social influencers.

2. Driving web traffic volume is the basis for a solid digital platform

The digital leaders tend to have high web traffic, with two of them in the top 10% of retailers. Primark is in the top half of retailers despite not having an online sales platform, which is testament to its strong digital presence. This is typically the result of a higher level of upstream marketing activity, such as paid search. Social media can also be harnessed to drive web traffic.

3. Right-sizing a store estate must optimise the trade-off between cost (store numbers) and perceived convenience

L.E.K. Consulting analysis shows that an estate of 70 stores can reach 90% of the population within a 40-minute drive. Given the current situation, all retailers should examine whether their estate has the right size and format. Store network planning is an increasingly complex and analytical discipline, and for many retailers a large estate negatively affects their economics. Conversely, retailers such as Screwfix demonstrate that it is possible to operate large estates profitably.

4. Range is more important than you think

Range breadth and depth support customer satisfaction. However, range must be expanded with careful consideration to address customer missions and align with store formats while being economically sound. Retailers should also consider infilling their range with impulse products, where clever merchandising can lead to bigger baskets — for instance, a watch retailer adding interchangeable straps or a variety retailer expanding its range of seasonal goods.

In compiling the Retail Power Index, we uncovered a number of best practices and best in class retailers that demonstrate how careful planning and well-thought-out commercial and marketing strategies drive performance. In this most challenging of environments, retail and consumer brands can leverage these lessons to optimise the effectiveness of their commercial operations.

Endnote:

1Research and analysis conducted in November 2019.

09222020120930