Key takeaways

-

An already-booming BPC sector is expected to grow 4.2% per year through 2021, outperforming historical growth since 2011.

-

This rapid growth in the BPC space provides abundant opportunities for chemical companies that can surefootedly navigate this evolving landscape by:

-

Realigning product offerings with the current “it” ingredients and beauty trends

-

Reevaluating go-to-market strategies based on industry shifts and the changing needs of customers

-

-

As part of their go-to-market strategy, chemical companies should focus on “asset-light” brands and contract manufacturers and make technical and sales support a top priority.

A beacon in an otherwise gloomy retail landscape, the booming beauty and personal care (BPC) sector presents big opportunities for U.S. chemical companies and investors that can navigate this rapidly growing and evolving terrain. Today consumers are opening their wallets with far more enthusiasm for beauty products than for shoes and apparel. And in direct contrast to other retail sectors, we expect the BPC sector to grow 4.2% per year through 2021, outperforming historical growth of 3.4% per year since 20111 — opening a window rich with possibilities.

How can U.S. chemical companies successfully capitalize on this underlying sector growth? The answer is twofold. First, companies must align their product offerings with current beauty trends by focusing on the latest “it” ingredients. And next, companies must approach their go-to-market strategies from a fresh angle now that the “what” and “how” to sell are undergoing swift transformations.

The following analysis is part of our ongoing Executive Insights series on emerging trends and growth opportunities for U.S. chemical companies.

Profiting from three key ingredients

Today’s BPC consumers are a new breed: They are plugged-in, informed and savvy, thirsty for proven, good-for-you, one-of-a-kind products — whether it’s a moisturizing serum that has been promoted on Instagram by a celebrity or an organic body scrub in Sephora. And they are driving demand for BPC product formulators to create the “next great thing” — like erasing wrinkles overnight or eradicating acne for good — using specialty ingredients.

This places U.S. chemical manufacturers at a crossroads, where the winners will find ways to profit from the radically shifting consumer and end-customer preferences by expanding their ingredient offerings in tandem with beauty trends. With that in mind, we see the following product attributes having the biggest impact on commercial success in the specialty BPC chemical market going forward:

Functional. Companies are on the endless quest for the next greatest active ingredient to meet consumers’ need for products that are proven to work — not ones that might work. There is also high demand for specialty ingredients (e.g., jojoba) for specific functional properties. Cutting-edge beauty trends from Asia are also creating a demand for specialty ingredients, driving U.S. market expansion with new products, such as beauty balm (BB), color correcting (CC) and “dynamic do-all” (DD) creams, and creating a need for uncommon active ingredients like snail slime (see Figure 1).

Natural. Consumers are becoming increasingly aware that what goes into their beauty products goes beyond skin-deep. To keep consumers happy, manufacturers are eschewing artificial elements, such as dyes and synthetic-based silicon, in favor of naturally sourced products — which are typically higher value than synthetic materials. In fact, the shift from synthetic to natural and specialty natural ingredients is the main growth driver in the personal care market.

Personalized. A bigger dilemma for the consumer is often what a product will do for her specific issue — and the store and online shelves are chock-full of answers. Products are increasingly serving precise purposes for addressing specific skin types (e.g., oily, sensitive), requiring more innovative specialty chemicals to provide these tailored benefits.

Consumers, BPC companies and product formulators alike have reaped the benefits of the specialized ingredient trend — whether through healthier skin, a growing customer base or increased profits.

U.S. chemical companies can benefit as well through higher profit margins, a smaller competitive playing field, potentially proprietary formulas and increasingly important ingredients.

First, specialty actives and additives boast higher profit margins, typically exceeding 50%, compared with 20% to 50% on nonspecialty ingredients. Furthermore, the competitive playing field is noticeably smaller; typically, only one or two suppliers produce a specific specialty ingredient.

Another benefit is the complexity of product formulations. Specialty ingredient formulas are not easily duplicated and are potentially proprietary, unlike commodity ingredients that can be easily copied and sourced. Entering the specialty ingredient market also opens the door to an array of increasingly important ingredients — some of which are new or unique and could play an important role in the next best anti-wrinkle cream or hairsmoothing product.

Two formulas for successfully going to market

Now that we’ve determined “what” to sell, “how” do U.S. chemical companies sell it? Those that succeed will examine their go-to-market strategy through a different lens — inclusive of a value-added approach shaped by industry shifts and tailored to the changing needs of customers.

1. Focus on emerging brands and contract manufacturers

Emerging niche brands (or “asset-light” brands, which don’t have their own manufacturing assets) and contract manufacturers are vital not only to each other’s success but to the specialty beauty and personal care supply chain as a whole. U.S. chemical companies must foster collaborative relationships with these groups or risk losing out on abundant opportunities where timing is critical.

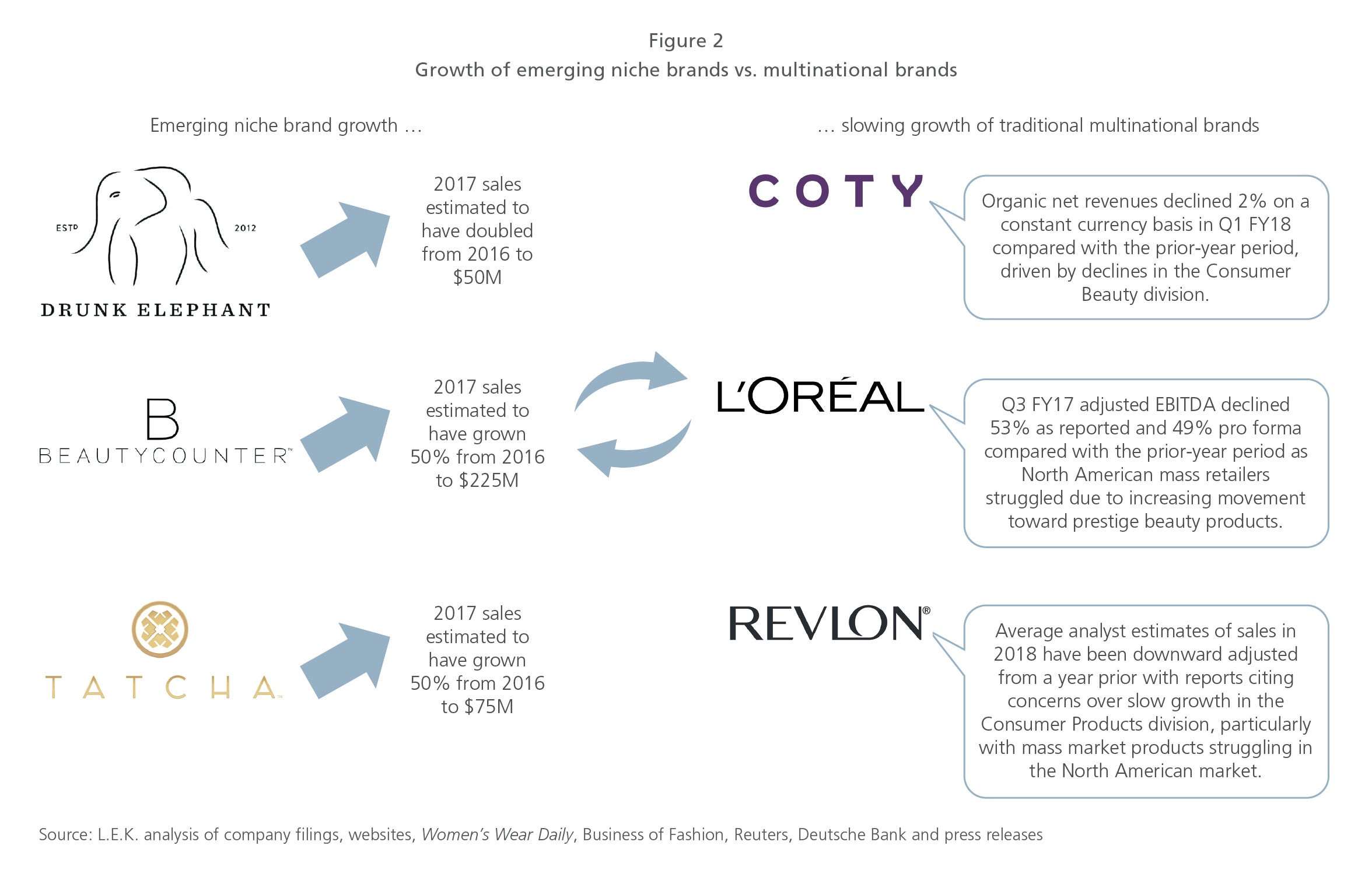

One trend underscores the importance of this point: Stalwart multinational brands such as L’Oréal and Estée Lauder are being pushed aside by small BPC players such as Drunk Elephant and Tatcha (see Figure 2). These brands and those like them, while not yet household names, are expected to continue poaching market share from the legacy brands because they excel at things those companies do not. For example, they’re adept at navigating key marketing platforms, particularly social media, and they foster personal relationships with consumers by quickly launching products that align not only with market trends but with their customers’ tastes, and by presenting unique brand stories that resonate with the individual.

In turn, contract manufacturers are producing these asset-light brands’ products by using each brand’s proprietary formulas and specific ingredients; some contract manufacturers even go a step further by providing product development support if needed.

And there’s more. Multinational brands also work with contract manufacturers to increase speed to market, and retailers like Sephora collaborate with them on private-label lines, underscoring the importance of U.S. chemical companies’ increasing need to focus on the contract manufacturing market segment.

2. Make technical and sales support a priority

Gone are the days when U.S. chemical companies could compete by playing one role — that of the supplier. Many U.S. chemical companies are not structured to deliver technical assistance and consistent in-person sales support to customers because, quite simply, the distribution of more basic ingredients has not merited high-touch support in the past.

With asset-light brands and contract manufacturers now encroaching on legacy-brand market share, however, U.S. chemical companies must be a partner — providing perhaps more intangible but no less important services like technical expertise and R&D assistance to their customers.

How can chemical companies go about doing this? For the burgeoning asset-light BPC brand market, for example, this means that chemical companies — and/or their distributors — need to make technical assistance a seamless component of product formulation services, thereby saving BPC companies time and resources.

Multinational companies have also been affected by the ever-changing consumer and end-customer preferences and the subsequent shift in ingredient offerings. Strategically sending sales support to areas that are not necessarily within the purview of the purchasing department, like R&D and marketing, ensures that market trends become a regular part of the conversation and drive decision-making.

A potential payoff for chemical companies

Big things are happening in the beauty and personal care sector, and the outlook through 2021 is especially bright. U.S. chemical companies are in an opportune position to reassess existing specialty ingredient product offerings, homing in on functional, natural and personalized ingredients, as well as go-to-market strategies that highlight collaboration and value-added services, with an eye toward capitalizing on an exciting period of growth. As the underlying growth sector trends upward, those companies that can sure-footedly traverse this rapidly changing landscape will win versus the competition.

1Euromonitor, DSA, Quartz, L.E.K. analysis

01052021090111