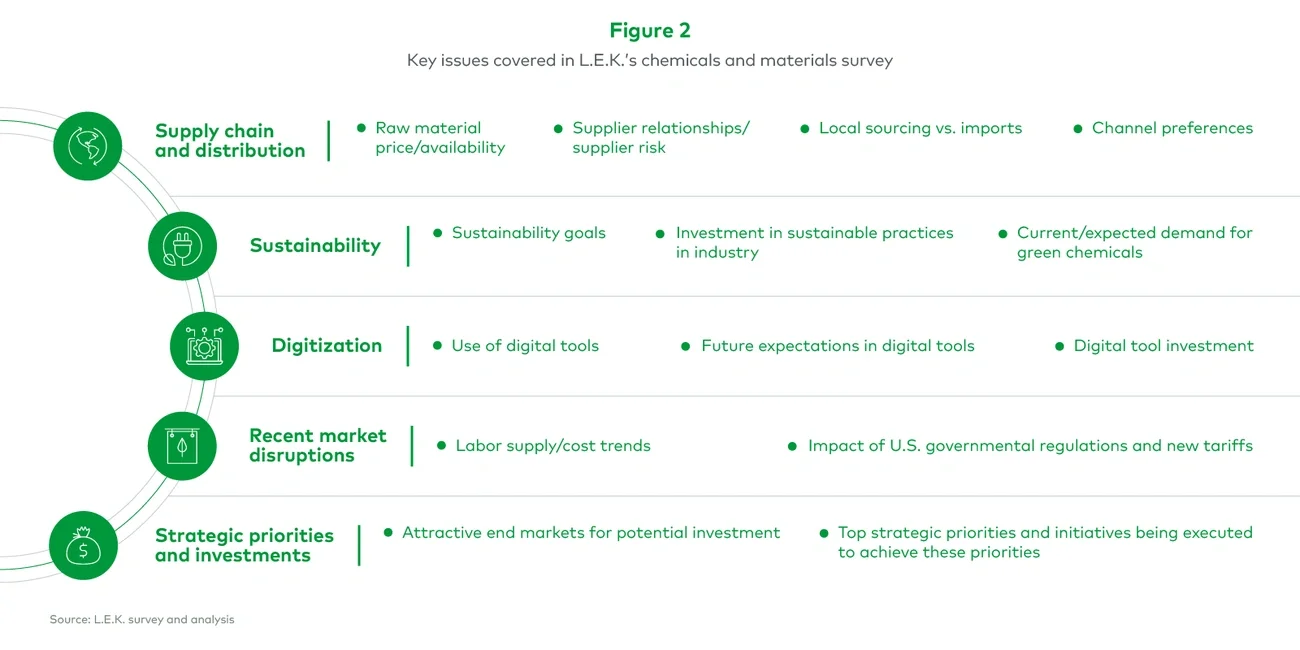

After consistent expansion over the past several decades, the specialty chemicals industry now faces a transformational future. Enduring trends such as development of petrochemical feedstocks and heavy investment in fossil-fuel supply chains are giving way to innovation and significant investment in the development of specialty chemicals to address key megatrends facing the industry around sustainability, industrialization and resource scarcity.

A broad set of companies and investors — from major, diversified strategic chemicals firms to startups and academic research institutions — have seen and seized opportunities to innovate and capture growth in order to address critical needs tied to these megatrends. However, challenges persist around cost, feasibility, supply chain and commercial constraints. For example, numerous attempts at developing bio-based chemicals to address sustainability needs have historically seen mixed performance due to limited willingness to pay from end markets and complexities producing product at scale. Meanwhile, labor shortages, feedstock availability, price volatility, tightening regulatory oversight and numerous other operating challenges are adding complexity to supply chains.

Today, chemicals firms are looking to invest in several areas to overcome some of these barriers, including new digital ways of working, new technologies to support sustainability goals and optimization of the supply chain. The importance of evolving priorities within the industry is greater than ever for companies looking toward the future — customers are increasingly demanding green solutions, reduced emissions and ways to differentiate products, and these demands will be shaping the market for many years to come.

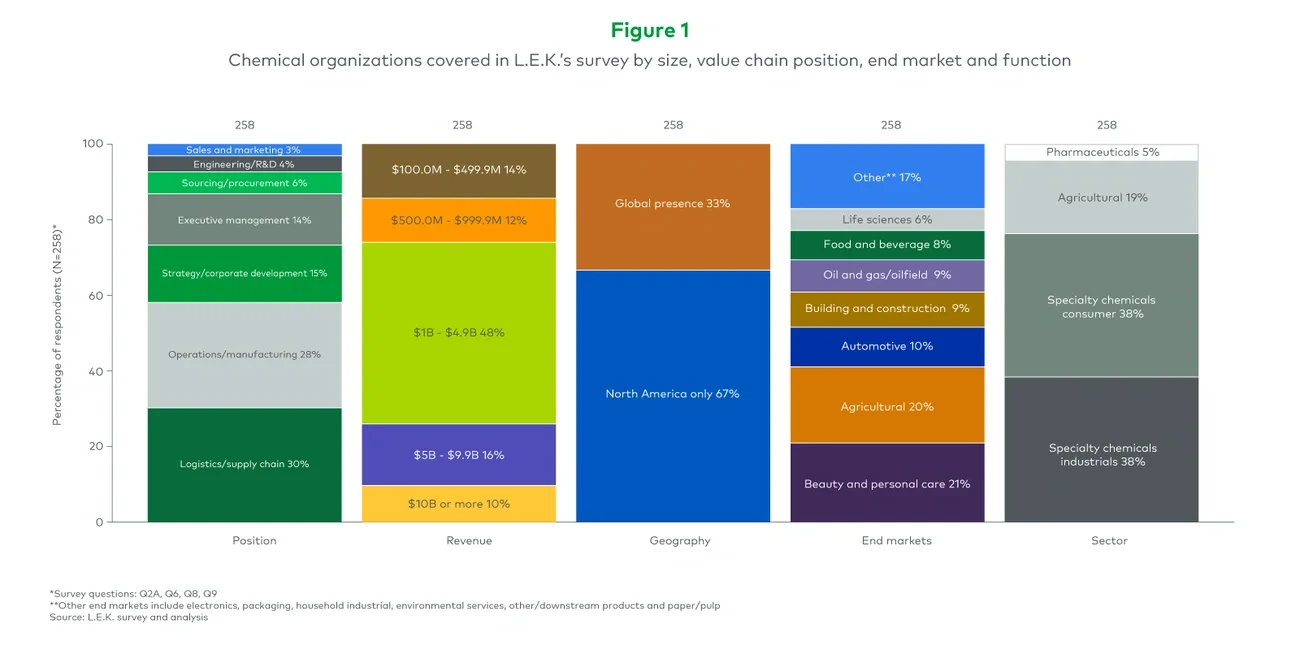

To capture a comprehensive picture of where specialty chemical growth strategies are headed, L.E.K. Consulting conducted our annual proprietary industry survey in July 2023. About 260 respondents from global and North American companies represent a cross-section of specialty chemicals organizations by revenue size, end market application and value chain position. Respondents include logistics/supply chain, operations and manufacturing, strategy and corporate development, and executive management perspectives. A multitude of specialty chemicals end markets were covered, including automotive, personal care, agriculture, building and construction, food and beverage, and oil and gas (see Figure 1).