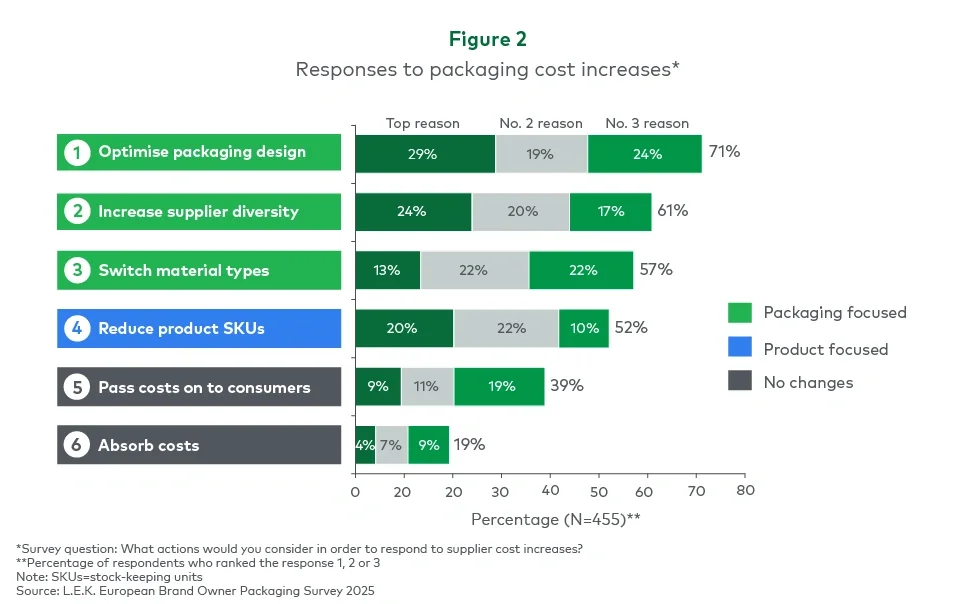

This year, packaging costs have become a dominant issue for brand owners across Europe. With inflationary pressures lingering and supply chain disruptions still rippling through global markets, the majority of companies now see rising packaging costs not as a blip but as a structural reality. The result is a shift in how companies are managing both day-to-day procurement and long-term packaging strategy.

To understand how brand owners are responding, L.E.K. Consulting conducted its fourth annual European Brand Owner Packaging Survey in December 2024 and January 2025. This year’s study includes responses from 645 brand owners across six major markets — Germany, France, the UK, Spain, Italy and Poland — spanning a diverse range of sectors from food and beverage to healthcare, beauty and consumer electronics.

This article, the first in a series, explores the cost trends shaping packaging decisions in 2025. Subsequent pieces will examine how brand owners are rethinking investment, sustainability and innovation in response to these pressures.

The cost outlook: Sharp increases ahead

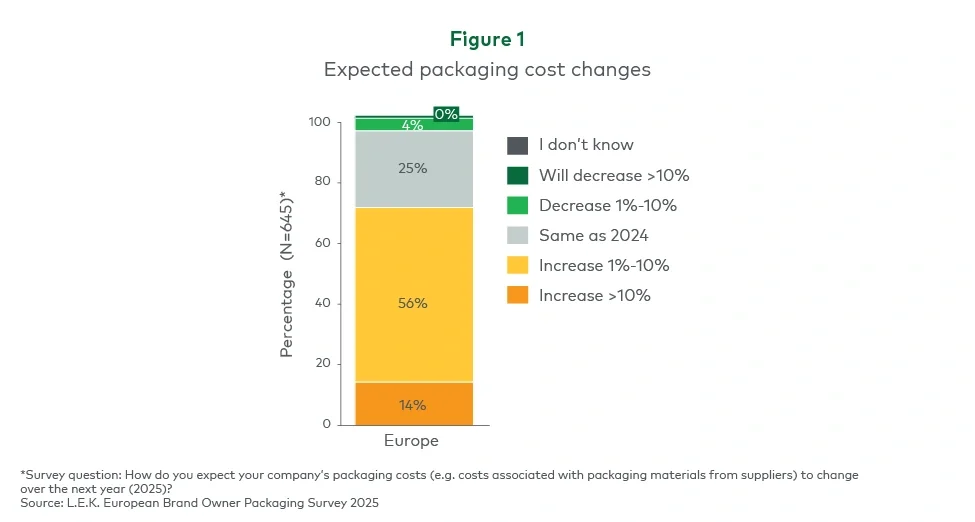

It’s little wonder that cost now sits at the top of the agenda for European packaging executives. More than 70% of European brand owners expect packaging costs to increase over the coming year. A full 56% anticipate rises in the range of 1%-10%, and a further 14% expect increases to exceed 10% — figures that underscore the intensity of cost pressures facing the market (see Figure 1).