This is the second in a series of articles that analyze why the packaging distribution industry is an attractive choice for M&A exploration.

As buyers approach potential acquisition moves in the packaging distribution industry, there are three key value creation levers to consider as factors in the decision: upstream value chain extension, equipment offering expansion and product mix diversification. Each can be enabled by M&A geographic footprint infill.

Upstream value chain extension

Potential buyers can focus their acquisition strategy on expanding their upstream value chain services to strengthen customer stickiness and realize margin uplift. This has been a theme especially in market segments where we see high-value packaging, such as beauty and high-end spirits.

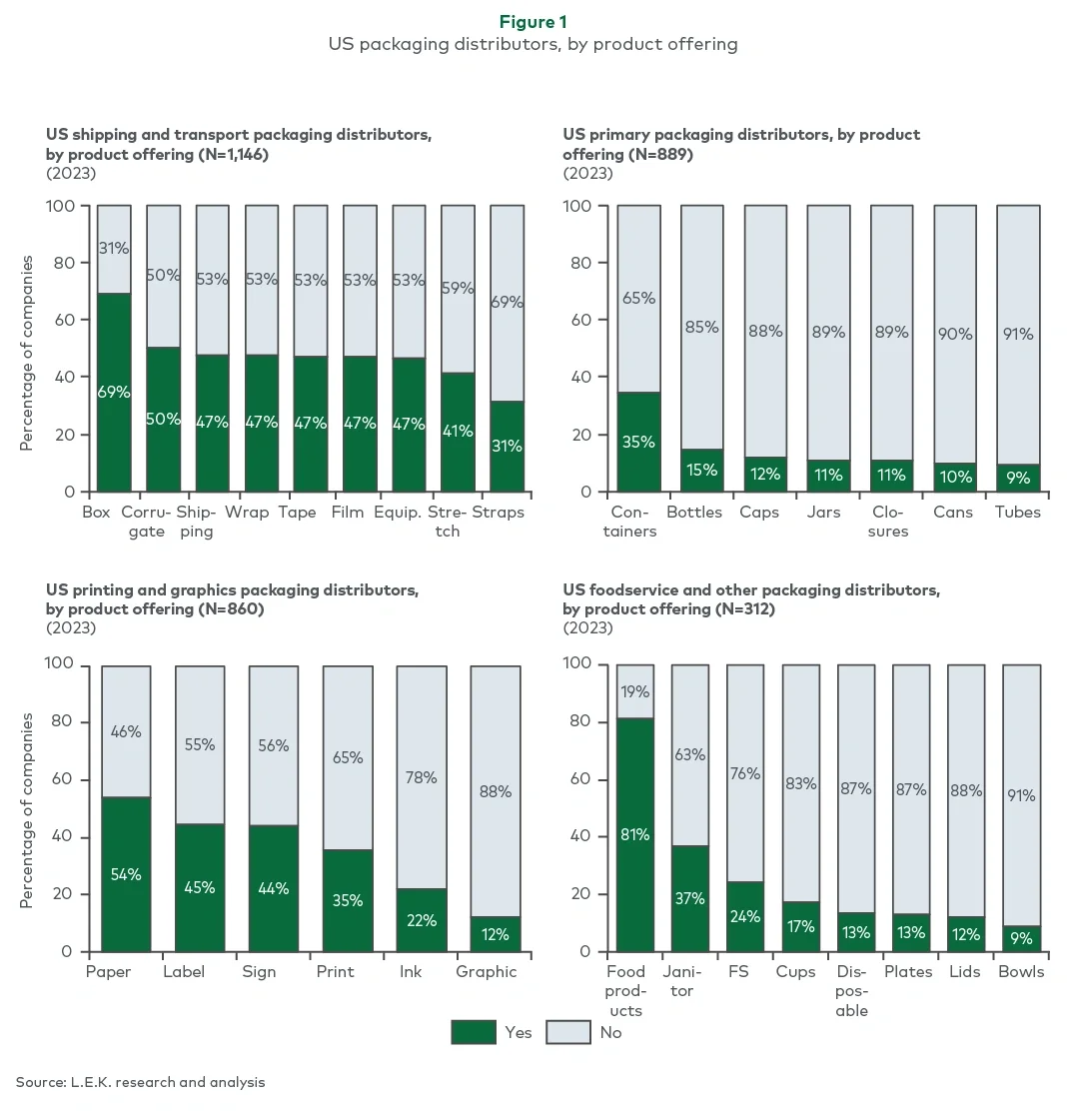

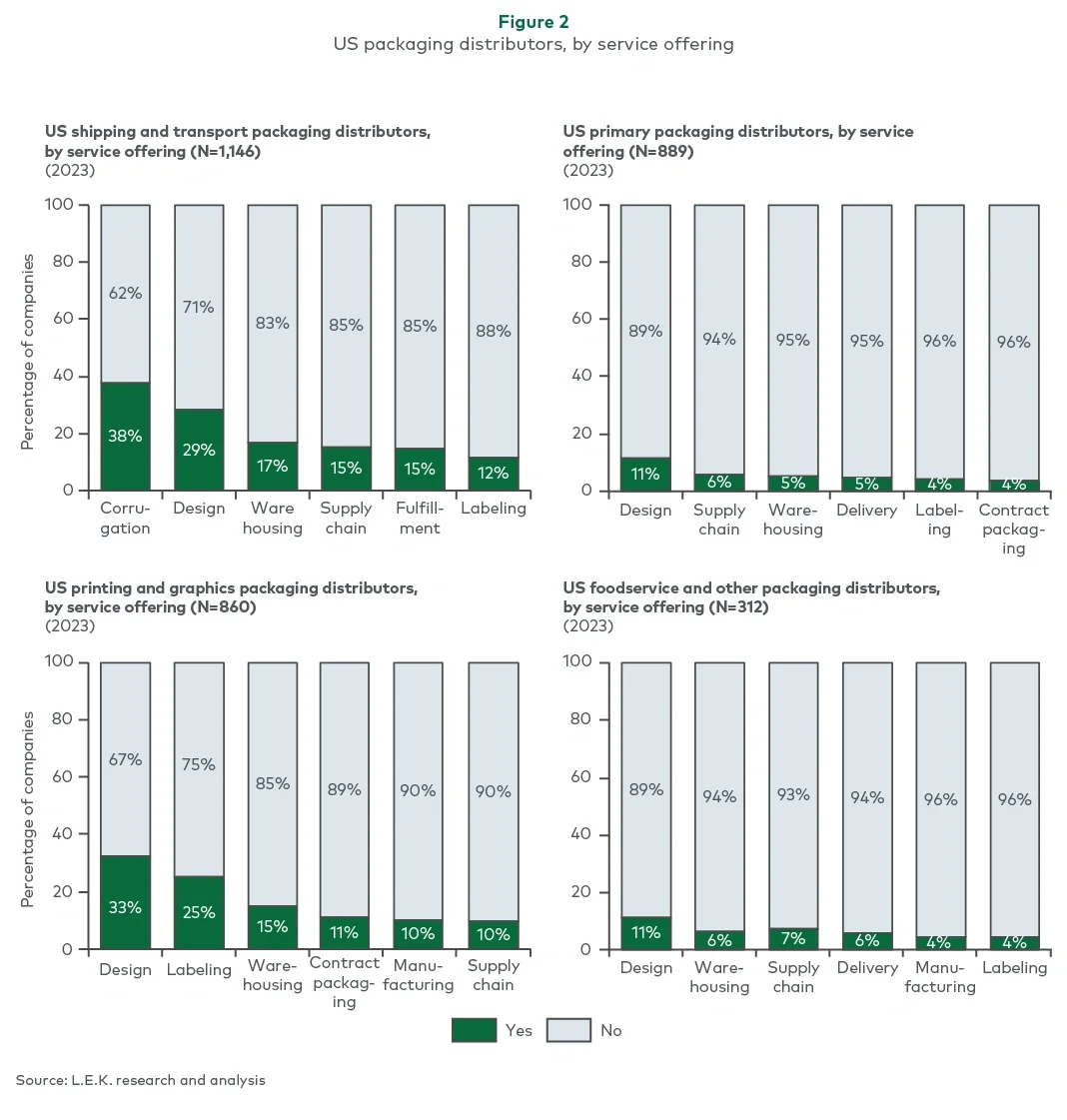

Examples of add-on, upstream capabilities include design, engineering, materials science and contract packaging capabilities. About 25% of the estimated 3,200 U.S. packaging distributors offer design services, and around 10% offer engineering and/or contract manufacturing services (each of which is usually accretive to typical distribution margins); this indicates an ongoing opportunity to acquire specific upstream capabilities.

Equipment offering expansion

Another area of potential value is equipment offerings, which can drive long-term consumable sales and support aftermarket parts and service offerings. Distributors that offer equipment are typically above $5 million in annual revenue. This indicates a need for higher levels of investment than what is required to distribute packaging products and indicates moderately more consolidation than other segments in packaging distribution.

An estimated 47% of about 1,150 shipping and transport packaging distributors (one of four major archetypes in distribution, see Figure 1) offer equipment as a product, implying runway for equipment product and aftermarket service-offering expansion. By offering equipment, distributors have an opportunity to grow share of wallet with current customers; generate stable, recurring revenue via consumable sales; and expand their customer bases, providing future product cross-sell opportunities. Critical to success in serving the equipment aftermarket is having a network of maintenance engineers trained on original equipment manufacturer (OEM)-branded equipment, who can perform aftermarket services that may otherwise have been handled in-house by the OEM operator or the equipment OEM.