This is the first in a series of articles that will look at the current landscape of packaging distribution and how to best create value in the market, drive differentiation and examine roll-up acquisitions opportunities.

One of the next frontiers of consolidation in the U.S. packaging market is the distribution landscape, which features 3,200 participants and represents a smart choice for M&A exploration. Five key themes underpin the attractiveness of the market as an investment opportunity, specifically:

-

End market and customer diversification: Packaging distributors typically serve a fragmented base of customers that often participate across end markets, which limits customer-specific risk, end-market concentration risk and threats from market cycles.

-

Positive channel shifts: Goods manufacturers (e.g., primary packaging converters, securement packaging manufacturers, print equipment original equipment manufacturers (OEMs) and paper producers, foodservice disposables manufacturers) increasingly rely on distribution as an alternative channel versus serving customers directly, particularly small to medium-sized customers.

-

Overexposure to high-growth customers: The distribution channel over-indexes to small and midsize customers. These customer segments are typically higher growth than enterprise customers and demonstrate greater willingness to pay than enterprise customers for value-add services (e.g., packaging design), given lower levels of in-house capabilities, creating opportunities to wrap incremental services around core product distribution.

-

Multiple means of unlocking value: There are a variety of value creation levers when consolidating packaging distributors, including executing effective post-merger integration, driving improvements in sales force effectiveness, leveraging digital tools to better reach and serve end customers, and expanding into additional product categories (e.g., JanSan).

-

Attractive market structure: The fragmentation of the distribution landscape presents a range of potential M&A opportunities from platform investments to targeted, end market-specific candidates and roll-up strategies.

The first article in this series explores the structure and relative fragmentation of the packaging distribution landscape.

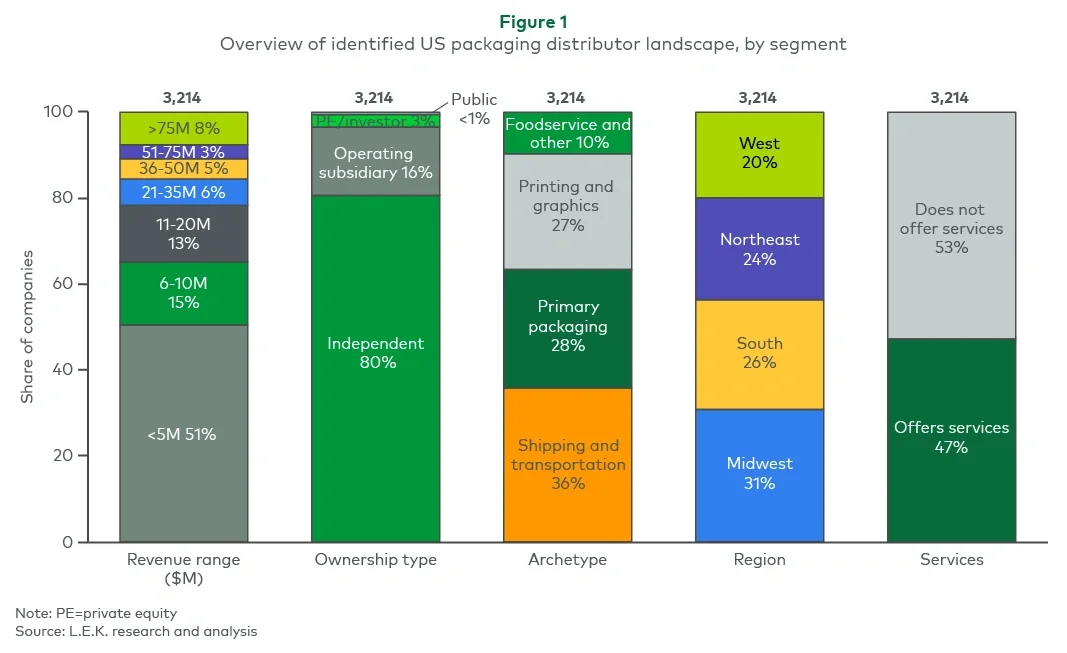

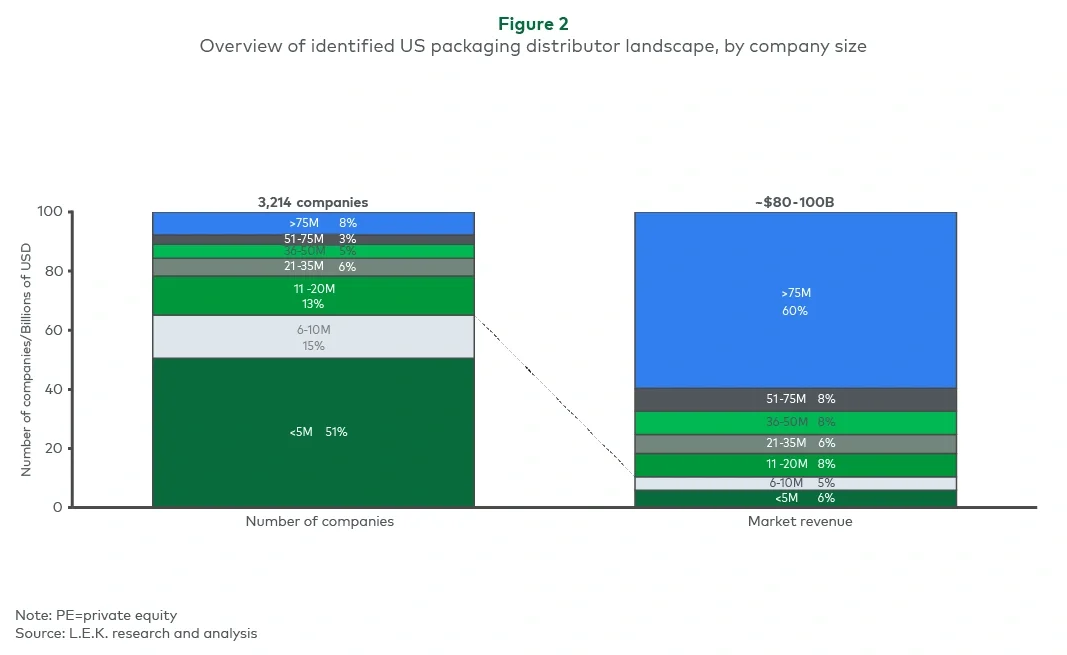

The packaging distributor market today is highly fragmented, consisting primarily of independently owned businesses, despite modest ongoing consolidation efforts by a subset of market participants (see Figure 1). The market includes over 250 potential “platform” targets (i.e., businesses with $75 million plus in revenue representing about 60% of addressable market value) and an attractive landscape of potential “add-on” targets. This add-on landscape includes over 850 distributors with revenue of $10 million-$75 million representing roughly 30% of addressable market value.

In terms of products and services, companies are well distributed across archetypes:

- Shipping and transportation (e.g., boxes, tape, wrap) — 36%

- Primary packaging (e.g., containers, bottles, tubes) — 28%

- Printing and graphics (e.g., labels, signage, ink) — 27%

- Foodservice and other (e.g., cups, disposables, janitorial) — 10%

The largest archetype in terms of number of companies, shipping and transport, has seen considerable demand growth driven by ecommerce.