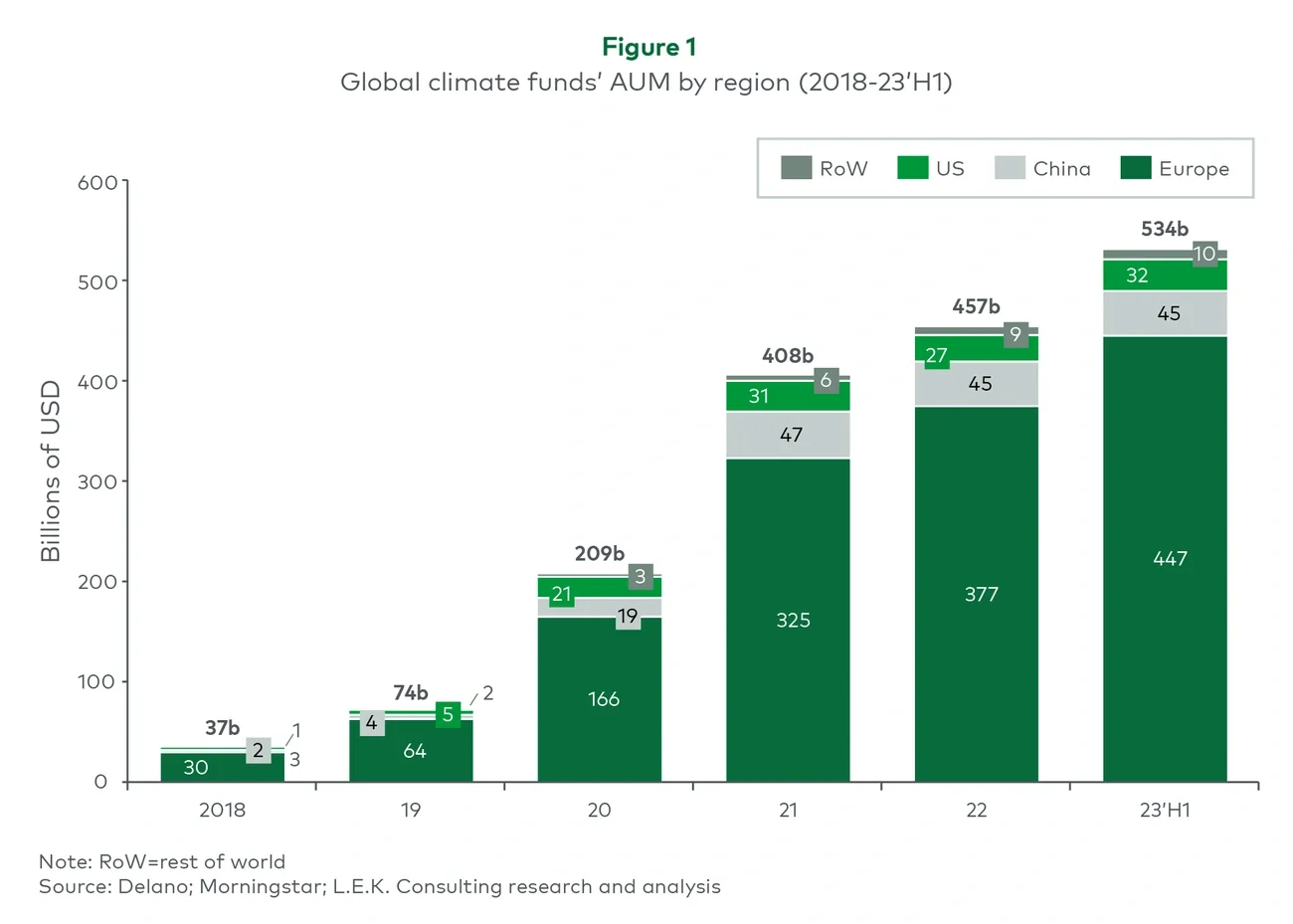

In recent years, there has been a substantial surge in global investments in climate solutions, driven primarily by Europe. According to recent analyses, Europe accounted for approximately 84% of climate assets under management (AUM) in the first half of 2023. Europe, the United States and China collectively represent nearly 98% of total climate investment. Since 2018, global climate funds’ AUM have grown at a CAGR of c.71%. This exponential growth in climate finance, particularly since the COVID-19 pandemic, underscores the increasing prioritisation of sustainable and green investments on a global scale (see Figure 1).

A Surge in Private Equity Investments in Sustainability Assets

A Surge in Private Equity Investments in Sustainability Assets

October 31, 2024

Image

Over the past decade, several major global private equity (PE) firms have established dedicated climate funds, and several have launched second or third round impact funds. KKR, TPG, Bain Capital, General Atlantic and Brookfield have all closed funds within the past three years with values ranging from $0.8 billion-$10 billion USD.

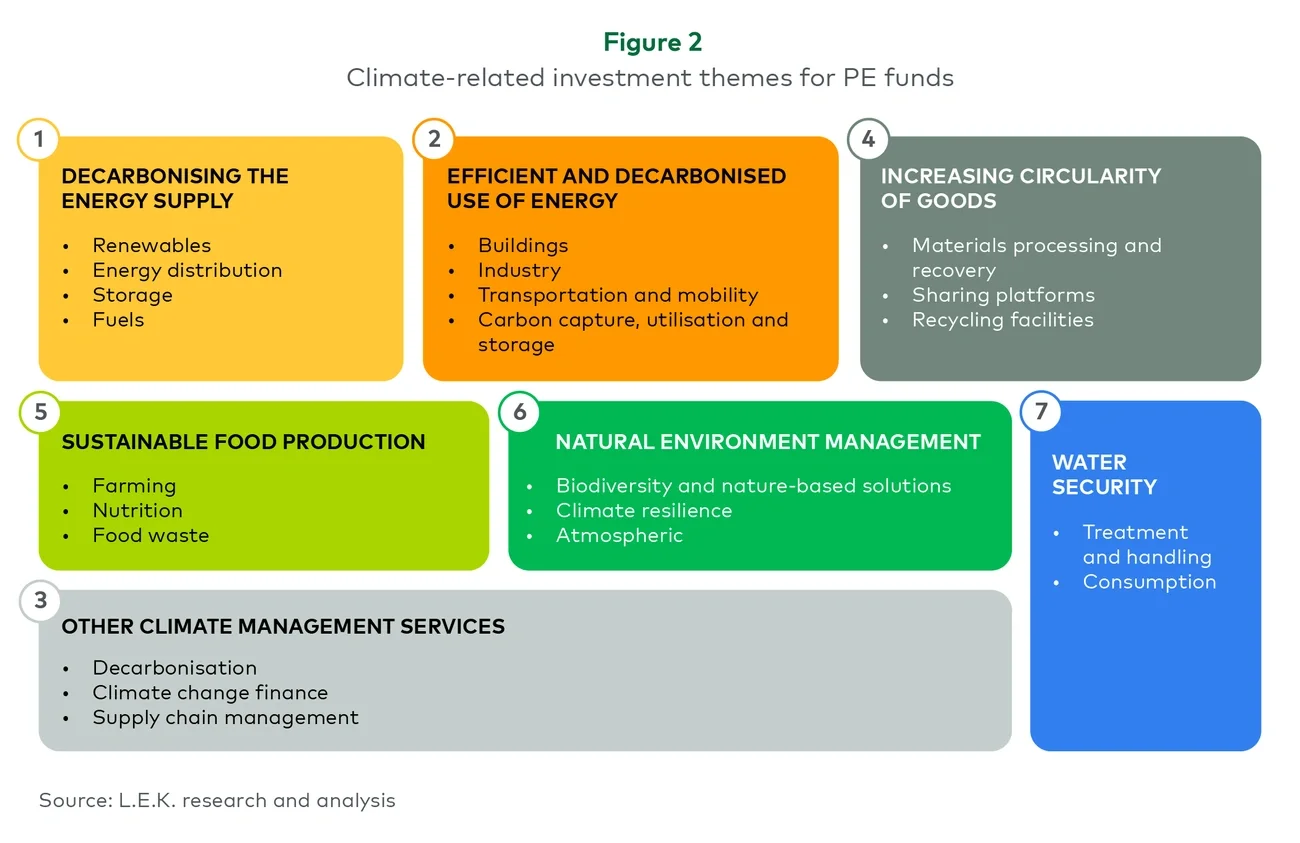

This trend reflects a growing recognition of the financial and environmental benefits of investing in sustainability assets, as well as heightened environmental, social and governance (ESG) concerns, regulatory pressures and technological advancements, which are driving expansion of the green economy (see Figure 2). Particularly in Europe, investment has been driven by increased regulatory pressure due to energy security concerns around Russian gas and the war in Ukraine. The sustainability assets PE firms have invested in encompass several key investment themes.

Image

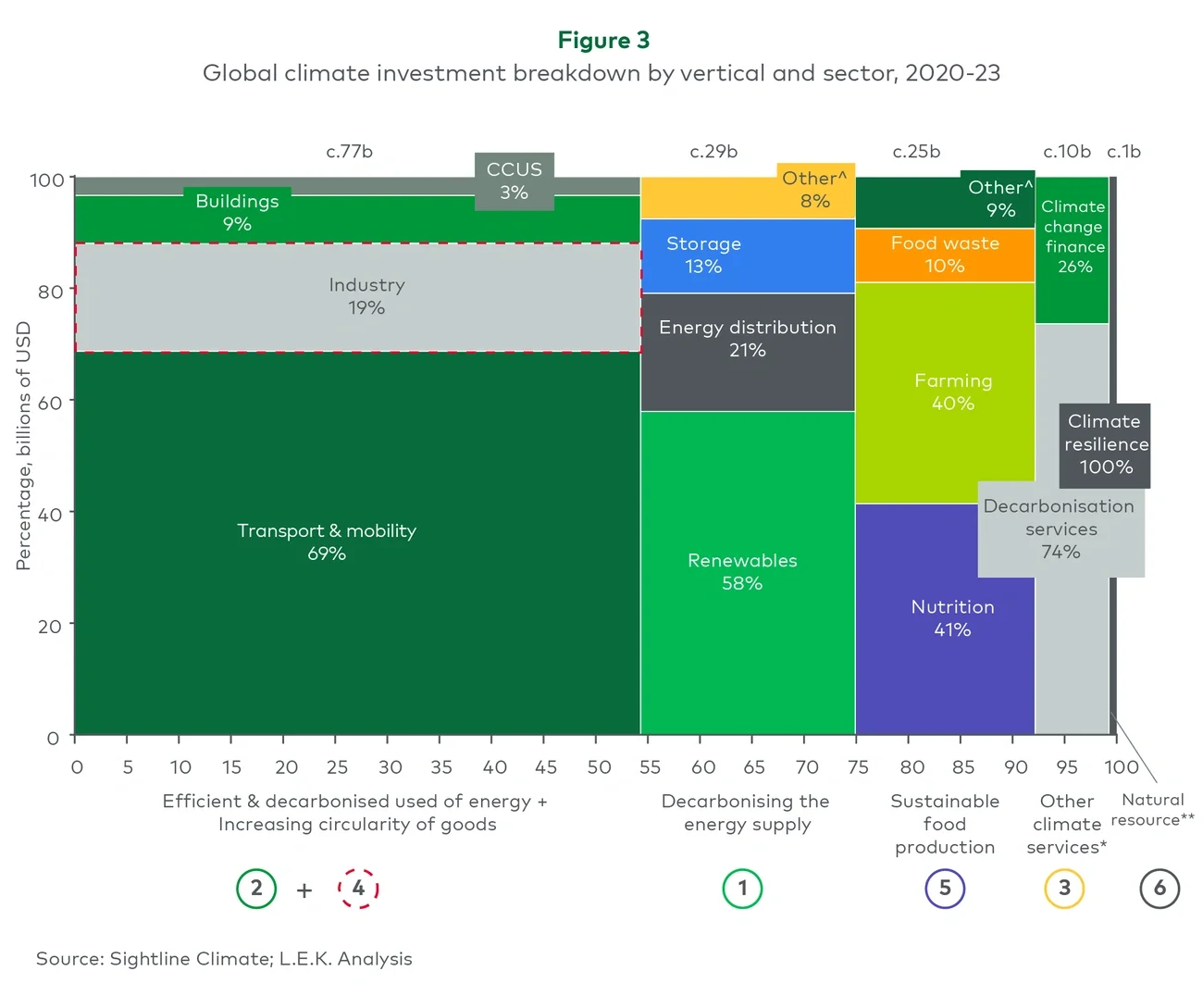

The theme that has attracted the most investment is the efficient and decarbonised use of energy, which has accounted for c.54% of climate venture and growth investments in recent years. Other themes attracting substantial investment include decarbonising the energy supply (c.20%), sustainable food production (c.18%) and other climate management services (c.7%). The latter includes services such as carbon measurement and accounting software, green finance platforms, and traceability and mapping software (see figure 3).

Image

The largest investment subcategory between 2020 and 2023 was the decarbonised use of transportation and mobility. This includes opportunities such as electric vehicles, sustainable aviation fuels and hydrogen-powered marine and rail transportation. Transportation and mobility accounted for c.49% of all global climate investments from 2020 to 2023.

Another important investment theme was decarbonising the energy supply, which includes investments in renewable energy supplies such as solar, wind and hydrogen; upgrading energy distribution infrastructure such as microgrids and pipelines; and enhancing energy storage solutions.

There has also been a strong focus on increasing the circularity of goods through second-hand goods marketplaces and re-commerce, recycling and waste management solutions. Additionally, sustainable food production — through vertical farming, regenerative agriculture and alternative proteins — is gaining traction. Sustainable food production addresses both food security and environmental sustainability.

The increasing allocation of PE funds towards sustainability assets highlights a transformative shift underway in global investment strategies. By channelling capital into diverse and impactful areas such as renewable energy, circular economy solutions and sustainable food production, PE is playing a pivotal role in driving the global transition towards a more sustainable and resilient future.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting

Related insights

You might also be interested in these insights.

English