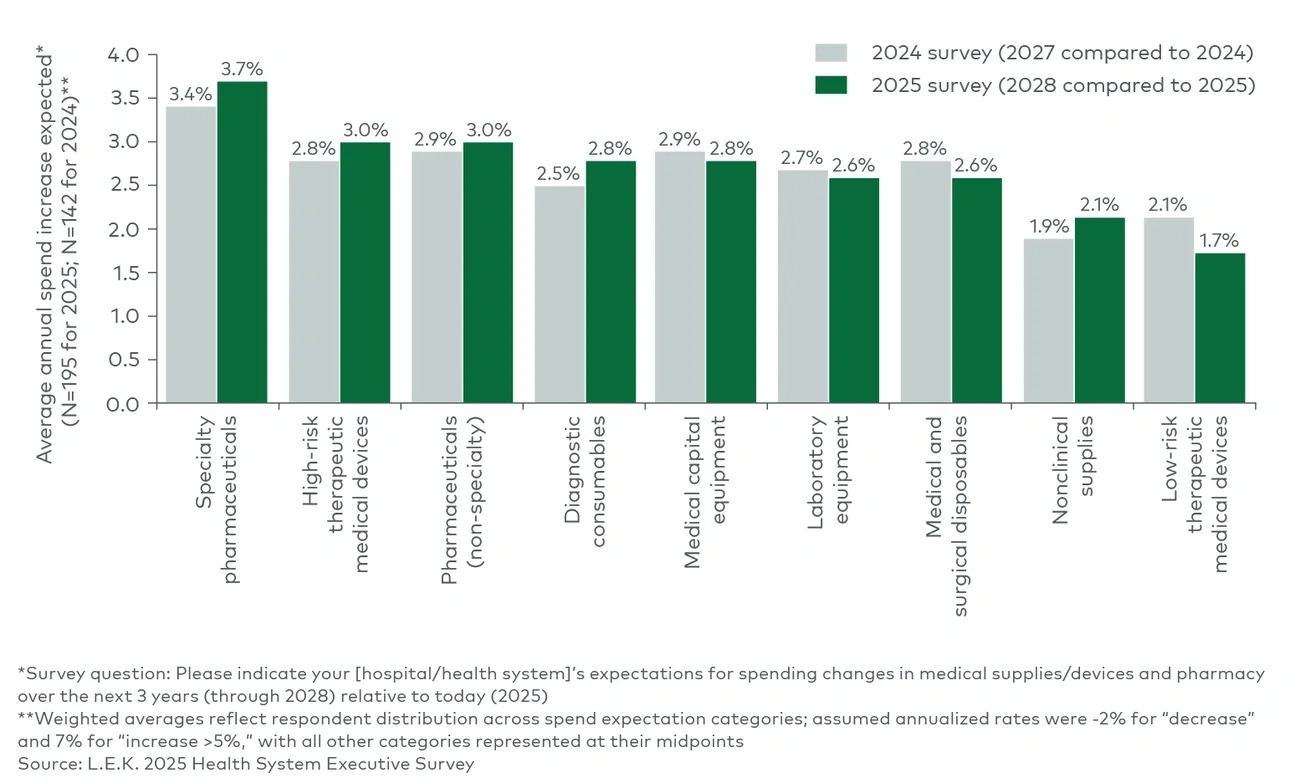

This steady outlook persists despite ongoing tariff exposure, labor inflation and supply chain cost pressure — indicating that hospitals do not expect to absorb major price increases. Instead, they anticipate suppliers will share in cost mitigation, whether by absorbing tariff and input cost impacts or by managing device and supply pricing through contracting discipline, product standardization and sourcing efficiencies such as multiyear agreements or volume-based rebates.

For medtech companies, the implications are clear: Pricing leverage will stay limited, even as demand for clinically essential products holds steady. Hospitals will also look to features beyond clinical performance alone, increasingly assessing how products influence total cost and workflow efficiency. They will favor suppliers that guarantee continuity, offer substitution options and support product standardization. They will also value devices that capture structured data or integrate billable events in electronic medical records to improve coding accuracy and payment integrity.

Positioning medtech for success in this environment

The 2025 L.E.K. Hospital Survey highlights a customer base focused on financial discipline and selective innovation. For medtech executives, four imperatives stand out:

1. Lead with efficiency.

Clearly quantify and communicate how products lower total cost — through reduced procedure time, shorter staffing requirements or higher throughput — and integrate this message into commercial, marketing and clinical discussions.

2. Strengthen supply chain partnerships.

Collaborate with providers to reduce disruption risk and total cost. This may include premium programs for guaranteed supply continuity, collaborative forecasting or standardization frameworks that balance choice and efficiency.

3. Expand value-added services.

With average selling price pressure intensifying, build complementary offerings — such as workflow optimization support, staff training or digital integration services — that create measurable operational value.

4. Collaborate closely with innovation-oriented systems.

Medtech growth will increasingly depend on partnerships with providers that are actively shaping care models and technology adoption. Collaboration may include tailored commercial engagement, shared development of products or workflows, or broader strategic alliances.

In upcoming Executive Insights, we will explore how hospitals are continuing to expand into ambulatory and other non-acute sites of care, how they are deploying AI and digital tools to improve efficiency, and more.

To discuss these findings — and how your organization can position for success in this evolving environment — please reach out to our Medtech team.

A special thank you to the Healthcare Insights Center for their contributions to this EI.

Note: AI was used to support the drafting of this article.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC