General CDMO landscape

Contract development and manufacturing organizations (CDMOs) have become critical enablers of innovation and scalability across a wide range of industries. They provide end-to-end services — from product development and regulatory support to manufacturing, assembly and postmarket services — helping original equipment manufacturers (OEMs) focus on core R&D while outsourcing capital-intensive and highly specialized production activities.

The global CDMO ecosystem is multimaterial, multi-industry and increasingly specialized, often rooted in deep capabilities in metals (e.g., nitinol, titanium), plastics (e.g., injection molding, extrusion), silicone, ceramics and advanced coatings. This material versatility allows CDMOs to serve multiple regulated industries — ranging from medtech and biopharma to consumer electronics and automotive.

Key drivers of the CDMO model:

- Manufacturing specialization: CDMOs offer OEMs access to high-precision, cost-efficient and specialized processes they cannot justify in-house

- Material-adjacency expansion: Many CDMOs scale across sectors by leveraging expertise in specific materials or fabrication methods (e.g., a plastic injection molding CDMO moving from consumer products into drug delivery devices)

- Asset-light growth for OEMs: CDMOs reduce OEM capital expenditure while supporting scalability and faster go-to-market timelines

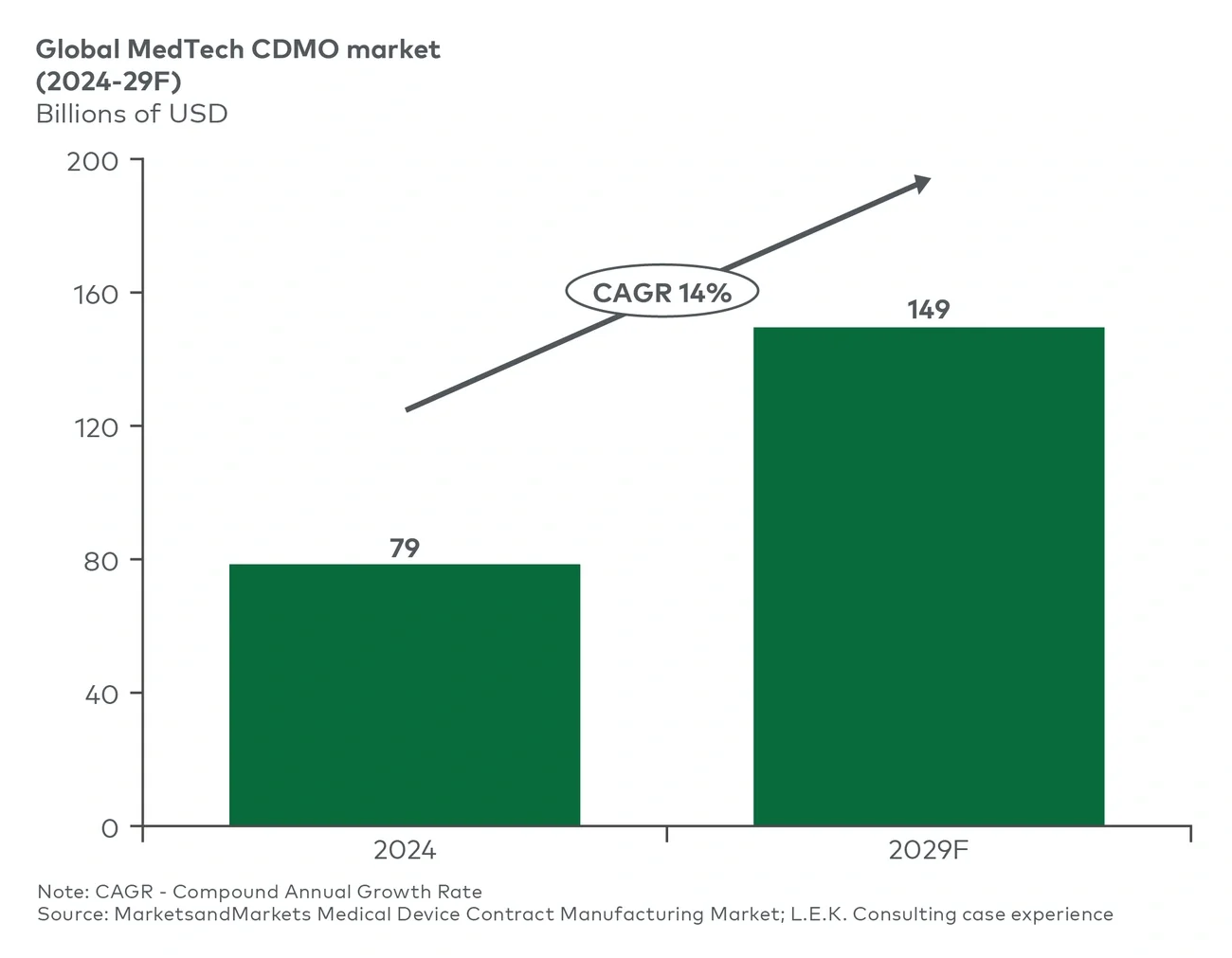

Global medtech CDMO landscape

Medtech CDMOs represent one of the most attractive verticals in the broader CDMO space (see Figure 1). Unlike general industrial or electronics CDMOs, medtech manufacturers operate in tightly regulated environments, needing to meet the standards of the U.S. Food and Drug Administration or the International Organization for Standardization, or to gain the CE mark; furthermore, they serve OEMs with eight-to-10-plus-year product life cycles and produce devices that are central to patient outcomes and safety.