In L.E.K. Consulting’s previous article in the 2025 Health System Executive Survey series, we highlighted the divide in the financial health of U.S. hospitals and health systems, with roughly half of executives reporting that their organization’s position is constrained. Across both financially constrained and stable systems, however, most leaders pointed to three key priorities: increasing operational and cost efficiency, enhancing supply chain and purchasing, and improving revenue capture and revenue cycle management (RCM). For systems under pressure, these moves are critical to stabilize performance, while for stronger systems they are equally important in order to protect margin, create capacity and maintain a competitive edge.

This edition of L.E.K.’s Executive Insights examines:

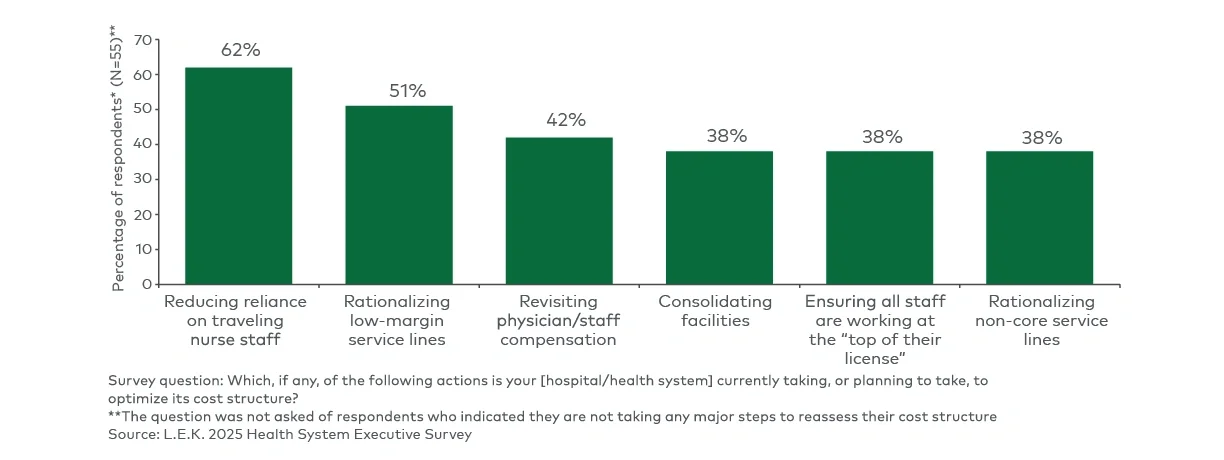

- What hospital and health system leaders are doing to reduce costs and increase operational efficiency

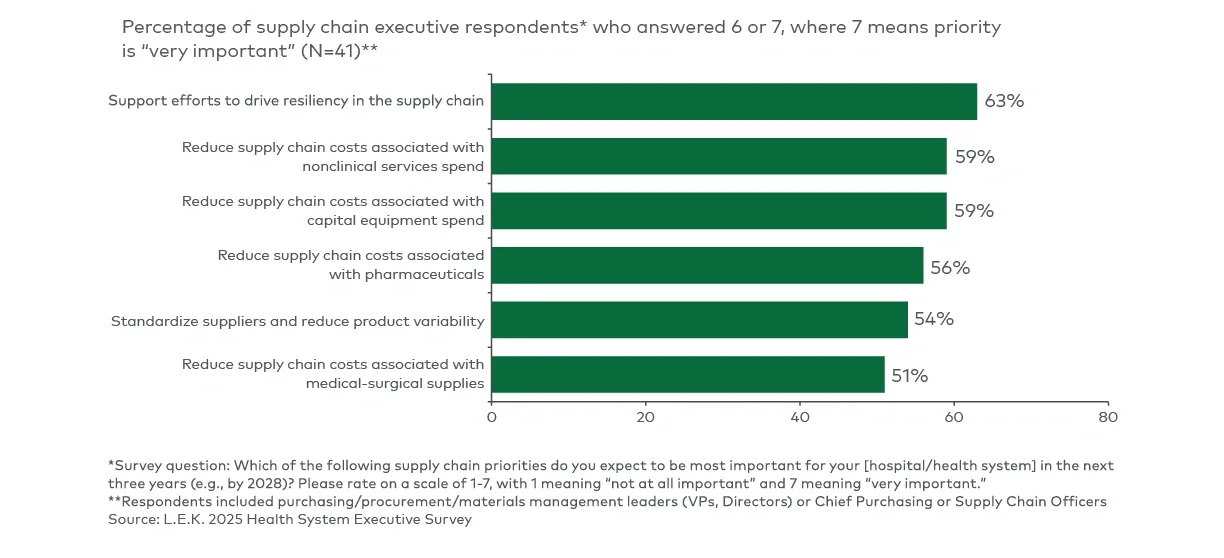

- What supply chain and purchasing priorities hospital leaders are elevating — and the immediate cost-cut actions to take

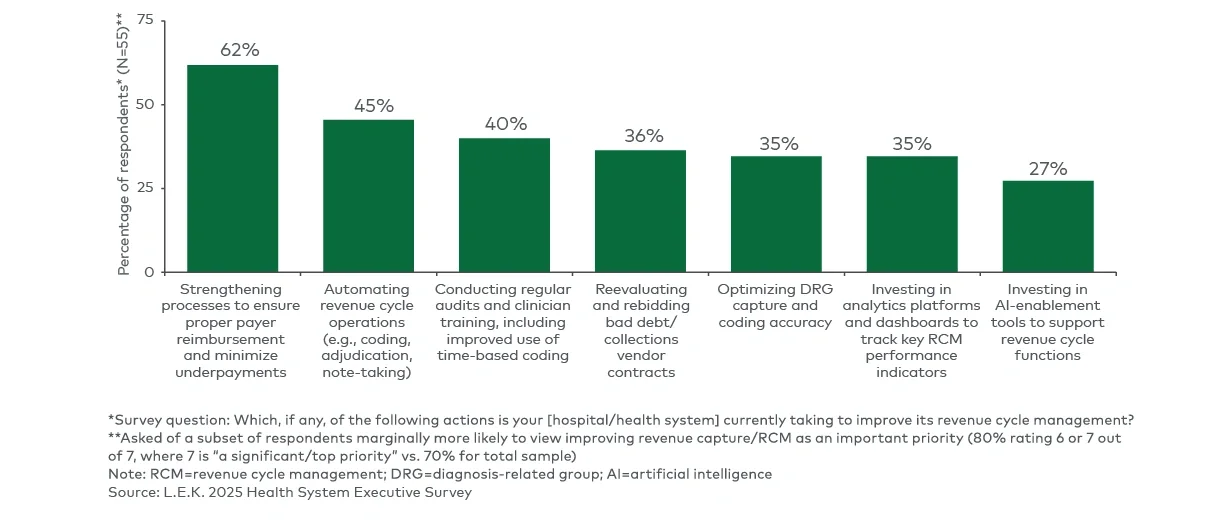

- The continuous improvement playbook hospitals are deploying for RCM

- Pharmacy operations as a case study in advancing all three priorities

Increasing operational and cost efficiency

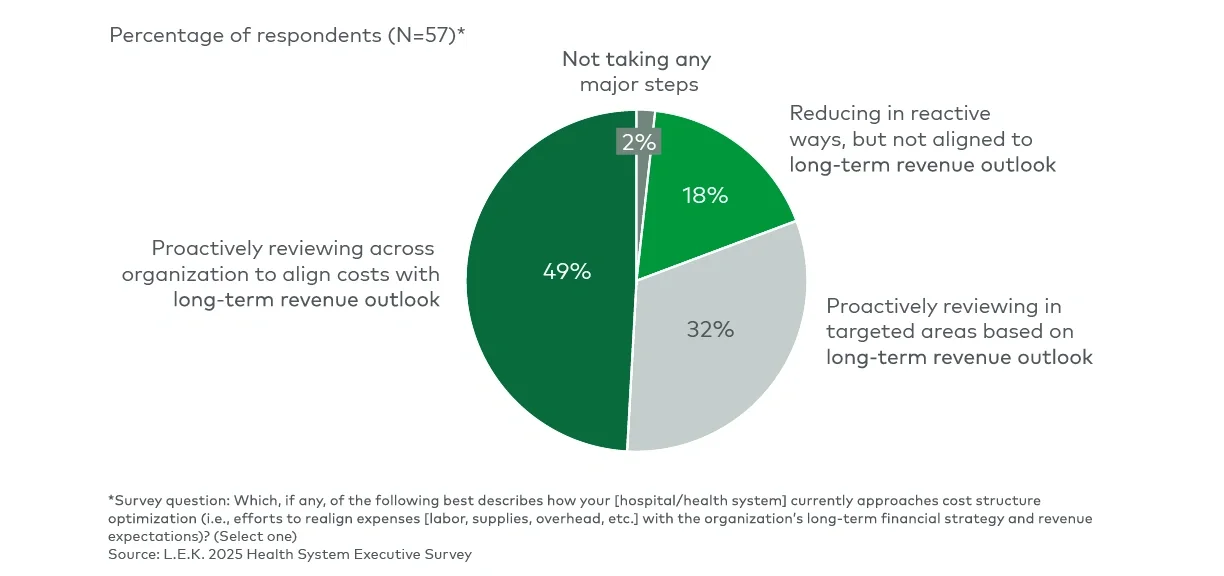

Increasing operational and cost efficiency is the No. 1 strategic priority cited in this year’s survey — and today’s operating environment leaves little room for reactive cost measures. In fact, 8 in 10 hospitals and health systems report proactively reviewing costs against their long-term revenue outlook as opposed to reactive reductions (see Figure 1).