Introduction

The U.S. healthcare market continues to evolve as the market has transitioned after the height of the COVID-19 pandemic. As a result of patients’ increased desire for virtual care, the labor/staffing challenges and the evolving regulatory landscape, the need for robust healthcare information technology (HCIT) solutions has never been greater. L.E.K. Consulting defines HCIT as provider (including pharmacy), payer and life sciences tools that optimize clinical, financial and operational activities to improve patient outcomes/engagement, enhance financial results, and yield efficient, effective and timely operational processes.

Since the onset of the pandemic in March 2020, over 700 M&A transactions have been consummated in U.S. HCIT.1 For market participants and investors, a number of questions arise in terms of how to make sense of these deals. How does recent activity compare to previous years, and where is the market headed? What types of companies are being acquired and combined? What assets drive value for care providers and other health organizations? Our analysis of these transactions yielded insights in four key areas: overall deal trajectory, areas of expansion for providers, the increasing importance of medical/care management software and the role of private equity (PE) in the market.

Overall deal trajectory

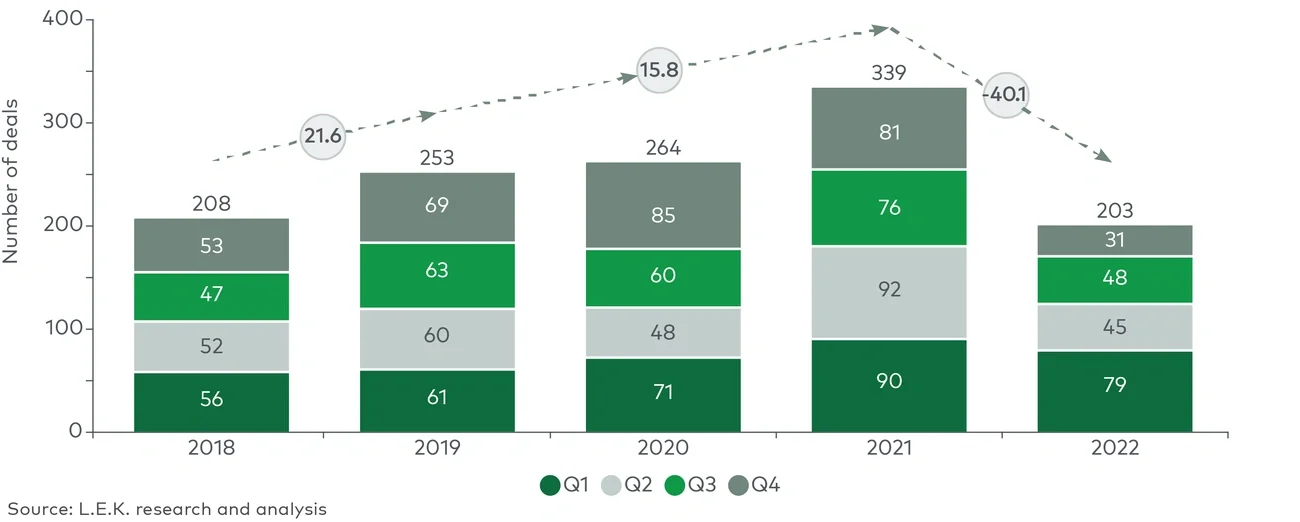

Prior to the pandemic, deal volumes had been growing consistently. From 2018 to 2021, total transactions increased approximately 18% p.a., from 208 deals to 339, despite a brief slowdown in Q2 and Q3 2020 during the initial COVID-19 outbreak shutdowns (see Figure 1). This flurry of activity was catalyzed by pandemic-related issues, such as the sudden/urgent need for more robust virtual care capabilities and labor/staffing issues.