Implants have emerged as the standard-of-care alternative to crowns as well as dentures to support implant-retained partial or full-mouth rehab. Implants provide improved functionality (e.g., better durability, bite strength), bone health, and aesthetics, driving strong U.S. dental implant growth of high single to low double digits annually through 2028F. Growth and expansion of the implant market is also supported by the emergence of implants at varied price points (i.e., premium vs. value implants) and the democratization of care supply.

Democratization of care supply

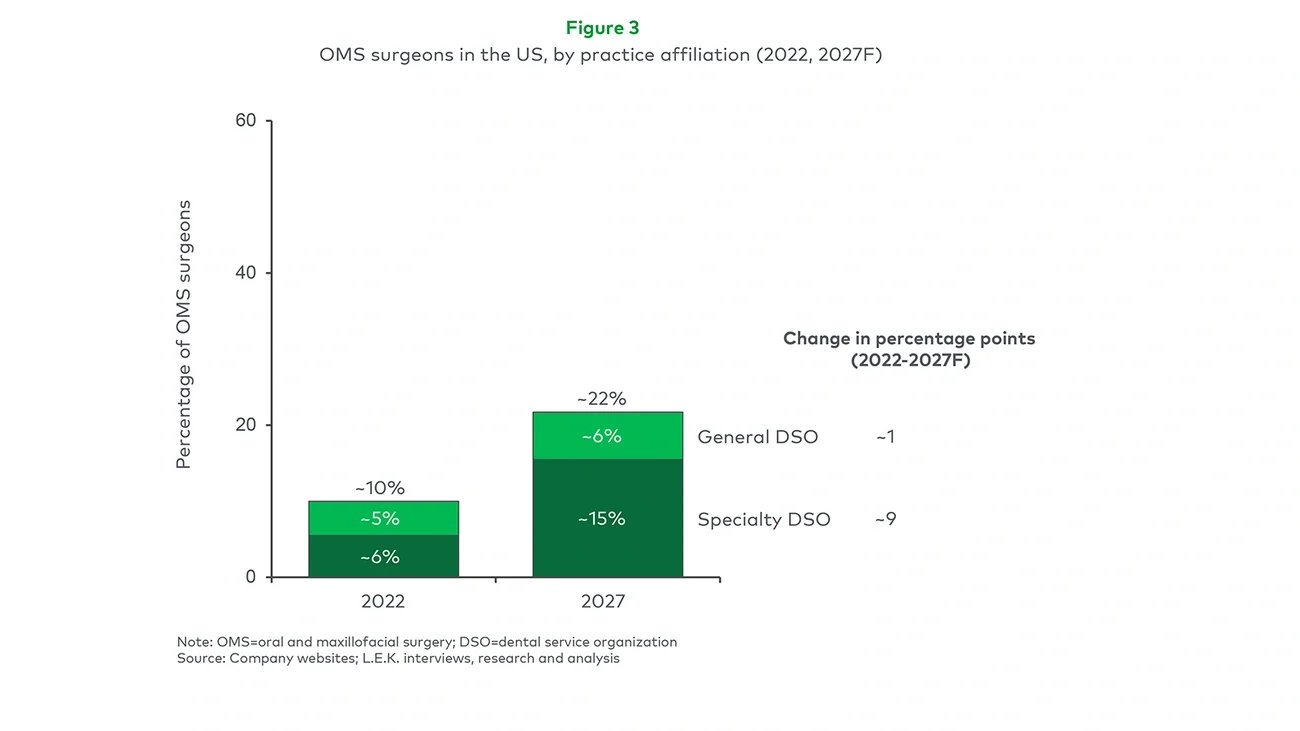

A growing number of GPs have started to offer specialized services and advanced procedures like implants, extractions and orthodontics — once reserved solely for specialists — especially in patients with less complicated cases. This shift has resulted from advances in dental technology (i.e., increased utilization of digital dentistry discussed above) as well as training on more advanced procedures offered in dental schools as part of the core curriculum and within clinician networks. Going forward, the dental market is set to expand further, given the greater patient reach enabled by “super GPs.” Patients who seek specialized services and advanced procedures from GPs tend to be more price sensitive (potentially reluctant to seek the services of specialist dentists), often influenced by direct-to-consumer marketing and social media advertising of aesthetic smile improvement solutions.

Expansion of dental coverage via Medicare Advantage and dental wellness programs

Dental coverage has seen some expansion recently with the growth of Medicare Advantage. While original Medicare largely does not cover routine dental care, many Medicare Advantage plans offer relatively broad dental coverage (e.g., full mouth restorations and implants) with low patient out-of-pocket costs to attract new members. The number of lives covered by Medicare Advantage is expected to continue to increase, driving parallel dental coverage expansion. Moreover, dental wellness programs (e.g., Delta Dental Wellness Plan) are also becoming more prevalent with the goals of prevention and cost savings. Some dental wellness programs are employing targeted interventions for high-risk patient populations to support oral care.

Implications

In the context of these dental trends, there are various implications that dental market stakeholders across the value chain should consider as they shape their go-to-market strategies and identify areas for investment going forward.

Overall, the dental space is a sizable market growing healthily, driven by established, developing trends (e.g., growing prevalence of DSOs, continued adoption of digital technologies) as well as newer, emerging phenomena (e.g., increased utilization of teledentistry, the “Zoom effect,” expanded coverage via Medicare advantage), providing opportunities for market stakeholders.

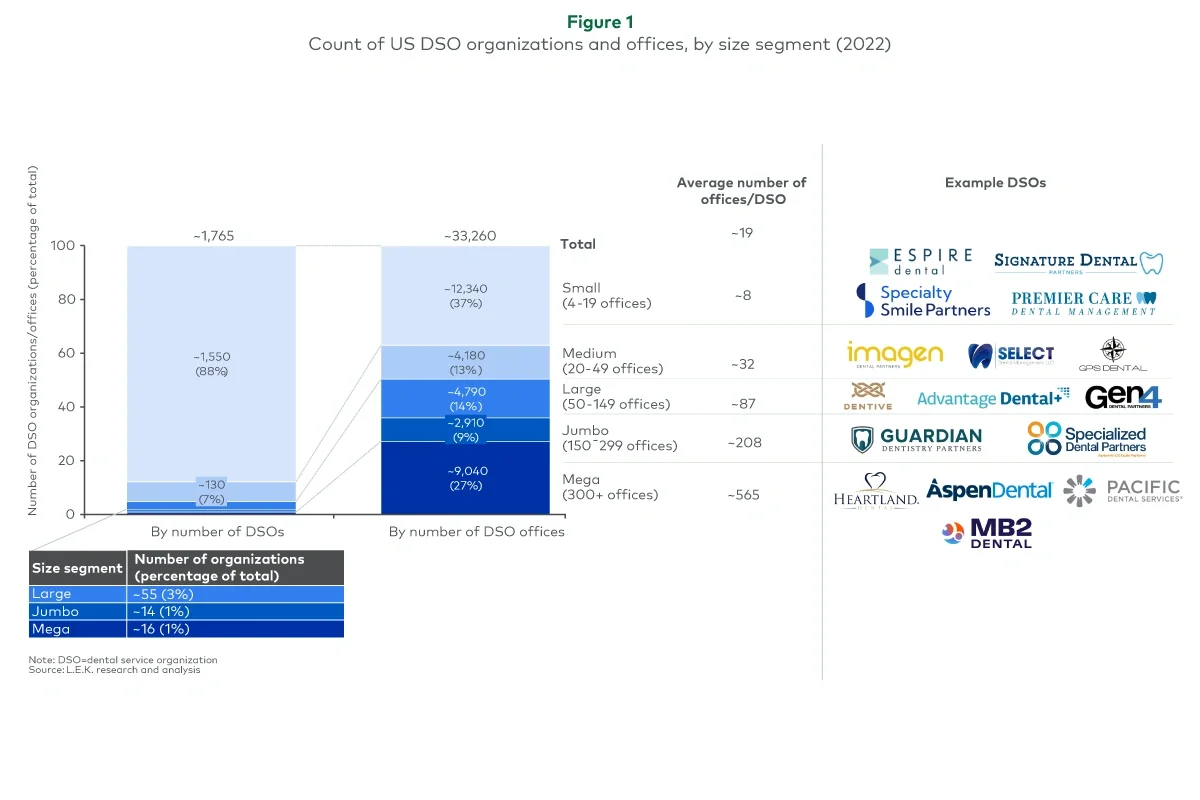

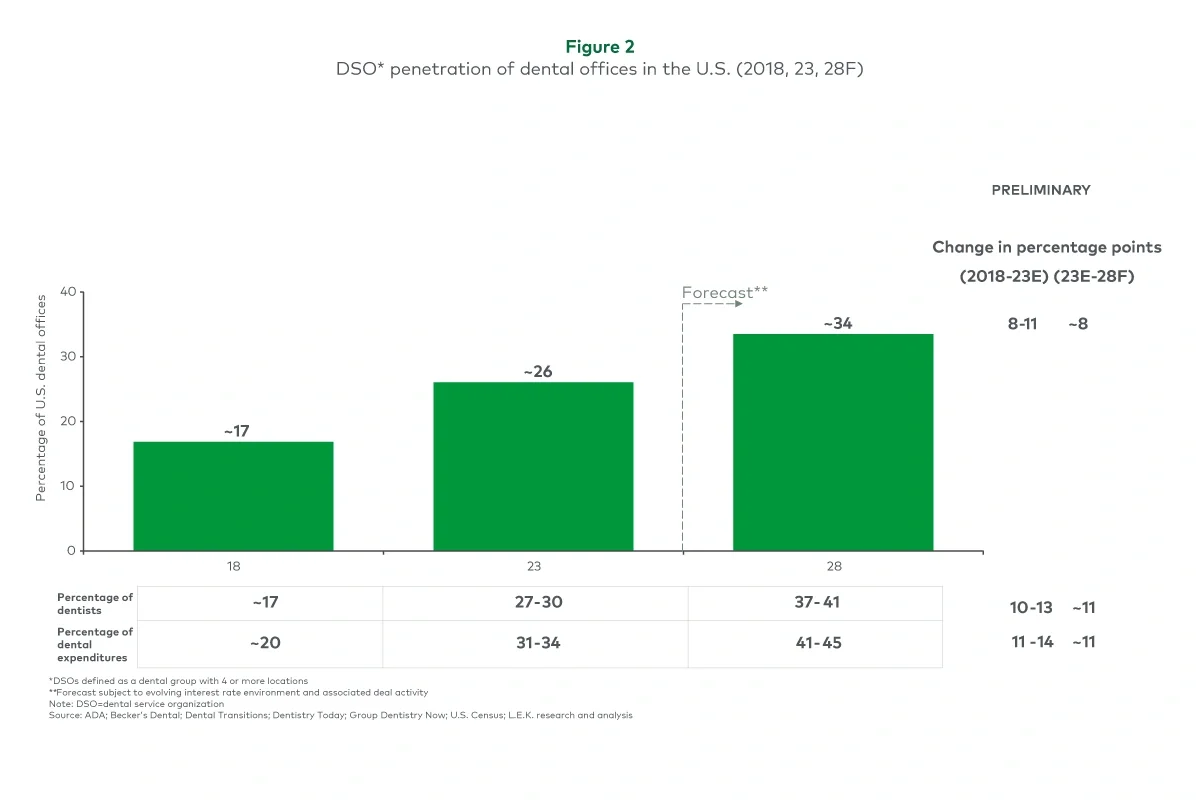

Dental scaled platforms such as DSOs have ample runway for continued growth. While an upward limit likely exists for the proliferation of these platforms, we are far from that limit, as independent dental practices continue to make up a sizable segment in the overall landscape of dental providers.

- DSOs looking to scale should acquire/partner with dental practices in metropolitan statistical areas (MSA) with attractive supply (e.g., high concentrations of GP dentists or specialists) and demand (e.g., older populations, high numbers of lives covered through commercial insurances and/or Medicare Advantage) dynamics, as well as a favorable competitive landscape (i.e., low relative DSO penetration). As DSOs continue to acquire/partner with dental practices, it is increasingly important to differentiate the platforms (e.g., by offering various JV models or levels of collaborative decision-making) to continue to attract practice owners.

Dental OEMs, dental labs and ancillary dental providers (e.g., providers of continuing dental education) should align their commercial efforts to service the two key customer segments (DSOs and independent dental practices) that have differing needs and expectations.

- For example, when it comes to purchasing dental lab products, independent dental practices generally value quality, relationships and service, while DSOs predominantly place a higher emphasis on price and scale.

- It is also essential to consider differing needs across dental scaled platform sub-segments (e.g., large, standardized nationally branded DSOs vs. small regional DSOs that essentially operate as independents) to further tailor offerings and sales approaches.

- What’s more — across dental scaled platforms — dental OEMs, dental labs and ancillary dental providers should not only maintain strong relationships at the corporate platform level but also continue to expand support and touchpoints with dentists at the contracted practices.

As dental OEMs, dental labs and ancillary dental providers focus on dentists, they should continue to specifically evolve their strategies and sales teams to cater to the growing number of GPs providing specialized services and their more price-sensitive patients. Since not all GPs are created equal, expanding reach to target GPs should involve careful segmentation and robust analysis along key dimensions such as current use of digital dentistry, age, patient volume and DSO affiliation. Super GPs will continue to look for easy-to-use, digitally enabled technologies as well as readily available product training to support such solutions.

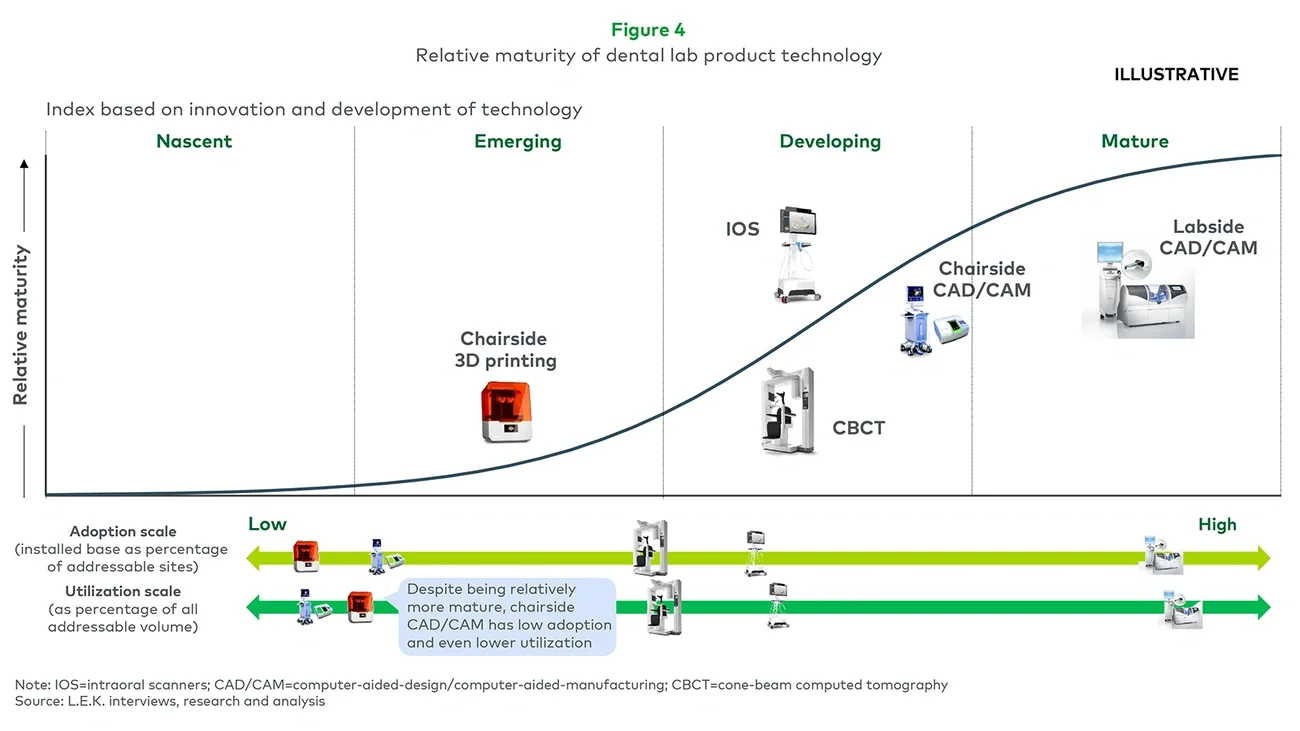

For the more nascent technologies (e.g., 3D printing), there is still a need to drive penetration, focusing on placement and being at the cusp of technological advancements.

For the more established technologies (e.g., labside CAD/CAM), there is an appetite among dentists for solutions that can improve characteristics such as throughput speed and capacity.

The current ceiling around chairside CAD/CAM penetration may be lifted if dental OEMs can design systems that address some of the widespread utilization barriers, including operational burdens. To date, nothing has moved the needle on chairside CAD/CAM adoption and use.

For more of L.E.K.’s insights into dental market dynamics, please reach out to medtech@lek.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting LLC