The Southeast Asia (SEA) medtech market is growing rapidly, driven by an expanding middle class, aging populations, and increasing healthcare investments. Despite these promising macro trends, MNCs face persistent challenges including fragmented regulations, complex procurement mechanisms, and heterogenous market opportunity across the region.

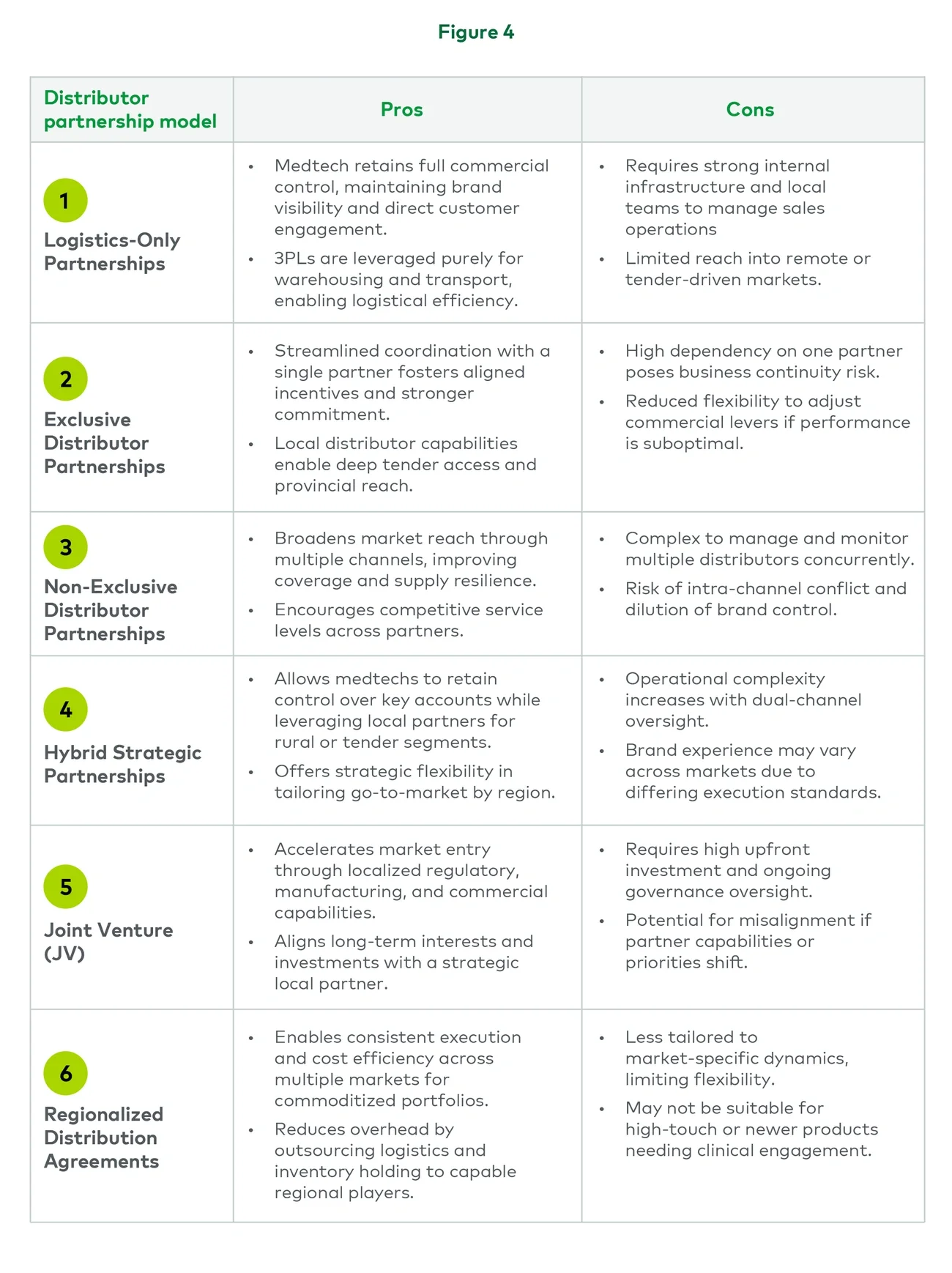

In this context, distributor partnerships have emerged as critical enablers of market access and sustainable growth, offering an effective alternative to direct market entry by companies. Distributors offer MNCs local regulatory knowledge, access to fragmented markets, and the flexibility to tailor commercial models to specific market conditions. These partnerships extend across the value chain, spanning importation, logistics, registration and commercialization support, allowing medtechs to scale effectively while managing risk.

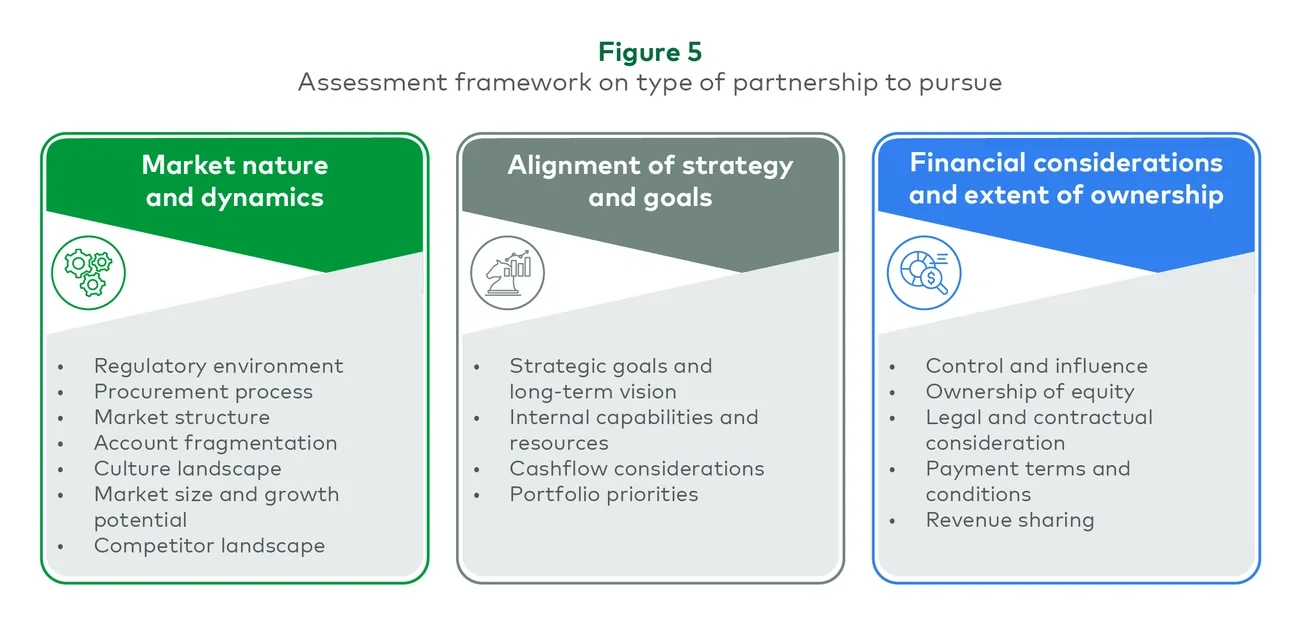

In this paper, LEK Consulting aims to provide a structured view of distributor partnerships in SEA, examining the drivers, trade-offs of different partnership models, and key questions/considerations to inform a resilient and scalable commercialization strategy mediated by distributor partnerships.

Section 1: Drivers of distributor partnerships in SEA

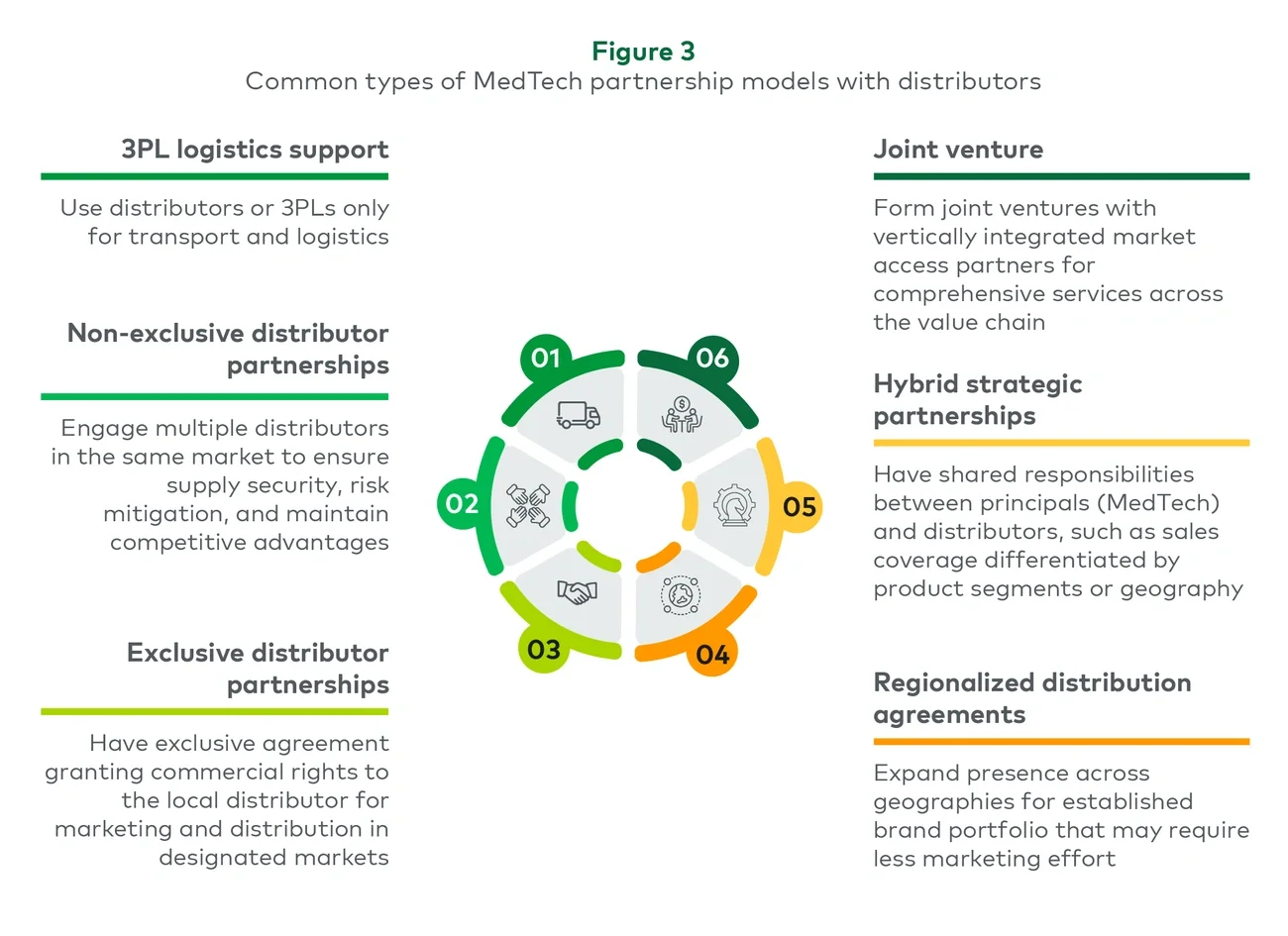

The diverse nature of SEA markets requires a flexible and customized approach to market entry and expansion. Local distributors, with their in-depth market knowledge and networks, play a crucial role in this strategy. Key factors driving the increasing reliance on distributor partnerships include: