Introduction

Europe has long stood at the forefront of academic excellence in life sciences. It hosts 37 of the world’s top 100 life sciences universities (versus 34 in the US).1 Moreover, the continent consistently leads the US in biomedical publication volume and citation impact. Yet a persistent gap remains between scientific innovation and commercial output in Europe compared to the US.

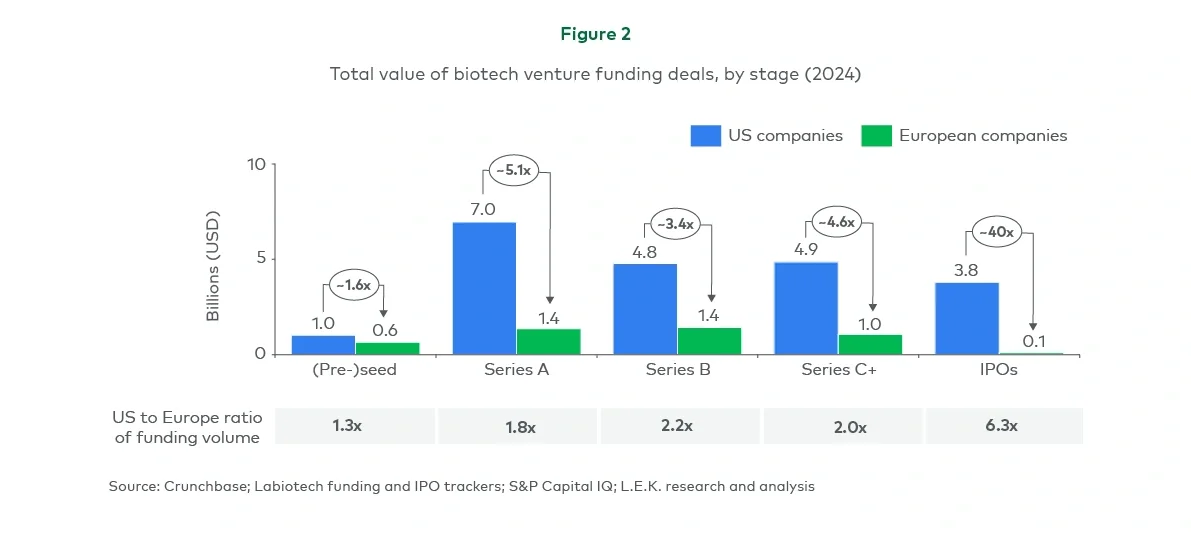

As the competition for biotech capital intensifies globally, key questions arise: How can stakeholders across the European ecosystem work to close the translational gap with the US? And what steps can European biotechs take to maximise their chances of success?

Diverging pathways from innovation to impact in Europe and the US

To highlight the commercial gap between the two markets, L.E.K. Consulting analysed the innovation pipeline from academic publication to drug approvals, focusing on drugs originating in academic or biotech institutions.2

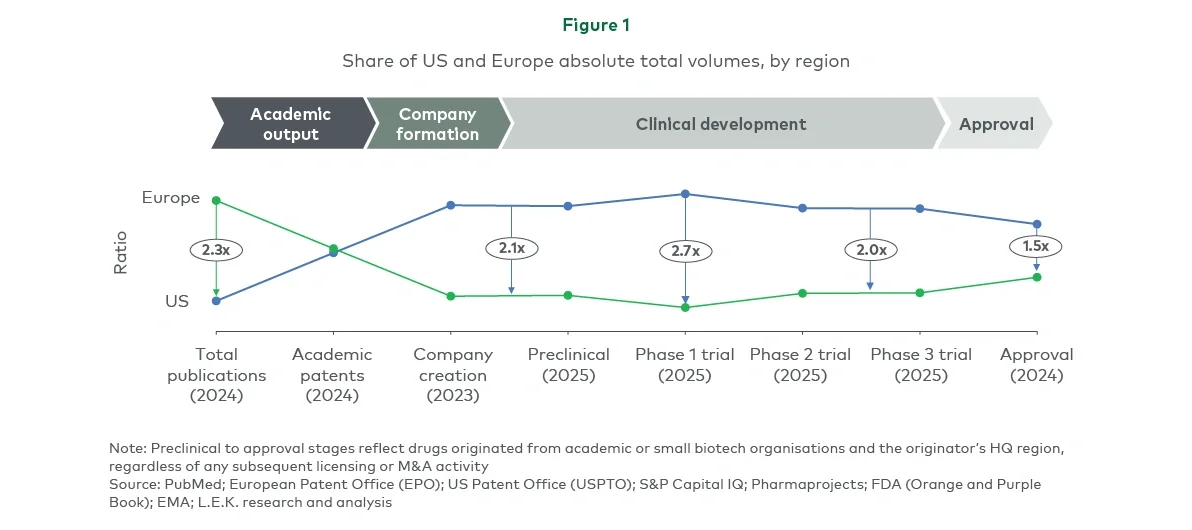

Europe publishes over twice as many publications as the US, but this advantage disappears at the academic patent stage (see Figure 1). In 2023, the US also founded more than twice as many biotech companies as Europe, despite a sharp decline in both regions since 2021.

The gap persists through development to the drug approval stage — US-originated intellectual property (IP) now accounts for 1.5 times more approvals than Europe, and this has been relatively consistent over the past five years.

Europe also lags in company maturation: US-headquartered small biotechs (revenue under $2 billion) independently launched more than three times as many drugs as European biotech peers from 2018 to 2024.