SME quote: “The competitive environment has changed. Distributors aren’t just facing macroeconomic headwinds — they’re up against competitors engineered for integration and operational excellence, while serving customers who are smarter and more demanding than ever.”

In addition to improving underwriting quality and technology integration, MGAs must improve visibility into book performance, which can often feel like a black box. MGA clients also want claims analytics to understand claims trends, benchmark against peers and manage premiums.

For carriers, value creation increasingly depends on choosing distribution partners that offer both scale and insight — those with access to clean data, niche specialization and integrated risk solutions.

6 imperatives to compete and win

Winning in the next cycle will require a reset in both strategy and execution. Success won’t come from incremental change but from executing a focused set of strategic shifts.

We have identified six imperatives that will define the next era of commercial P&C distribution.

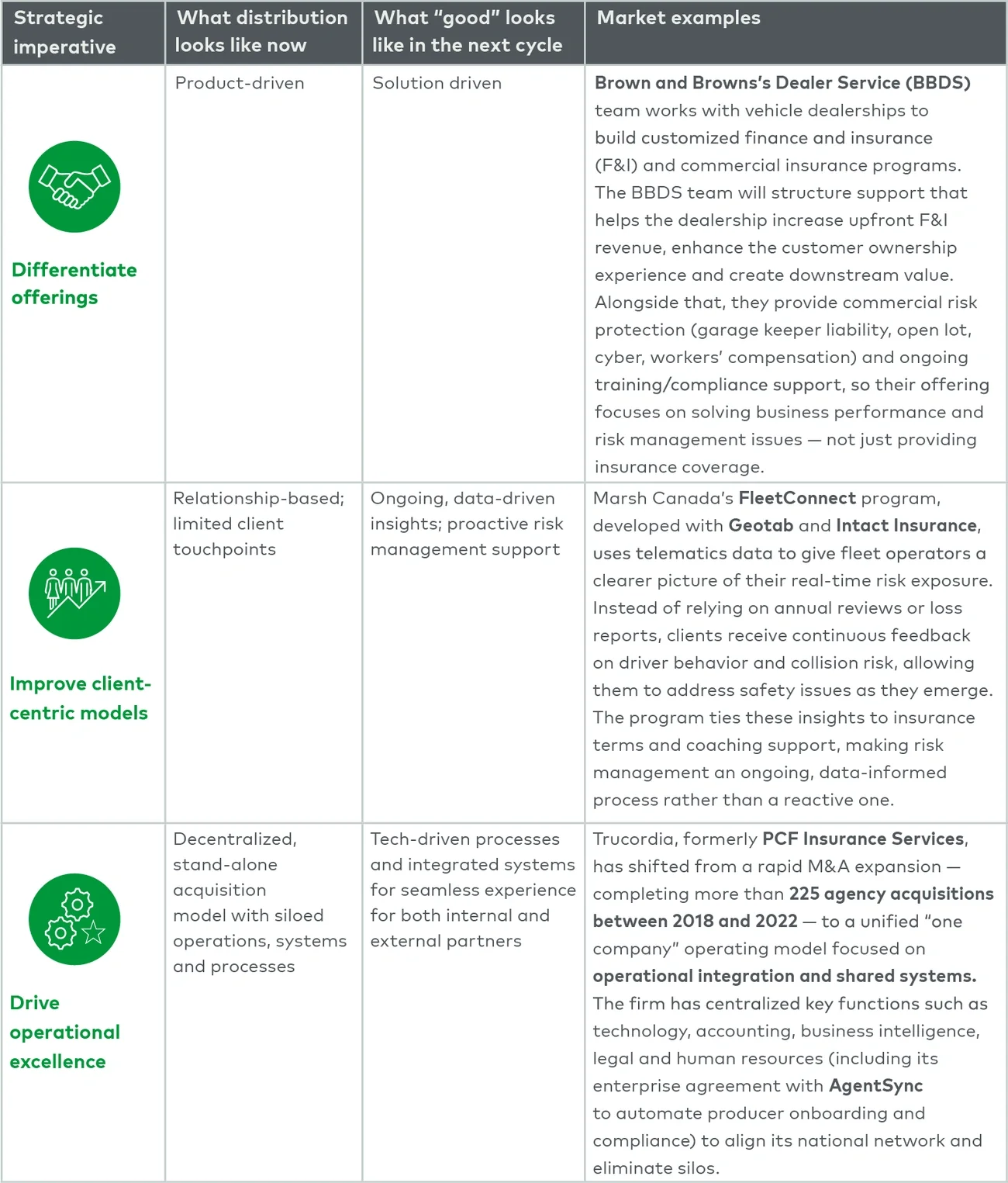

1. Shift from consolidation to integration

Brokers and MGAs must shift focus from targeting the next investment to extracting the value from past acquisitions. Private equity sponsors and strategic acquirers are prioritizing EBITDA improvement through synergy realization and platform integration. Distributors should aim to unify systems and data infrastructure across entities, harmonize compensation, and optimize market access.

Carriers must now extract value from their web of MGA and broker relationships. While MGAs want to maintain flexibility with underwriting and pricing, carriers look to control risk and maintain reliable returns. Carriers should leverage near real-time data (vs. monthly/quarterly reports) that enables them to spot emerging trends and resolve issues with MGAs before losses mount.

2. Choose your lane and own it

Distributors should shift from being generalists to serving as specialists. In mature markets, distributors must look to exploit and sharpen expertise, which can include geography, client size and client segment. Next-generation distributors won’t try to be everything to everyone. Instead, they will identify core strengths and build upon them.

The key to specialization is differentiating. Determine whether your company competes best on differentiated products, customer excellence or operational efficiency. Distributors that try to compete on too many fronts will fail against market specialists and niche providers.

Successful specialization requires a clear-eyed assessment of existing strengths and how to deploy them effectively. For example, one broker used a locally driven, relationship-based model to dominate in the middle market through deep client loyalty. By contrast, some high-touch, bulge-bracket players have struggled to move down-market, where midsize clients have very different needs, and far less appetite or budget for complex service models.

For carriers, developing a segmented distribution strategy will be essential. A well-defined approach should clearly delineate which risks are best served through delegated authority arrangements (e.g., MGAs) and which are more effectively handled in-house or through digital direct-to-client channels.

3. Leverage scale in fee negotiations

In the recent hard market, higher rates, restrictive underwriting conditions and limited capacity forced distributors to broaden their carrier relationships. Rather than relying solely on preferred markets, brokers had to engage a wider range of carriers to secure adequate coverage for clients. This approach prioritized availability over alignment to meet demand.

Now the balance of power has shifted back toward distribution. As carriers return to growth mode and expand capacity, brokers can optimize their placement strategies. Brokers should now focus on capturing contingent income opportunities, particularly those linked to premium volume.

Acquisitions frequently leave brokers with multiple trade agreements across the same trading partners. Once centralized, that volume shifts to bargaining power that improves terms and rates.

MGAs that grew and developed profitable books through innovation and calculated risk-taking can now leverage their supplier power with both carriers and reinsurers that seek to grow in a more competitive environment. This can include negotiating better fronting terms, quota shares and deals. Carriers must defend margins by tiering partners based on performance, tightening governance over delegated authority and investing in automation to reduce servicing costs. Shifting toward outcome-based compensation and building low-cost digital or embedded channels can further offset rising distribution expenses while preserving underwriting control.

4. Deliver risk solutions, not just policies and coverage

Insurance buyers demand more than policy placement; they want a partner that will help manage and mitigate risk. Brokers and MGAs must integrate policies with operational risk tools and advice. Risk analytics tied to policies provide a servicing advantage over generalist distributors. More important, these integrated tools provide distributors with valuable risk and claims data that can inform their own product design and enable more accurate pricing.

To meet rising customer expectations, distributors must actively collaborate with managed service providers, insurtechs, and data platforms to gain richer insights and deliver more holistic solutions. These partnerships unlock new avenues for distributors to bring innovative offerings — such as cybersecurity monitoring, Internet of Things-enabled alerts, telematics-driven products and supply chain analytics — to market.

Carriers can co-invest or white-label such offerings, empowering their distribution partners to differentiate at the point of sale while deepening client engagement. In doing so, carriers move from being passive capacity providers to becoming active solution enablers, reinforcing retention, improving underwriting performance and creating value beyond price.

5. Evolve from data points to market value

Players that can move from data collection to data-driven action will set themselves apart in the market. But it’s not just about owning and activating data; brokers, MGAs, and carriers that build or own the infrastructure to aggregate client data will gain a larger share of the value chain. How? This infrastructure empowers seamless connectivity across the ecosystem, the integration of advisory tools and smarter UW decisions. This can fundamentally shift current client ownership dynamics.

A connectivity hub can automate paper-based submissions and instantly compare quotes across carriers, reducing turnaround time from days to hours and giving clients greater visibility into the process. Additionally, advanced advisory tools can incorporate disaster scenario modeling into client reports, moving beyond simple coverage demonstration to identify potential exposures and recommend proactive risk-mitigation strategies. For carriers, ingesting and leveraging distribution data will allow them to better manage risk and reduce volatility.

6. Double down on digital, or risk irrelevance

Ignoring the digital capabilities of newcomers, including rapid product launches and API-enabled architecture, will result in a diminished spot on the value chain. Distributors must invest in digital to provide the proactive service and improved client experience that insureds demand. Small commercial carriers can already offer digital quoting and policy management and can better identify cross-sell opportunities than larger distributors.

Client quote: “Digital tools aren’t optional. They determine whether we retain and grow clients or lose them to more nimble competitors.”

Navigating the next horizon

Next-gen leaders will engineer advantage through sharper focus, stronger integration and smarter data orchestration. While market tailwinds have faded, opportunity hasn’t. Brokers, MGAs and carriers that start the transformation today through system integration, digitized processes and aligning everything to client outcomes will win the next cycle. Change is coming. Will you lead it?

For more information, please contact us.

Endnote:

1InsuranceInsiderUS.com, “Global insurance pricing falls 4% over Q3: Marsh.”

https://www.insuranceinsiderus.com/

article/2fht83n5vu44f0uma3uo0/lines-of-business/commercial-lines/global-insurance-pricing-falls-4-over-q3-marsh?zephr_sso_ott=wigJQQ

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC