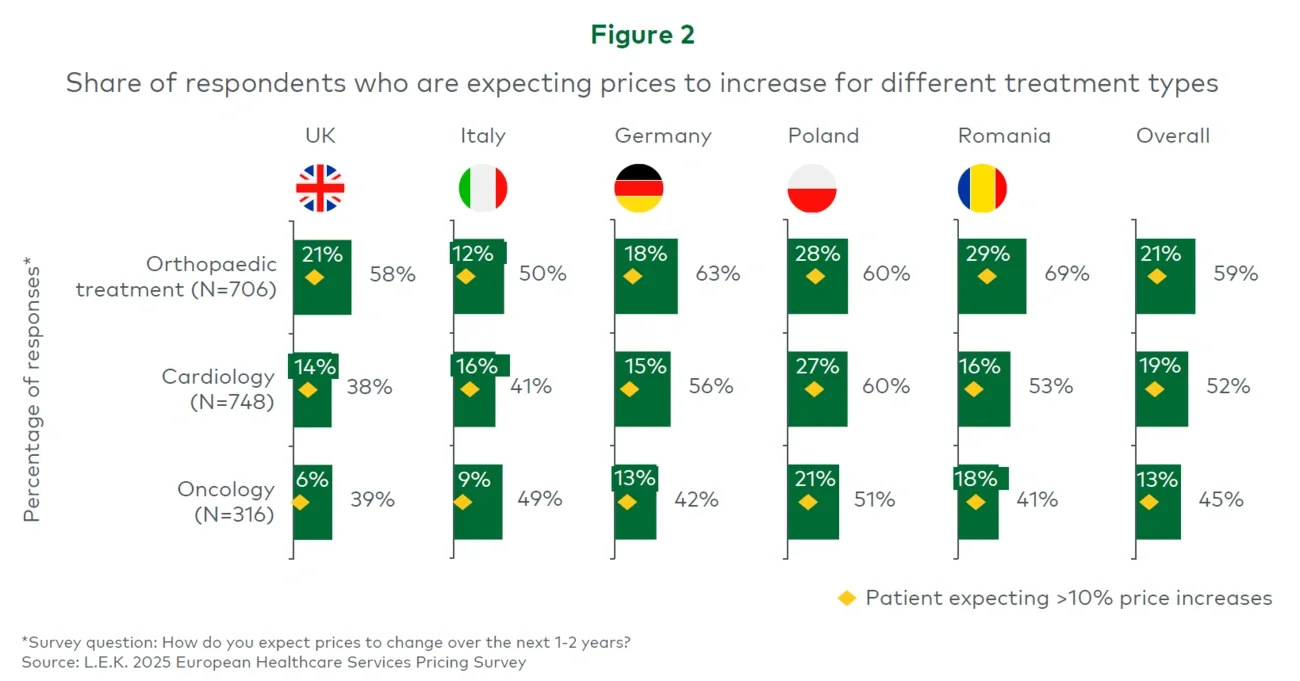

As out-of-pocket healthcare spending continues to rise across Europe, a major opportunity is emerging for providers: pricing strategy. Historically, pricing in the private healthcare sector has often been reactive, ad hoc and inconsistently applied — especially for out-of-pocket patients. But as private pay becomes a bigger slice of the pie, pricing is now a frontline strategic lever that can help capture value, drive share gain and open new patient segments. For example, in the UK, c.36% of patients surveyed indicated that they were more likely to pay for private healthcare for orthopaedics than they had been in the past five years.

L.E.K. Consulting’s recent survey of over 3,500 patients across five European markets sheds light on the shifting dynamics, from how patients think about pricing to where providers are leaving value on the table.

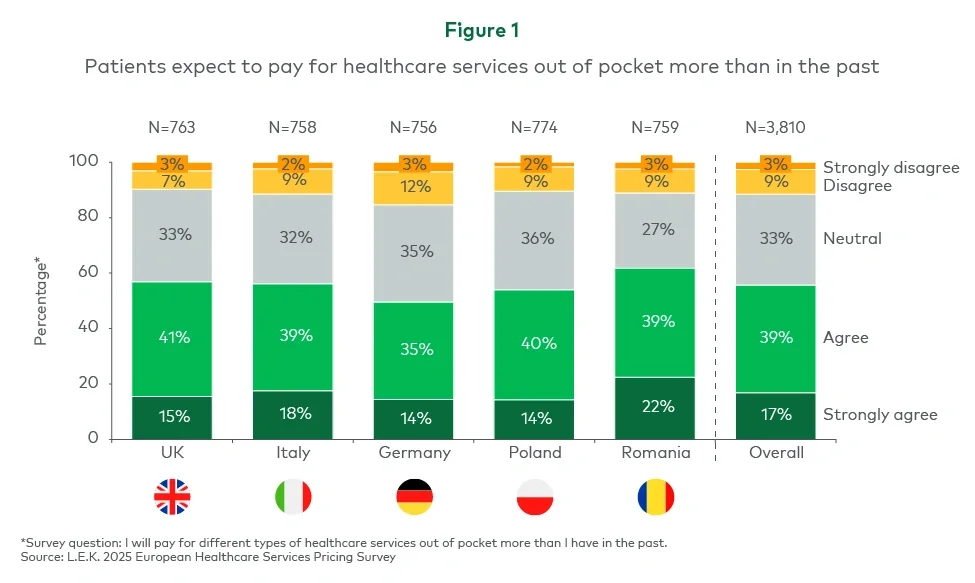

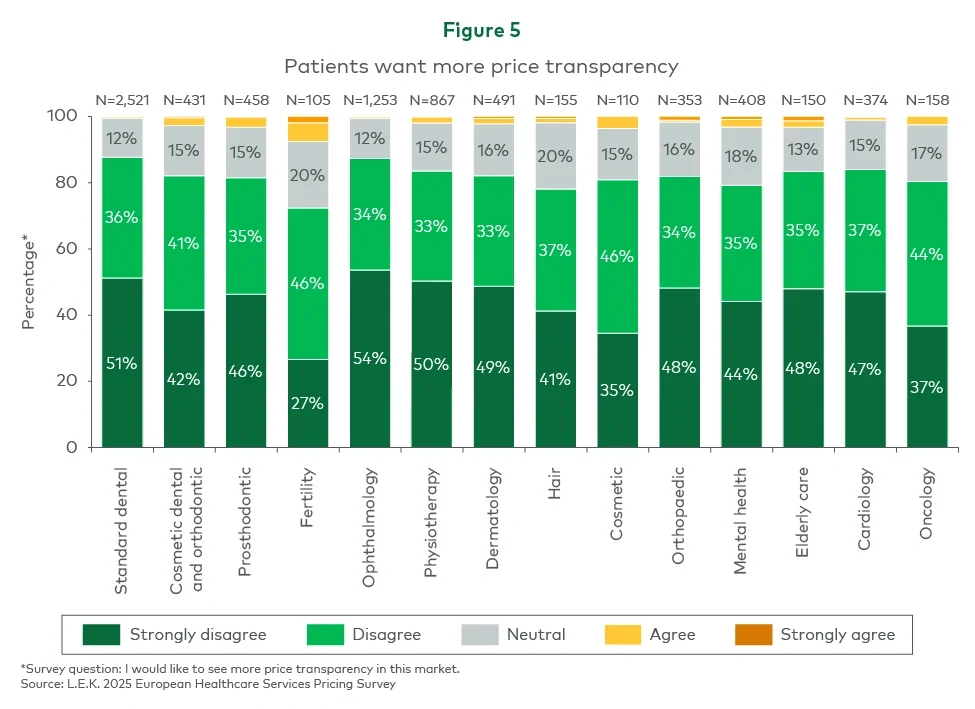

Out-of-pocket spend is rising, but pricing discipline isn’t keeping up

Private pay, once a niche or supplementary funding source, is becoming a core pillar of healthcare financing. Across markets, more than half of respondents said they expect to increase out-of-pocket spending in the next five years (see Figure 1). Even in countries with strong public coverage, like the UK and Germany, a significant share of patients foresee a shift toward personal healthcare expenditure.